Risk aversion returned forcefully overnight, with Wall Street suffering its steepest daily decline in a month as investors unwound exposures. The reopening of the U.S. government offered no support to sentiment, with markets instead refocusing on the prospect that a December Fed rate cut is far from assured. Comments from several Fed officials pushed back against aggressive easing expectations, prompting Fed fund futures to mark down the odds of a December cut to around 50%, from nearly 70% just one week ago. The shift revived concerns that policy support may not arrive as early as traders had hoped.

Technology stocks bore the brunt of the selloff. Major AI leaders, including Nvidia and other semiconductor names, saw another round of heavy liquidation, a stark reversal from the early-week relief rally. It appears the market’s concern over stretched AI valuations was only temporarily set aside—not dismissed.

Asian sentiment followed the U.S. lower, with Nikkei and Kospi leading declines. SoftBank’s sharp plunge, extending a third day of heavy losses after confirming on Tuesday that it had sold its entire Nvidia stake, added an extra drag to regional tech shares.

China offered no cushion. Fresh data showed an even deeper slowdown in October, driven by weak consumer demand, falling investment, and the ongoing property downturn. The soft tone reinforced the perception that China’s recovery remains uneven and fragile.

Nevertheless, there was one constructive development on the trade front. The U.S. and Switzerland moved closer to a deal that could reduce the crippling 39% U.S. tariffs on Swiss imports. After talks in Washington, both sides described discussions as “very positive,” with Swiss Economy Minister Guy Parmelin saying virtually all issues were clarified.

An unnamed Swiss official said a deal has been effectively reached, pending final approval from US President Donald Trump. A senior U.S. official echoed the optimism, adding that Switzerland had presented a plan to reduce its trade surplus with the U.S. and lower non-tariff barriers, creating a path for tariff reductions if the White House signs off.

In the currency markets, Swiss Franc remains the strongest performer this week, benefiting from safe-haven flows and expectations of a breakthrough in trade negotiations. Kiwi and Aussie hold second and third place but are starting to look vulnerable as risk sentiment deteriorates.

At the other end of the spectrum, Yen remains pinned at the bottom, pressured by expectations that the BoJ will delay its long-anticipated hike until January at the earliest. Sterling is the second weakest as soft data reinforce BoE cut expectations for December. Dollar sits third-weakest, while Euro and Loonie are positioned in the middle of the weekly rankings.

In Asia, at the time of writing, Nikkei is down -1.59%. Hong Kong HSI is down -1.26%. China Shanghai SSE is down -0.16%. Singapore Strait Times is down -0.78%. Japan 10-year JGB yield is up 0.008 at 1.699. Overnight, DOW fell -1.65%. S&P 500 fell -1.66%. NASDAQ fell -2.29%. 10-year yield rose 0.047 to 4.112.

China industrial production slows to 4.9% yoy in October, investment contraction deepens

China’s October activity data pointed to a loss of momentum, with industrial production rising 4.9% yoy, down from September’s 6.5% yoy and below expectations of 5.6%. It marks the weakest annual pace since August 2024.

Retail sales also slowed, rising 2.9% yoy compared with 3.0% in September, though slightly outperforming expectations of 2.7% yoy. Still, it was the slowest pace since August last year, underscoring persistently cautious household demand. Excluding autos, consumer goods retail sales rose a firmer 4.0%, suggesting pockets of resilience but not enough to anchor a broad consumption recovery.

More concerning was the continued drag from investment: fixed asset investment fell -1.7% ytd yoy, deteriorating from -0.5% and missing expectations of -0.7%. Private-sector investment remained under heavy pressure, dropping -4.5%, underscoring structural weakness in confidence, property-linked spillovers, and limited risk appetite.

New Zealand BNZ PMI at 51.4 as orders hit three-year high

New Zealand’s manufacturing sector showed further improvement in October, with BusinessNZ PMI rising from 50.1 to 51.4, marking a fourth straight month above 50. While still below the long-term average of 52.4, the sector is now experiencing its most sustained period of expansion in three years, hinting that the worst of the downturn may be behind it.

The details were encouraging: production improved from 50.5 to 52.0. New orders jumped from 50.5 to 54.9, the strongest pace since August 2022 and a key sign that demand conditions are firming. Employment remained in contraction at 48.1, up from 47.7, but even that component showed stabilization after six months of declines.

BusinessNZ’s Catherine Beard said October brought “more signs of life” after months of stagnation. The share of negative respondent comments fell from 60.2% to 54.1%, with many firms reporting stronger orders, seasonal demand, new customers, and productivity gains driven by process improvements and automation.

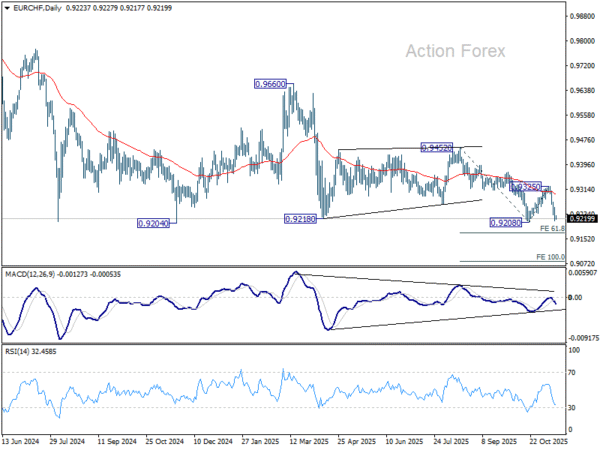

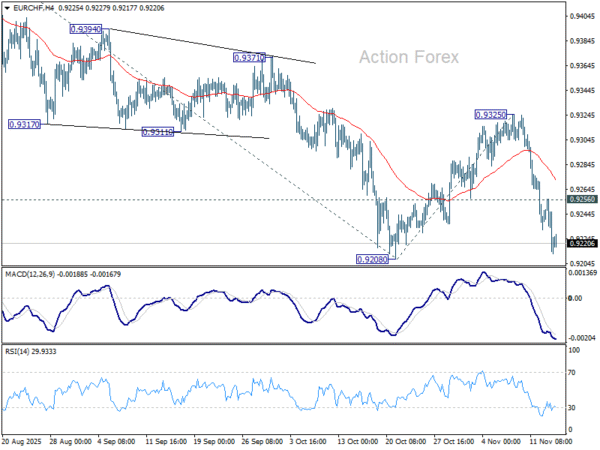

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9207; (P) 0.9233; (R1) 0.9252; More….

Intraday bias in EUR/CHF remains on the downside for 0.9204/8 support zone. Break there will confirm larger down trend resumption. Next near term target is 61.8% projection of 0.9452 to 0.9208 from 0.9325 at 0.9175. Decisive break there could prompt downside acceleration to 100% projection at 0.9082. On the upside, above 0.9256 minor resistance will delay the bearish case and turn bias neutral first.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9383). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. However, break of 0.9452 resistance will now be the first sign of medium term bottoming.