Risk sentiment in the forex markets appears to be tilting towards risk aversion in Asian trading, marking a shift from the broad Dollar selloff earlier in the week. Overnight, US President Donald Trump granted temporary tariff exemptions for Canadian and Mexican goods under the USMCA, delaying a full-scale implementation until April 2. While this provided some relief for Canadian Dollar, overall market sentiment remained fragile, with major US equity indexes closing in the red, led by losses in NASDAQ.

The temporary exemption covers roughly 50% of Mexican imports and 38% of Canadian imports. However, Trump’s move has done little to inspire confidence, as markets remain skeptical about his erratic trade policies. Investors have become wary of his inconsistent messaging—one day insisting on strict tariff enforcement, the next day granting exemptions. This unpredictability has left traders cautious, unsure of how to position for potential future shifts in trade policy.

Despite the tariff delay, risk-sensitive currencies like Australian and New Zealand Dollars have come under renewed selling pressure in Asia. The broader market focus has shifted toward the April 2 deadline, when Trump’s proposed “reciprocal tariffs” are set to take effect. These tariffs will target foreign nations that impose import taxes on US goods, keeping trade war fears firmly in play.

Adding to market unease is the upcoming US non-farm payrolls report. With sentiment already on shaky ground, any significant weakness in the jobs data could deepen risk aversion. While a weaker NFP might increase expectations for a Fed rate cut, traders are growing concerned that deteriorating labor market conditions could signal a sharper economic slowdown. This dynamic suggests that even rising Fed cut bets may not be enough to offset broader recession fears.

So far for the week, Dollar remains the worst-performing currency, struggling to find any solid footing. Canadian Dollar follows closely as the second weakest, alongside Australian Dollar. On the stronger side, Euro continues to outperform, driven by optimism over fiscal expansion plans in Europe. Sterling and Swiss Franc are also holding firm, while Yen and Kiwi are settling in the middle.

In Asia, the time of writing, Nikkei is down -2.07%. Hong Kong HSI is down -0.06%. China Shanghai SSE is up 0.15%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is up 0.023 at 1.535. Overnight, DOW fell -0.99%. S&P 500 fell -1.78%. NASDAQ fell -2.61%. 10-year yield rose 0.021 to 4.286.

NFP in focus: NASDAQ and S&P 500 at risk of deeper correction

US markets are standing on precarious footing, with investors attention on the February non-farm payrolls report due later in the day. There has been noticeable anxieties surrounding the impact of fiscal and trade policies changes. A set of weaker-than-expected NFP data could be taken as another signal of swift deceleration in the economy and rattle market sentiment further.

Cooldown in the job market might prompt Fed to resume rate cuts earlier. Markets are currently pricing in 53% chance of a 25bps rate cut in March, reflecting growing belief that Fed will need to act sooner rather than later. However, the immediate market response to downside surprises may not be relief over monetary easing but rather heightened concerns about the pace of economic weakening, given recent policy uncertainties and trade disruptions.

Markets anticipate 156k increase in NFP for February, up from 143k in January. The unemployment rate is forecast to remain at 4.0%, while average hourly earnings should hold steady at 0.3% m/m.

The latest indicators paint a mixed picture: ISM Manufacturing PMI Employment subindex dropped to 47.6 from 50.3, while ISM Services PMI Employment inched up to 53.9 from 52.3. Meanwhile, ADP Employment reading of 77k missed last month’s 186k, and the 4-week moving average of jobless claims rose to 224k—its highest level so far this year.

Technically, NASDAQ has been sliding for two consecutive weeks, now testing its 55-week EMA at 17,874.13. A decisive break below this level would confirm that the index is at least in a correction relative to the broader uptrend from the 10,088.82 low in 2022. The next key support to watch is the 38.2% Fibonacci retracement of 10,088.82 to 20,204.58, which comes in at 16,340.36. Extended losses here could set a negative tone for broader U.S. equities.

The S&P 500, still trading comfortably above its 55-week EMA at 5,590.31, may follow in the NASDAQ’s footsteps if sentiment sours further. Should the index breach this EMA convincingly, it would likely confirm that the fall from 6,147.43 is a correction of the uptrend from the 3,491.58 low in 2022. This scenario would set a 38.2% retracement target around 5,132.89, marking a significant downside pivot.

Overall, whether today’s NFP meets, misses, or exceeds expectations, the market’s reaction will hinge on how investors interpret the labor data in the context of looming trade uncertainties and weakening growth momentum. A softer reading could drive near-term Fed cut bets higher but might also deepen concerns that the U.S. economy is losing steam, thereby raising the stakes for traders and policymakers alike.

Technically, NASDAQ is now eyeing 55 W EMA (now at 17874.13) with the extended decline in the past two weeks. Sustained break there will confirm that it’s at least in correction to the up trend from 10088.82 (2022 low). Next target will be 38.2% retracement of 10088.82 to 20204.58 at 16340.36.

Extended selloff in NASDAQ could be a prelude to the similar development in S&P 500. While it’s still well above 55 W EMA (now at 5590.31), sustained break there will align the outlook with NASDAQ. Fall from 6147.43 would then be correcting the up trend from 3491.58 (2022 low) at least, and target 38.2% retracement of 3491.58 to 6147.43 at 5132.89.

Fed’s Waller: No immediate rate cut, but open to future easing

Fed Governor Christopher Waller suggested that another rate cut at the next FOMC meeting is unlikely, but he remains open to further easing down the line.

“I would’t say at the next meeting, but could certainly see [cuts] going forward,” he noted. Waller particularly highlighted the February inflation report and the evolving impact of trade policies as key factors in shaping the Fed’s outlook.

Waller acknowledged the challenges in assessing the economic effects of tariffs, citing changing economic conditions and President Trump’s harder trade stance as factors complicating policy decisions.

He noted that evaluating the impact of tariffs is more difficult this time, adding, “It’s very hard to eat a 25% tariff out of the profit margins.”

Fed’s Bostic: Economy in flux, no rush to adjust policy

Atlanta Fed President Raphael Bostic emphasized the high level of uncertainty in the US economy due to evolving policies under the Trump administration. With inflation, trade policies, and government spending all in flux, he suggested that meaningful clarity may not emerge until “late spring or summer”. Given this, he reiterated “We’ll have to just sort of really be patient.”

Speaking overnight, he described the situation as being in “incredible flux,” with rapid shifts in trade and fiscal policies making it difficult to predict economic trends. Given this backdrop, Bostic urged caution, stating, “You’ve got to be patient and not want to get too far ahead.”

He noted that just this week, there have been significant swings in expectations regarding economic policy. “If I was waiting before to see and get a clear signal about where the economy is going to go, I’m definitely waiting now,” he said.

BoE’s Mann: Larger rate cuts needed as global spillovers worsen

BoE MPC member Catherine Mann argued that recent monetary policy actions have been overshadowed by “international spillovers.” Financial market volatility, particularly from cross-border shocks, has disrupted traditional policy signals, making “founding premise for a gradualist approach to monetary policy is no longer valid”.

Mann said that larger rate cuts, like the 50bps reduction she supported at the last BoE meeting, would better “cut through this turbulence” and provide clearer guidance to the economy.

She believes that a more decisive policy stance would help steer inflation expectations and stabilize economic conditions, rather than allowing uncertainty to linger with smaller, incremental moves.

Despite her stance, the BoE opted for a smaller 25bps rate cut in its latest decision, with Mann and dovish member Swati Dhingra being outvoted 7-2.

China’s exports rise 2.3% yoy, imports fall -8.4% yoy

China’s exports rose just 2.3% yoy to USD 539.9B in the January–February period, coming in below forecasts of 5.0% yoy and down sharply from December’s 10.7% yoy.

Meanwhile, imports sank -8.4% yoy to USD 369.4B, missing expectations of 1.0% yoy growth and marking a noticeable drop from December’s 1.0% yoy.

As a result, trade balance resulted in USD 170.5B surplus exceeding projections of USD 147.5B.

Looking ahead

Germany factory orders, Swiss foreign currency reserves and Eurozone GDP revision will be released in European session. Later in the day, Canada employment will also be published alongside US NFP.

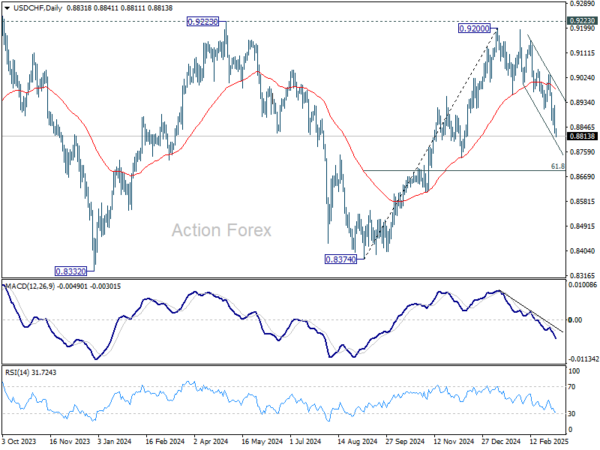

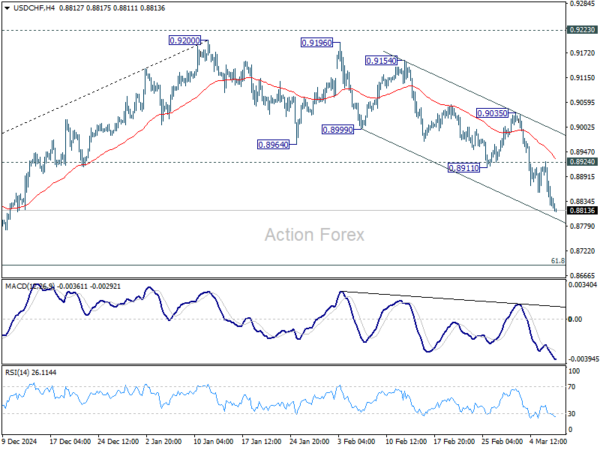

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8800; (P) 0.8863; (R1) 0.8900; More…

Intraday bias in USD/CHF remains on the downside for the moment. Rise from 0.8374 should have completed at 0.9222, after rejection by 0.9223 key resistance. Deeper fall should be seen to 61.8% retracement of 0.8374 to 0.9200 at 0.8690 next. On the upside, above 0.8924 minor resistance will turn intraday bias neutral first. But rise will now stay on the downside as long as 0.9035 resistance holds, in case of recovery.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.