Global markets have entered a phase of heightened volatility as Middle East tensions transition into direct and widening regional conflict. Initial safe-haven flows rushed into Swiss Franc, pushing the currency to decade-highs against Euro. However, the move proved short-lived after rare and explicit pushback from Swiss National Bank.

In what traders quickly labeled a “verbal floor,” SNB warned of increased willingness to intervene to protect price stability. With Swiss inflation sitting at just 0.1%, authorities made clear they will not tolerate a safe-haven squeeze that risks tipping economy into deflation. The unprompted nature of the statement carried significant weight.

The message was effective. EUR/CHF stabilized after approaching key 0.9000 level — with some viewed as trigger zone for actual currency sales. Current CHF strength is seen as geopolitical spike rather than structural Eurozone deterioration back in 2010, and SNB appears determined to treat it as temporary battle of nerves.

The vacuum left by capped CHF strength has resulted in aggressive rotation into Dollar, which now stands as strongest performer. Canadian Dollar ranks second, supported by elevated energy prices. Sterling surprisingly holds third place. By contrast, Euro and Kiwi sit among weakest performers, together with Swiss Franc.

Equity markets reflect broader stress. European indexes, led by Germany’s DAX down roughly -2.4%. US futures are also pressured, with DOW down around -1.0%. Gold extended recent rebound and it’s now pressing 5,400 as hedge against systemic escalation. WTI crude, though moderating near 73 after initial spike, remains highly sensitive to developments around Strait of Hormuz.

In Europe, at the time of writing, FTSE is down -1.44%. DAX is down -2.41%. CAC is down -2.06%. UK 10-year yield is up 0.078at 4.311. Germany 10-year yield is up 0.044 at 2.700. Earlier in Asia, Nikkei fell -1.35%. Hong Kong HSI fell -2.14%. China Shanghai SSE rose 0.47%. Singapore Strait Times fell -2.09%. Japan 10-year JGB yield fell -0.047 to 2.065.

UK PMI manufacturing finalized at 51.7, strong output and export growth

UK PMI Manufacturing was finalized at 51.7 in February, easing marginally from January’s 17-month high of 51.8 but remaining firmly in expansion territory. The data suggest that the sector has made an “encouraging start” to 2026, with output rising at the fastest pace in 17 months as new orders improved across both “home and overseas markets”.

According to Rob Dobson at S&P Global Market Intelligence, growth in new export business reached a four-and-a-half year high, supported by stronger client confidence in North America, mainland China, the EU and the Middle East. The rebound in external demand has helped offset lingering weakness seen through much of last year, giving manufacturers renewed momentum.

Business optimism remains elevated, close to January’s recent peak, with nearly three-fifths of firms expecting to raise production over the coming year. While staffing levels continue to decline, the pace of job losses has moderated to the weakest in the current 16-month downturn, pointing to early signs of stabilization.

Eurozone PMI manufacturing finalized at 50.8, turning corner with broad-based recovery

Eurozone PMI Manufacturing was finalized at 50.8 in February, rising from January’s 49.5 and marking a 44-month high. The move above also the 50 threshold signals a return to expansion for the bloc’s factory sector.

The rebound appears increasingly broad-based. Greece (54.4) and Ireland (53.1) led growth, while Germany climbed to 50.9, its highest level in nearly four years and back in expansion for the first time in three-and-a-half years. Netherlands, Italy, France and Spain also hovered around or above the growth line, with Austria the only country still below 50. Among the major economies, Germany is now showing the fastest improvement in manufacturing conditions.

According to Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, the data point to a “broad-based recovery”, with six of eight surveyed countries now in growth territory. However, input price pressures accelerated for a fourth consecutive month and picked up sharply in February. While companies were able to pass on part of these increases, margins likely remained under strain.

Encouragingly, firms expressed growing optimism about future sales and production. Expectations for output improved further compared to January, suggesting confidence that demand conditions will strengthen in coming months.

Japan’s PMI manufacturing finalized at 53.0, output and orders post fastest gains in years

Japan’s PMI Manufacturing was finalized at 53.0 in February, rising from 51.5 in January and marking highest reading since May 2022. The data point to a clear acceleration in factory activity, with the sector extending its expansion and signaling that recovery momentum is broadening at the start of Q1.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, companies reported the quickest increases in output, new orders, employment and purchasing activity in more than four years. Business confidence also climbed to highest level since mid-2024, supported by expectations that global demand will continue to revive, particularly across technology and automotive sectors.

While input cost pressures eased slightly, price growth remained elevated by historical standards, partly reflecting impact of “weak Yen” on imported materials. Nevertheless, stronger demand could improve firms ability to pass on higher costs, helping to stabilize margins.

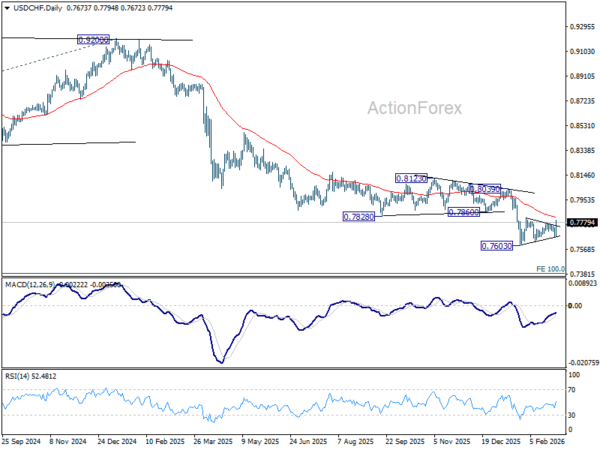

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7659; (P) 0.7705; (R1) 0.7737; More….

USD/CHF jumps sharply today, but upside is still limited below 0.7816 resistance, as well as 55 D EMA (now at 0.7818). Intraday bias stays neutral first, and further decline is till expected. Below 0.7671 will bring retest of 0.7603 low. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.