Panic has officially seeped into the European sessions. Crude prices are not just rising; they are re-accelerating, after Iran’s Revolutionary Guard warned that any ship entering the region would face a “serious response.” The death of Supreme Leader Ayatollah Khamenei on February 28 has removed the traditional diplomatic guardrails, leaving markets to fear a prolonged, high-intensity conflict.

The disruption has moved beyond the “price per barrel” to the “price of passage.” Charter rates for Very Large Crude Carriers from the Middle East to China have doubled in a week, hitting an all-time high of USD 423,000 per day.

And, it isn’t just the Strait. Retaliatory strikes against energy infrastructure in Saudi Arabia and the UAE have introduced a “physical destruction premium.” If these disruptions persist for more than 14 days, $100 oil—a figure once thought to be a relic of the past—could become the new baseline for 2026.

The most significant shift is occurring in interest rate expectations. The “war-induced” inflation spike has forced traders to abandon bets on a June rate cut. Fed fund futures now show a 67% probability of a hold, as central bankers cannot “look through” energy spikes that threaten to unanchor inflation expectations.

As a result, the “buy the dip” mentality that briefly appeared in the stock markets yesterday has been crushed by a sea of red. DAX (-3.3%) and DOW Futures (-700 pts) reflect a massive rotation out of risk.

In the currency markets, Dollar reigns supreme as the ultimate safe haven. Loonie follows as the second strongest, bolstered by surging oil, while Yen takes third place, following by a -3% slide in Nikkei.

Aussie and Kiwi are today’s laggards. Despite hawkish comments from the RBA head—which left the door open for a March hike—domestic policy is being overwhelmed by global risk aversion. Both the Euro and Sterling are caught in the crossfire, positioning in the middle of the pack.

In Europe, at the time of writing, FTSE is down -2.60%. DAX is down -3.30%. CAC is down -2.77%. UK 10-year yield is up 0.158 at 4.469. Germany 10-year yield is up 0.083 at 2.794. Earlier in Asia, Nikkei fell -3.06%. Hong Kong HSI fell -1.12%. China Shanghai SSE fell -1.43%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.068 to 2.133.

Eurozone CPI reaccelerates to 1.9% in Feb, as core and services pick up

Eurozone CPI accelerated from 1.7% year-on-year in January to 1.9% in February, exceeding expectations of 1.7%. Core CPI, which excludes energy, food, alcohol and tobacco, also firmed from 2.2% to 2.4%, above expectation of 2.2%, pointing to renewed underlying price pressures.

The composition of the increase suggests services remain primary driver. Services inflation rose to 3.4% from 3.2%, maintaining its position as the most persistent component.

Food, alcohol and tobacco held steady at 2.6%, while non-energy industrial goods picked up to 0.7% from 0.4%. Energy prices remained negative at -3.2%, though the drag eased compared to -4.0% in January.

ECB’s Lane warns Middle East war could spike inflation, hit growth

ECB Chief Economist Philip Lane warned that a prolonged conflict in the Middle East could significantly raise inflation in the Eurozone while undermining economic growth.

In an interview with the Financial Times, Lane said “Directionally, a jump in energy prices puts upward pressure on inflation, especially in the near-term, and such a conflict would be negative for economic activity.”

He emphasized that the ultimate impact would depend on the “breadth and duration” of the war.

Still, with current inflation running at 1.7%, below the ECB’s 2% target, a limited energy-driven uptick would not necessarily warrant immediate action. In particular, monetary policy cannot effectively counter short-term price swings as it operates with long lags.

RBA’s Bullock reopens door to March hike as oil risks mount

RBA Governor Michele Bullock delivered a distinctly hawkish message at the AFR Business Summit today, warning markets not to assume a March rate hold is a done deal. She stressed that the upcoming meeting is “live,” pushing back against expectations that policy decisions are effectively pre-set or limited to quarterly moves.

Bullock highlighted that inflation remains elevated at 3.8% while unemployment at 4.1% still reflects tight labor market conditions. The Board, she said, will be “actively looking” at whether it needs to “move more quickly”, explicitly discouraging the view that the RBA only adjusts rates at predictable intervals.

Central to her remarks was the risk of a prolonged oil price spike stemming from escalating Middle East tensions. While she emphasized that it is too early to quantify the impact, Bullock warned that a supply-driven shock could add to inflation pressures and, critically, influence inflation expectations — a development the RBA is “very alert to.”

WTI oil eyes key resistance at 79 as energy markets seized by panic

Oil prices surged again today, breaking through yesterday’s spike with aggressive upward acceleration. Markets are entering a state of panic following explicit threats from Iranian officials to “set fire” to any vessel attempting to navigate the Strait of Hormuz.

Ebrahim Jabbari, an adviser to the commander-in-chief of Iran’s Islamic Revolutionary Guard Corps (IRGC), told state TV: “Ships should not come to this region. They will certainly face a serious response from us.”

The Strait of Hormuz is a vital artery for the global economy, carrying approximately 20% of the world’s oil and gas. This flow has effectively ceased following a series of kinetic attacks on tankers over the last 72 hours.

Beyond the surge in raw commodity prices, the conflict has sent shipping overheads into uncharted territory. The cost of hiring a supertanker to move oil from the Middle East to China hit an all-time high on Monday, exceeding $400,000 (£298,300) per day. According to data from the London Stock Exchange Group, this represents a near-doubling of costs in just seven days.

Technically, WTI is now eyeing a key structural resistance level at 78.87. Decisive break there would confirm that the multi-year down trend from 131.82 (2022 high) has completed at 54.98. This supported by the double bottom reversal pattern (55.20, 54.98). In this case, WTI could extend current rise to 38.2% retracement of 131.82 to 54.98 at 84.33 next. In any case, near term outlook will remain bullish as long as 70.15 support holds.

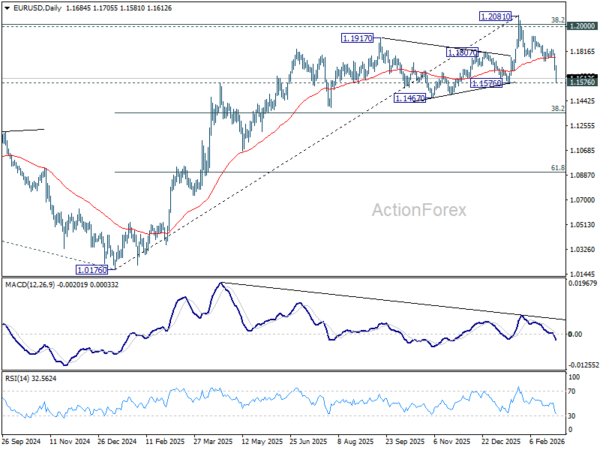

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1641; (P) 1.1719; (R1) 1.1765; More….

Intraday bias in EUR/USD remains on the downside, and immediate focus is now on 1.1576 structural support. Firm break there would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. For now, risk will stay on the downside as long as 1.1740 support turned resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.