Dollar initially surged after the US Court of International Trade ruled against President Donald Trump’s sweeping reciprocal tariff orders. Market participants initially interpreted the ruling as a potential turning point in the US trade policy, fueling a rally in the greenback and risk assets.

However, the greenback’s rally proved short-lived. As the US session opened, the greenback reversed course and turned broadly lower. Traders began to reassess the practical implications of the ruling, with many suspecting that the Trump administration could still find legal or procedural workarounds to reinstate the tariffs.

In that context, the ruling may have increased legal complexity but done little to reduce the overarching geopolitical uncertainty. Traders are clearly skeptical that the legal setback will lead to a meaningful shift in trade tensions.

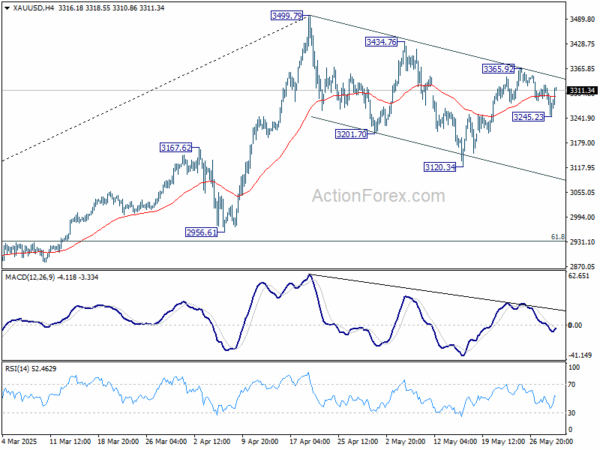

Indeed, skepticism is evident across financial markets. DOW futures, which had gained more than 500 points earlier in the day, gave back almost all of those gains. NASDAQ remained resilient, supported by tech sector optimism, but broader risk appetite appeared to fade. Gold, meanwhile, rebounded above the 3300 level as safe-haven demand returned, signaling that markets are still hedging against unresolved geopolitical and policy risks.

In currency markets, the shift in sentiment was clear. Dollar is now the weakest performer of the day, followed by Sterling and then Yen. Aussie emerged as the top gainer, while Euro and Kiwi also firmed. Swiss Franc and Canadian dollar are trading in the middle of the pack.

Technically, intraday bias in Gold is turned neutral first with current recovery. On the upside, break of 3365.92 resistance will revive the case that correction from 3499.79 has completed with three waves down to 3120.34, and bring retest of 349.79 high. Nevertheless, below 3245.23 will extend the corrective pattern with another falling leg.

In Europe, at the time of writing, FTSE is flat. DAX is up 0.23%. CAC is up 0.63%. UK 10-year yield is down -0.006 at 4.726. GErmany 10-year yield is down -0.005 at 2.551. Earlier in Asia, Nikkei rose 1.88%. Hong Kong HSI rose 1.35%. China Shanghai SSE rose 0.70%. Singapore Strait times rose 0.13%. Japan 10-year JGB yield rose 0.003 to 1.520.

US initial jobless claims rise to 240k vs exp 230k

US initial jobless claims rose 14k to 240k in the week ending May 24, above expectation of 230k. Four-week moving average of initial claims fell -250k to 231k.

Continuing claims rose 26k to 1919k in the week ending May 17, highest since November 13, 2021. Four-week moving average of continuing claims rose 3k to 1890k, highest since November 27, 2021.

RBNZ’s Hawkesby: OCR in neutral zone, July cut not a done deal

RBNZ Governor Christian Hawkesby told Bloomberg TV today that another rate cut at the July meeting is “not a done deal” and “not something that’s programmed.”

With the OCR at 3.25% after this week’s reduction, it’s now sitting within the estimated neutral range of 2.5% to 3.5%. Hawkesby emphasized the central bank has entered a phase of “considered steps,” guided closely by incoming data rather than a preset easing path.

He acknowledged rising uncertainty, noting that near-term growth headwinds have intensified and both demand and inflation pressures are weaker than they were back in February. He also highlighted the uncertainty surrounding global trade policy, particularly tariff developments, which could play out in various ways.

NZ ANZ business confidence falls to 36.6, supporting case for further RBNZ easing

New Zealand’s ANZ Business Confidence index dropped sharply in May, falling from 49.3 to 36.6. Own Activity Outlook, a key indicator of firms’ expectations for their own performance, declined to 34.8 from 47.7.

Profit expectations also plunged to 11.1, indicating mounting pressure on margins. Although cost and wage expectations eased slightly, they remain elevated, while inflation expectations edged up from 2.65% to 2.71%.

According to ANZ, the survey paints a mixed picture: the economy is in recovery mode, but businesses continue to face tough operating conditions, particularly in passing on cost increases. The data reinforces the view that RBNZ can afford to support growth through further rate cuts, barring any major inflation or data surprises.

ANZ expects the OCR to eventually fall to 2.5%, as global headwinds and domestic fragilities persist.

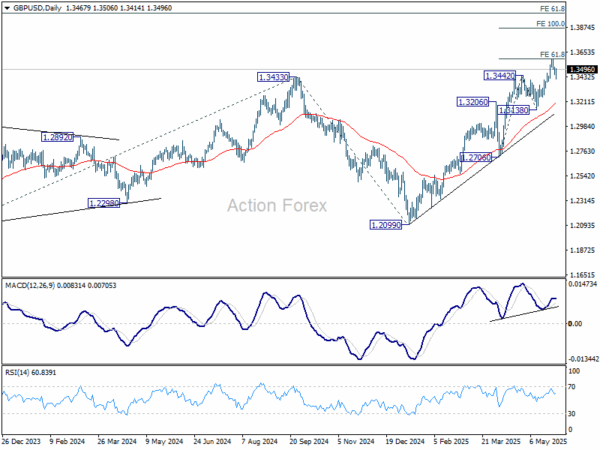

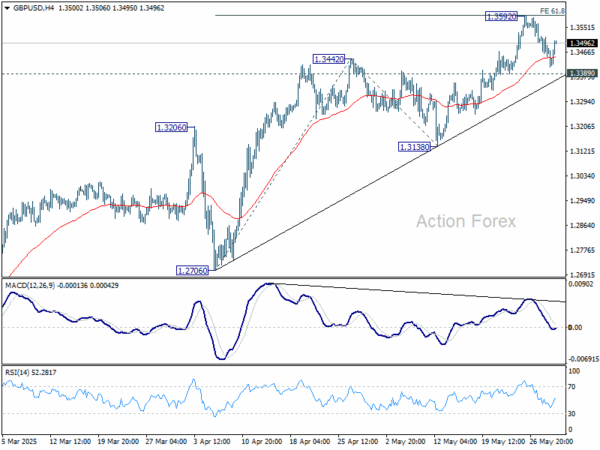

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3440; (P) 1.3481; (R1) 1.3512; More…

Intraday bias in GBP/USD remains neutral for the moment. With 1.3389 support intact, further rally is expected. On the upside, firm break of 1.3592 will resume larger rally for 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, decisive break of 1.3389 will confirm short term topping, and turn bias back to the downside for 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2870) holds, even in case of deep pullback.