Risk aversion reasserted itself across global markets overnight as NASDAQ led US equities sharply lower once again, with AI disruption fears resurfacing as the primary catalyst. Asian markets followed and traded broadly lower. The vulnerability in equities was mirrored in fixed income markets. Safe-haven demand pushed US Treasuries higher, sending the 10-year yield tumbling and extending its recent technical breakdown.

Attention now turns to the January US CPI release. However, expectations for sustained volatility following the data appear limited. Instead, the more important question is whether AI-driven risk-off trades quickly resume once the event risk passes. If sentiment remains fragile, markets could revert to selling rallies in technology and cyclicals rather than focusing solely on inflation dynamics.

Meanwhile, not all traditional safe havens behaved uniformly. Gold and silver experienced what some described as a flash crash, diverging from the broader defensive tone. The trigger appeared to be geopolitical rather than macroeconomic. US President Donald Trump said he insisted that talks with Iran continue during a meeting with Israeli Prime Minister Benjamin Netanyahu, adding that a deal could be reached within a month. The remarks were interpreted as reducing near-term geopolitical risk premiums embedded in precious metals and oil prices.

On trade policy, fresh research from the New York Fed highlighted 90% of tariffs imposed on imported goods are absorbed by American consumers and companies. The study found that Americans absorbed 94% of tariff costs between January and August, easing slightly later in the year but still accounting for the vast majority of the burden. These findings align with analysis from the Congressional Budget Office, which estimates that 70% of import price increases are passed through to consumers, with businesses absorbing 30% via lower margins.

Separately, the US finalized a trade agreement with Taiwan, setting tariffs on Taiwanese exports at 15% and opening Taiwan’s market to US goods. Taipei committed to removing or reducing 99% of tariff barriers and pledged to purchase over USD 84 billion in US goods between 2025 and 2029, including LNG, crude oil and aircraft.

In currency markets, Yen remains the strongest performer of the week, followed by Aussie and Swiss Franc. Sterling is now the weakest, trailed by Dollar and Kiwi, while Euro and Loonie trade in the middle.

In Asia, at the time of writing, Nikkei is down -1.14%. Hong Kong HSI is down -2.10%. China Shanghai SSE is down -0.76%. Singapore Strait Times is down -1.43%. Overnight, DOW fell -1.34%. S&P 500 fell -1.57%. NASDAQ fell -2.03%. 10-year yield fell -0.068 to 4.104.

Brutal risk shift ahead of US CPI: Yields sink, NASDAQ fails, USD/JPY under threat

US equities staged a sharp reversal overnight, closing decisively lower with NASDAQ leading losses at -2%. DOW fell -1.3%, slipping back below the 50,000 mark after managing to hold it for four sessions only. Treasury markets reinforced the risk-off signal as 10-year yield took another leg lower and is now on the verge of breaking below 4.1% handle.

January CPI is due, but its influence may be limited. The strong non-farm payrolls report has effectively removed urgency for a March Fed move and supports a pause at least through June. Unless inflation delivers a major shock, markets would revert to broader risk dynamics once the event passes.

The catalyst behind the equity selloff is once again AI disruption anxiety. Software stocks, which have been under persistent pressure this year, extended losses sharply. More concerning is that the negative tone is spreading beyond technology. Financials came under pressure amid fears that AI could disrupt wealth management and advisory services. Industrials and logistics stocks also saw heavy selling on concerns that AI-driven efficiency gains in freight and supply chains could erode traditional revenue models. Even real estate came under scrutiny on speculation that higher unemployment or automation could dampen demand for office space.

Technically, NASDAQ’s rejection at the 55 D EMA (now at 23,229), is a clear near-term bearish signal. Immediate focus now turns to 22,461 support. Firm break there would open the door through 21,898 support towards 38.2% retracement of 14,784.03 to 24,020.00 at 20,419.85.

Meanwhile, 10-year yield’s close below 4.108 solidifies the view that the rebound from 3.947 3.947 has completed as a corrective move to 4.311. As long as 55 D EMA (now at 4.178) caps upside, downside risk dominates. Sustained trading below 4.100 would send yield further to 4.000 psychological level and potentially retest the October low near 3.947.

USD/JPY remains marginally above 38.2% retracement of 139.87 to 159.44 at 151.96, leaving the pattern from 159.44 technically seen as a consolidation within the broader uptrend from 139.87. As long as this level holds, the structural bias cannot be deemed decisively bearish.

That said, extended weakness in US equities and further decline in Treasury yields would likely intensify downside pressure on USD/JPY. A clear break below 151.96 would mark a significant technical shift towards bearish trend reversal. Deeper fall would then likely be seen to 61.8% retracement at 147.34, and possibly below.

BoJ’s Tamura says inflation becoming “sticky,” sees scope to tighten

BoJ board member Naoki Tamura said in a speech that the wage–price cycle the Bank has been aiming to establish remains intact, with inflation increasingly driven by domestic factors rather than imported cost shocks. He argued that inflation is “becoming endogenous and sticky,” as higher labor costs replace raw material prices as the primary driver.

Tamura noted, as early as this spring the Bank could judge its price stability target achieved — provided wage growth in 2026 is confirmed to be consistent with the 2% goal for a third consecutive year. Such confirmation would mark a significant milestone in Japan’s long struggle to exit deflation.

He cautioned, however, that price developments warrant close attention as Yen resumes depreciation. Also, as firms continue to lift wages, there is strong potential for higher labor costs to be passed through across production, distribution and retail stages.

Tamura also there remains “considerable distance” to the neutral interest rate level, implying that even further rate hikes would leave financial conditions accommodative. The challenge, he said, is to avoid both a premature tightening that risks deflation and an environment of persistent inflation that exceeds what can be considered moderate — a balancing act that keeps normalization gradual.

NZ BNZ manufacturing eases to 55.2, but signals continued expansion

New Zealand’s BusinessNZ Performance of Manufacturing Index eased from 56.1 to 55.2 in January, indicating a slight moderation in momentum but remaining firmly in expansion territory. Production slipped from 57.5 to 56.6, employment edged down from 53.7 to 52.9, and new orders cooled from 59.9 to 56.4, pointing to slower yet still solid activity.

Despite the pullback, BNZ described the latest reading as reflecting a “healthy level of expansion.” Senior Economist Doug Steel said the January PMI adds to evidence that the economy has “finally turned the corner,” aligning with forecasts and a broader set of indicators suggesting decent growth.

However, underlying sentiment showed some softening. The proportion of positive comments from respondents fell to 47.7% in January, down from 57.1% in December and 54.4% in November. While the sector remains in growth mode, the decline in optimism hints at a more cautious tone among manufacturers as 2026 begins.

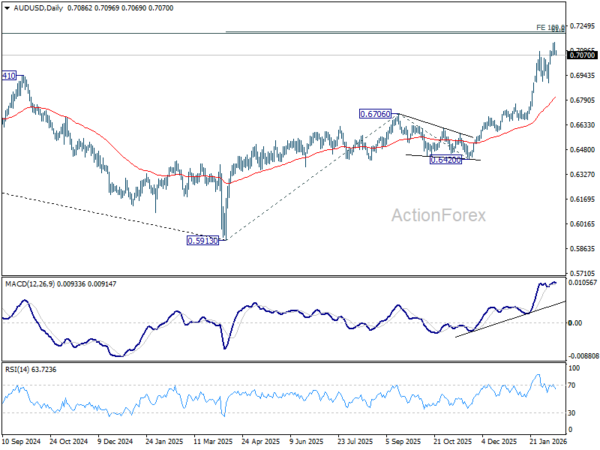

AUD/USD Daily Report

Daily Pivots: (S1) 0.7078; (P) 0.7110; (R1) 0.7159; More…

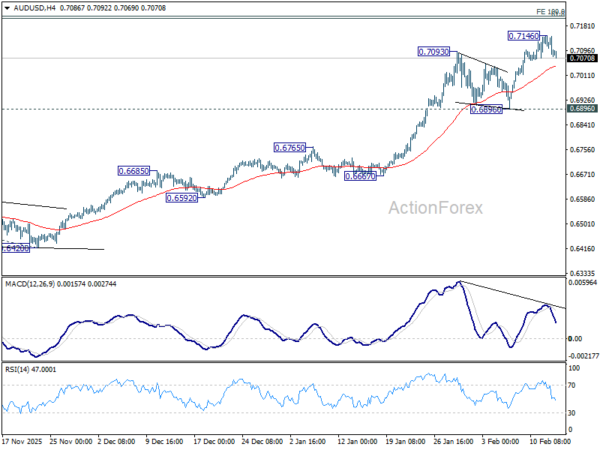

Intraday bias in AUD/USD is turned neutral first with current retreat, and some consolidations would be seen. But downside should be contained above 0.6896 support to bring another rally. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213. However, considering bearish divergence condition in D MACD, firm break of 0.6896 will argue that deeper correction is underway to 55 D EMA (now at 0.6802).

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.