Asian markets traded mixed despite a softer US session overnight. In particular, regional tech stocks showed resilience, with hardware names outperforming on the view that supply-chain positioning remains intact even if US software valuations reset. South Korea’s Kospi notched a fresh record high for a third straight session, powered by a rally in chipmakers. In Japan, the Nikkei also advanced, led by “picks and shovels” AI beneficiaries—equipment makers and component suppliers—on bets that Asian hardware firms will continue to monetize global AI capex. The regional divergence is clearer when contrasted with India, where software services names underperformed.

In China, equities strengthened as markets reopened for the Year of the Horse. Sentiment was buoyed by belief that the recent US Supreme Court ruling striking down sweeping reciprocal tariffs could ease near-term export pressure. The shift from “reciprocal” levies to a flat 15% surcharge has been read as a relative improvement for China. Although US President Donald Trump subsequently announced a temporary 15% global tariff, analysts argue the reset may translate into lower effective rates for China compared with prior proposals under country-specific frameworks. That relative repricing explains the relief bid in onshore shares.

Hong Kong, however, was a regional outlier, slipping as international investors reassessed implications of the new tariff regime. The selloff may reflect “fade the rally” positioning, with global funds cautious that the 150-day surcharge window represents only a temporary pause before more permanent measures are unveiled.

The reconfiguration from reciprocal tariffs to a flat surcharge has produced accidental winners and losers. China, India, and Brazil—previously facing potentially punitive bilateral rates—now fall under the 15% umbrella. Traditional allies such as the UK, Italy, and Australia, which had lower baseline exposure, now face a higher effective floor.

Still, the framework remains fluid. The 15% rate is legally defined as a temporary surcharge with a hard 150-day sunset. The administration is sure to use this period to prepare a more durable tariff architecture, limiting conviction in the relief trade.

Currency markets reflect a mild risk-off tilt. Sterling leads gains, followed by Dollar and Swiss Franc. Australian Dollar is the weakest, trailed by Kiwi and Loonie, while Yen and Euro sit mid-pack. Yet price action lacks follow-through. Major pairs and crosses remain bounded within last week’s ranges, signaling hesitation rather than decisive repositioning. Traders appear reluctant to commit ahead of Trump’s upcoming State of the Union address today, which could clarify what’s next regarding tariffs.

In Asia, at the time of writing, Nikkei is up 0.90%. Hong Kong HSI is down -2.16%. China SHanghai SSE is up 0.87%. Singapore Strait Times is down -0.57%. Japan 10-year JGB yield is down -0.005 at 2.105. Overnight, DOW fell -1.66%. S&P 500 fell -1.04%. NASDAQ fell -1.13%. 10-year yield fell -0.57 to 4.029.

RBA stays focused on quarterly trimmed mean during CPI transition

In a speech today, Michael Plumb, head of economic analysis at the RBA, said the central bank welcomes the introduction of a complete monthly CPI, noting that more frequent and comprehensive data will materially improve the timeliness of its inflation assessment.

However, Plumb cautioned that it will “take us some” time to understand the properties and seasonal patterns of the new monthly series. During the transition, the RBA will continue to “focus on the quarterly data”, particularly the quarterly trimmed mean measure, for forecasting and evaluating underlying inflationary pressures.

While maintaining its quarterly focus, the RBA has begun analyzing underlying inflation measures constructed from monthly data. Plumb said policymakers will assess potential biases, seasonal differences, responsiveness to economic conditions, and usefulness as a leading indicator.

The central bank intends to engage widely and communicate transparently before any shift in preferred measures in what he described as a gradual move toward a “post-quarterly CPI world.”

ECB’s Lagarde: Rates in “good place”, Europe can capture AI gains through application

Speaking at a conference in Washington, ECB President Christine Lagarde reiterated that Eurozone monetary policy is in a “good place,” repeating guidance that the current rate setting remains appropriate. The remarks signal that the ECB is not actively considering a policy shift, as inflation stabilizes and growth remains resilient.

Lagarde emphasized that the ECB will continue to assess incoming data and remain “agile”, but her tone suggested confidence in the existing stance. The message reinforces expectations of stability in near-term meetings, with policy adjustments contingent on material changes in inflation or financial conditions.

Turning to structural growth, Lagarde argued that Europe can still capitalize on artificial intelligence even if it does not dominate the development of cutting-edge models. She noted that history shows economic value often lies in broad application rather than invention alone, particularly in manufacturing and industrial sectors.

PBoC extends pause in LPR, USD/CNH downtrend slows

The People’s Bank of China left its benchmark lending rates unchanged, keeping the 1-year Loan Prime Rate at 3.00% and the 5-year LPR at 3.50%. The decision marks the tenth consecutive month of steady policy.

For now, policymakers are seen favoring targeted structural tools—supporting sectors such as technology and green energy—rather than deploying broad-based rate cuts. Holding benchmark rates also helps anchor the Yuan, which has been hovering near a 34-month high, buoyed in part by broad Dollar weakness.

USD/CNH has been trending lower since early 2025, reflecting persistent Dollar softness. However, technically, downside momentum appears to be fading, with bullish convergence emerging on D MACD. That suggests selling pressure may be losing traction in the near term.

Support may emerge near 200% projection of 7.2224 to 7.0840 from 7.1381 at 6.8613 to bring rebound. Firm break above 6.9105 resistance would indicate short-term bottoming and open the way toward the 55 D EMA (now at 6.9629).

Still, renewed broad-based Dollar weakness could quickly push the pair through 6.8613 toward 261.8% projection at 6.7758, and possibly revive medium term downside momentum along the way.

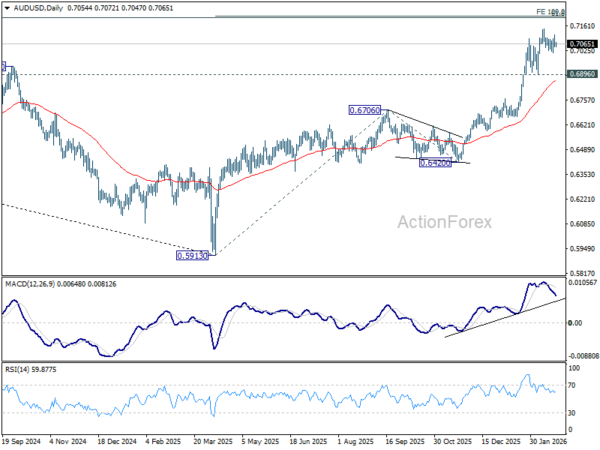

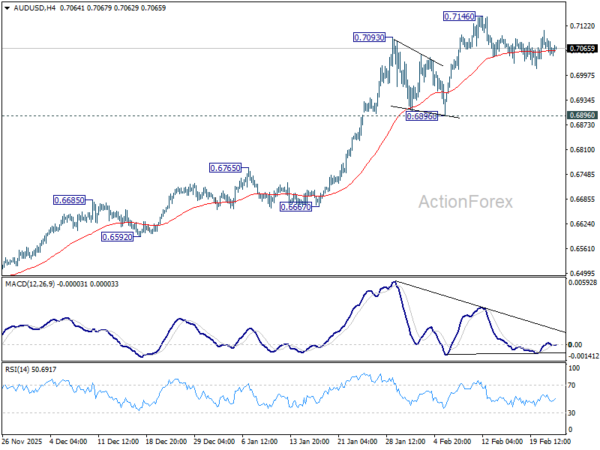

AUD/USD Daily Report

Daily Pivots: (S1) 0.7033; (P) 0.7072; (R1) 0.7096; More…

AUD/USD continues to gyrate in familiar range below 0.7146 and intraday bias remains neutral. Consolidations would continue and deeper retreat cannot be ruled out. But downside should be contained above 0.6896 support. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.