There was a fleeting uptick in sentiment overnight after US President Donald Trump spoke by phone with Chinese President Xi Jinping, calling the conversation “very positive” and announcing renewed lower-level trade talks. However, the initial optimism quickly faded, with major US indexes reversing early gains to end the session lower.

The Chinese readout was more cautious, stressing that the US should “withdraw negative measures” and warning Washington to handle Taiwan “prudently.” The divergence in tone reinforces the sense that the two sides remain far apart. The agreement to more talks appears to be little more than a tactical delay rather than genuine progress.

Elsewhere, US Treasury called on BoJ to continue policy tightening to support a normalization of Yen and correct bilateral trade imbalances. The statement, part of the Treasury’s semiannual currency report, suggested Tokyo had more to do on the policy front.

However, Japan’s Finance Minister Katsunobu Kato offered a restrained response, reiterating that monetary decisions lie with the BOJ and avoiding direct comment on the US call for further tightening. Yen, meanwhile, barely reacted, continuing its technical consolidation as it drifts slightly lower against Dollar.

In currency markets, Dollar remains the worst performer of the week heading into Friday’s crucial non-farm payrolls release. With a string of weak labor-related indicators earlier this week—ADP, ISM employment components, and initial claims—markets are bracing for a soft headline. Yen and Swiss Franc are also lagging this week, underperforming alongside the greenback

On the other hand, Kiwi leads the pack, while Aussie and Sterling also posted modest gains Euro and Loonie Dollar are positioning in the middle. However, all these standings remain subject to sharp realignment depending on the tone of the upcoming US employment data and its interplay with broader market sentiment.

In Asia, at the time of writing, Nikkei is up 0.51%. Hong Kong HSI is down -0.09%. China Shanghai SSE is down -0.06%. Singapore Strait Times is up 0.16%. Japan 10-year JGB yield is flat at 1.462. Overnight, DOW fell -0.25%. S&P 500 fell -0.53%. NASDAQ fell -0.83%. 10-year yield rose 0.029 to 4.394.

Looking ahead, Germany will release industrial production and trade balance in European session. Swiss will publish foreign currency reserves while Eurozone will release retail sales and GDP revision. Later in the day, Canada will also release job data along with US non-farm payrolls.

US NFP: Muted Hiring or Major Miss?

Markets are awaiting today’s US non-farm payrolls release, with little doubt that hiring had slowed meaningfully in May amid heightened tariff threats and elevated uncertainty. The key question now is just how sharp the slowdown was.

Consensus forecasts see NFP at 130K, unemployment steady at 4.2%, and average hourly earnings rising 0.3% mom. Recent labor indicators have painted a dismal picture. ADP private employment came in at just 37k, a stark miss. ISM Manufacturing employment stayed subdued at 46.8 and the Services component barely rose back into expansion territory at 50.7. Meanwhile, 4-week average of jobless claims has crept up to 235k.

While a modest softening in job growth would likely be tolerated as a natural response to macro headwinds, any significant downside surprise could reignite recession fears. An NFP reading below 100K could provoke a sharp risk-off response in equities. However, such a result would likely weigh further on Dollar, as markets would begin pricing in earlier Fed rate cuts in response to labor market deterioration.

Technically, S&P 500 extended the near term rise from 4835.04 this week, but continued to lose upside momentum as seen in D MACD. This rise is seen as the second leg of the corrective pattern from 6147.43. Hence, while further rise cannot be ruled out, given that S&P 500 is now close to 6000, upside potential is limited. On the other hand, break of 5767.41 support will signal that a short term top was already formed. Deeper pull back should be seen back to 38.2% retracement of 4835.04 to 5999.70 at 5554.79, with risk of bearish reversal.

Fed’s Kugler: Tariffs may entrench inflation via expectations, pricing power, and productivity

Fed Governor Adriana Kugler cautioned that disinflation “has slowed” and that tariffs are beginning to exert upward pressure on prices, a trend she expects to continue into 2025. Speaking overnight, Kugler emphasized that the balance of risks has tilted, with “greater upside risks to inflation” now emerging, even as downside risks to employment and growth loom on the horizon. As a result, she reaffirmed support for holding the current policy rate steady.

Kugler outlined three channels through which tariffs could entrench inflationary pressures. First, she noted that rising short-term inflation expectations may grant businesses “more leeway to raise prices”, thereby increasing inflation persistence.

Second, she flagged the risk of “opportunistic pricing”, where firms use tariff headlines as cover to hike prices even on unaffected goods. This, combined with higher costs on intermediate goods, could generate “second-round effects” on inflation.

The third concern relates to “lower productivity”. As firms contend with elevated input costs and weaker demand, they may reduce capital investment and resort to less efficient production methods, reinforcing inflationary pressure through lower productivity.

Fed’s Schmid: Tariff impact uncertain, policy must stay nimble

Kansas City Fed President Jeff Schmid acknowledged in a speech overnight that monetary theory may suggest to “looking through a one-time price shock”, he would be “uncomfortable staking the Fed’s reputation and credibility on theory alone.”

Despite the expected drag from tariffs, Schmid remains “optimistic” about the economy’s momentum. However, he acknowledged that both the inflationary and growth implications of tariffs are highly uncertain.

As a result, he argued that Fed will “need to remain nimble”, and be prepared to adjust its stance as needed to maintain both price stability and maximum employment.

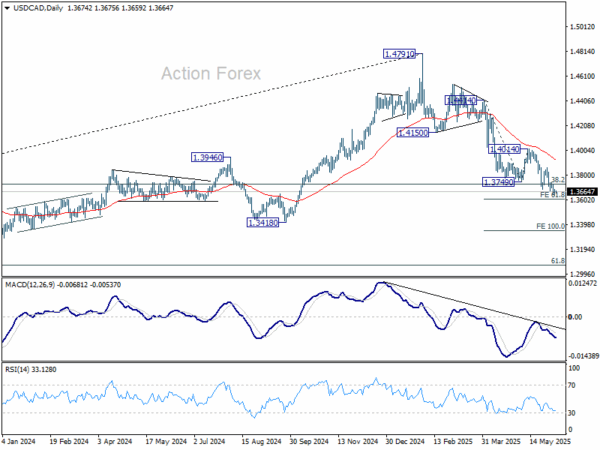

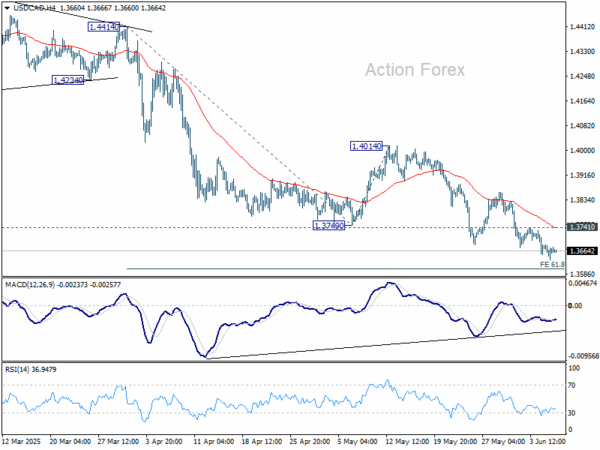

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3645; (P) 1.3665; (R1) 1.3694; More…

Intraday bias in USD/CAD stays on the downside as decline from 1.4791 is in progress. . Next target is 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. Firm break there will pave the way to 100% projection at 1.3349. On the upside, above 1.3741 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.