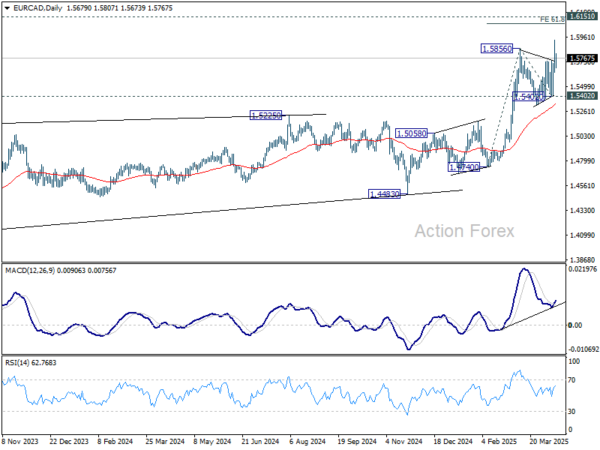

Sterling and the US Dollar are leading gains among major currencies today, lifted by anticipation surrounding the imminent announcement of a comprehensive US-UK trade agreement. The Pound remained resilient after BoE’s expected 25bps rate cut. The three-way split within the BoE’s Monetary Policy Committee and the mixed implications of its economic projections have made it difficult for markets to form a decisive reaction.

BoE’s updated economic projections included two alternative scenarios, one based on weaker global demand due to trade disruptions, the other on renewed inflation stickiness from second-round effects. But with global trade dynamics in flux, these projections are highly conditional and arguably academic at this stage. A trade deal with the US may relieve some economic pressure on Britain, but its benefit depends on how the US proceeds with other partners, especially the EU and China.

For now, attention is squarely on the 1400 GMT press conference where US President Donald Trump is expected to formally unveil the UK trade deal. Trump described the agreement as “full and comprehensive,” calling it a first step in a broader realignment of US trade policy. UK Prime Minister Keir Starmer’s office confirmed talks have progressed swiftly and promised an update later today.

Meanwhile, Euro is also holding firm despite signs of growing transatlantic strain. European Commission has announced preparations for countermeasures in response to Washington’s reciprocal tariff regime, launching a WTO dispute and consulting on duties affecting EUR 95B worth of US imports. Still, EC President Ursula von der Leyen emphasized a preference for negotiation, suggesting room remains for diplomacy.

In contrast, Yen is the weakest major currency today, Loonie and Swiss Franc. Aussie and Kiwi are positioning in the middle.

Technically, Bitcoin’s rally from 74373 resumed today by breaking through 97944 resistance. Further rally is expected as long as 93351 support holds, to retest 109571 record high. Nevertheless, barring clear sign of upside acceleration, current rise is seen as the second leg a medium term corrective pattern. Hence, strong resistance is expected from 109571 to limit upside to bring near term reversal.

In Europe, at the time of writing, FTSE is up 0.17%. DAX is up 0.80%. CAC is up 0.92%. UK 10-year yield is up 0.025 at 4.489. Germany 10-year yield is up 0.018 at 2.494. Earlier in Asia, Nikkei rose 0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.28%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield rose 0.025 to 1.325.

US initial jobless claims fall to 228k vs exp 235k

US initial jobless claims fell -13k to 228k in the week ending May 3, below expectation of 235k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims fell -29k to 1879k in the week ending April 26. Four-week moving average of continuing claims rose 9k to 1875k.

BoE cuts 25bps, three-way vote split reveals growing rift on rate path

BoE lowered its benchmark Bank Rate by 25 basis points to 4.25% , in line with market expectations. However, the decision revealed a rare three-way split among policymakers.

Five members supported the 25bps reduction, while Catherine Mann and Chief Economist Huw Pill voted to keep rates unchanged. On the dovish end, Swati Dhingra and Alan Taylor backed a deeper 50bps cut.

In its accompanying statement, BoE reiterated that a “gradual and careful approach” remains appropriate as it withdraws monetary restraint.

While acknowledging progress on inflation, the central bank emphasized the need for policy to stay “restrictive for sufficiently long” to ensure inflation returns sustainably to the 2% target.

In its latest Monetary Policy Report, the BoE’s baseline forecast sees CPI inflation rising to 3.5% in Q3 2025 before easing back to 2% in the medium term.

But policymakers outlined two risk-laden alternative scenarios. The first, a lower demand scenario, assumes heightened uncertainty depresses domestic spending and inflationary pressures fade more quickly. Under this path, the economy faces a wider output gap and inflation runs -0.3% lower than baseline by the three-year horizon.

Conversely, the second scenario envisions higher inflation persistence, where near-term rise in headline inflation triggers second-round effects in wages and prices, compounded by weak productivity growth. In this case, the impact on growth is modest, but inflation runs 0.4% above baseline throughout the forecast period.

RBNZ flags global growth risks as tariffs echo COVID-era disruptions

RBNZ Governor Christian Hawkesby warned today that rising global tariffs are having a clear and negative impact on global economic activity, prompting the central bank to revise down its projections for global growth.

Speaking to a parliamentary committee, Hawkesby called the effects of the tariff wave “unambiguously” harmful. He added that while New Zealand’s exposure to a 10% US tariff on exports poses challenges, the softer New Zealand Dollar may help cushion some of the blow. Nonetheless, weaker demand from key trading partners is now a growing concern for the country’s outlook.

Hawkesby drew a stark comparison between the supply-side disruptions caused by current tariffs and those seen during the COVID-19 pandemic, stressing that both are capable of delivering long-lasting economic distortions.

“We know from our experience, from the COVID experience, that supply side impacts are significant, and that are long-lasting and can create real challenges,” he said.

He added that the situation remains fluid, with considerable uncertainty about how the structural dynamics of the global economy will adjust to this new trade regime.

BoJ minutes: Caught between global uncertainty and domestic price pressures

Minutes from BoJ’s March meeting revealed growing concern among policymakers over the external risks posed by US tariff policies.

One member warned that downside risks from these policies had “rapidly heightened” and could significantly harm Japan’s real economy, suggesting BoJ should “be particularly cautious when considering the timing for the next rate hike.”

However, not all board members advocated for a cautious stance. Another member stressed that even amid heightened uncertainty, BoJ should not automatically default to a cautious stance, stating that BOJ “might face a situation where it should act decisively”.

A third voice on the board emphasized the importance of incorporating inflation expectations, upside risks to prices, and progress in wage growth into BoJ’s policy deliberations. Domestic developments could still justify tightening if conditions shift meaningfully.

Separately, BoJ Governor Kazuo Ueda reinforced this message in his remarks to parliament today, acknowledging that while food price volatility, particularly for rice, remains elevated, these pressures would ease over time.

Nonetheless, Ueda emphasized the importance of monitoring price developments closely, given the elevated uncertainty in the global economic environment.

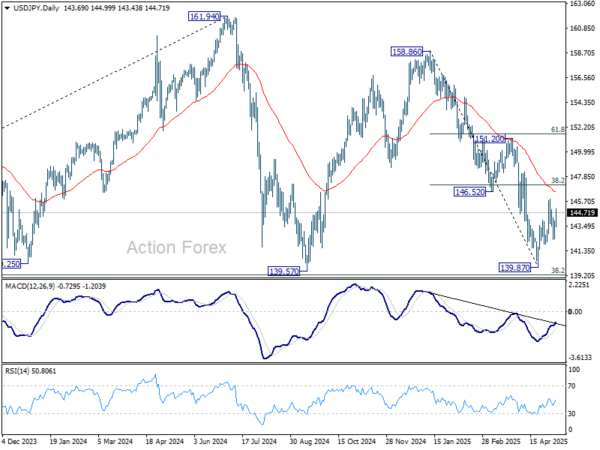

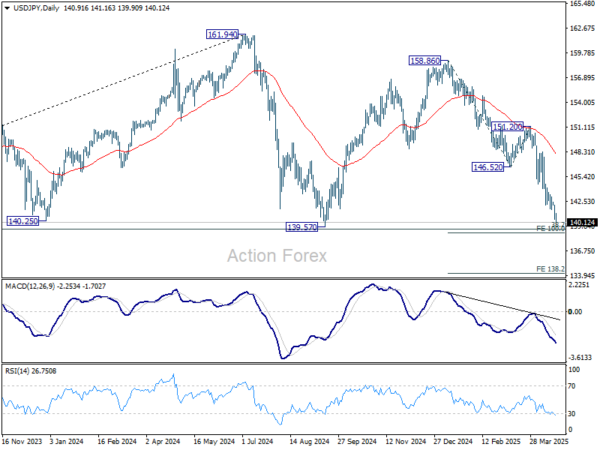

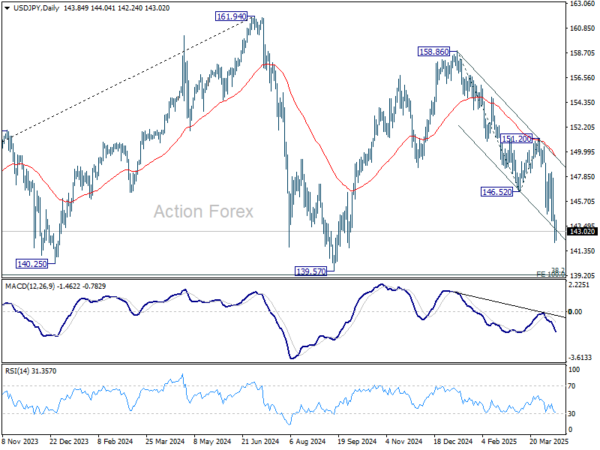

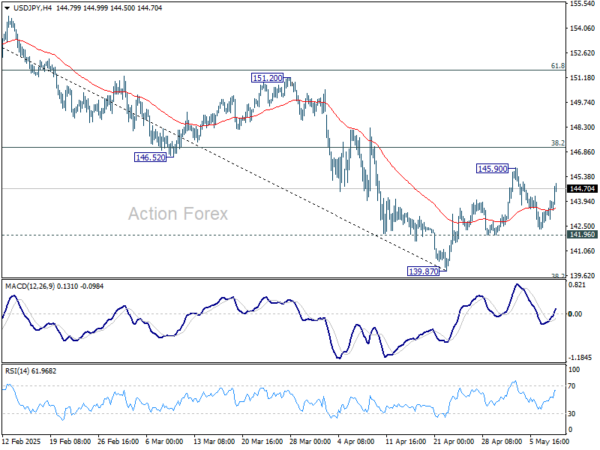

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.81; (P) 143.40; (R1) 144.43; More…

USD/JPY rebounded further today but stays below 145.90 resistance. Overall, rise from 139.87 could extend through 145.90. But near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds, in case of another bounce. On the downside, firm break of 141.96 will argue that rebound from 139.87 has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.