The stalled US-Iran negotiations have shifted global “Fear Trade” focus toward the Strait of Hormuz’s role as a critical fertilizer bottleneck. With 35% of global Urea exports at risk, benchmark prices have surged, creating a “pincer effect” for the Australian Dollar. Despite high commodity prices, rising input costs for the 2026 winter crop are neutralizing the AUD’s traditional commodity boost, while bolstering the US Dollar’s “safe-haven” status as Fed rate hike odds jump to 30%.

The Hormuz Bottleneck: Beyond Oil

While oil prices are staying in consolidations, the market is waking up to the fact that the Strait of Hormuz is a vital artery for the agricultural complex. Qatar, Saudi Arabia, and Iran account for nearly one-third of the world’s seaborne Urea. The current stalemate has turned Urea into a front-page risk factor, with benchmark NOLA prices jumping 25-30% since late February.

This is a “double whammy” for the sector: even if shipping remains open, the skyrocketing cost of natural gas—the primary feedstock for nitrogen—is creating an alarming price floor for global food production.

The “Pincer Effect” on the Aussie Dollar

For the AUD, the “fertilizer-to-food” pipeline has turned toxic. Normally, high commodity prices are a tailwind for the Aussie, but the current crisis is squeezing farmer margins to the breaking point.

As Australia prepares for the 2026 winter crop, the prohibitive cost of seeding could lead to significantly lower export volumes later this year. With the “make or break” window closing in late May, the AUD has become the week’s worst performer, lagging behind even its commodity peers, the Loonie and Kiwi.

Fed Pivot: From Easing to Tightening?

On the other hand, the impact on the US interest rate trajectory is the opposite. Futures markets have effectively priced out any hope for a Fed rate cut in 2026. Instead, the odds of a final rate hike by year-end have surged to nearly 30%.

As global supply chains fracture, Dollar is benefiting from its relative self-sufficiency in nitrogen production (driven by domestic shale gas), positioning the greenback as the “cleanest shirt in the dirty laundry.”

The “Winners vs. Losers”

Market activity today reflects a pause in momentum in currencies. Major FX pairs are largely confined within yesterday’s ranges. For the week so far, Dollar is gaining relative strength as investors gravitate toward economies with greater energy and production self-sufficiency. In contrast, commodity currencies are failing to benefit from higher prices. Aussie is particularly weak, as rising fertilizer and fuel costs threaten to erode agricultural profitability and potentially reduce future export volumes.

In Asian, at the time of writing, Nikkei is down -0.78%. Hong Kong HSI is down -2.03%. China Shanghai SSE is down -0.88%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield is up 0.02 at 2.275. Overnight, DOW rose 0.66%. S&P 500 rose 0.54%. NASDAQ rose 0.77%. 10-year yield fell -0.064 to 4.328.

Silver Defies ‘Cried Wolf’ Headlines: Why Bullish MACD Signals Signals Recovery Towards $80

Silver is exhibiting a classic “Cried Wolf” effect. Despite Tehran’s blunt rejection of the latest 15-point peace proposal, Silver has refused to buckle, maintaining a resilient floor above $70. Read more.

RBA Warns of ‘Restrictive’ Shift: Why Rising Neutral Rates and Petrol Shocks Could Trigger More Hikes

Assistant Governor Christopher Kent just delivered a sobering update on the RBA’s path forward. While global uncertainty usually cools rates, the “Supply Shock” from the Middle East is having the opposite effect—pushing Neutral Rates higher and keeping the pressure on Australian households. Read more.

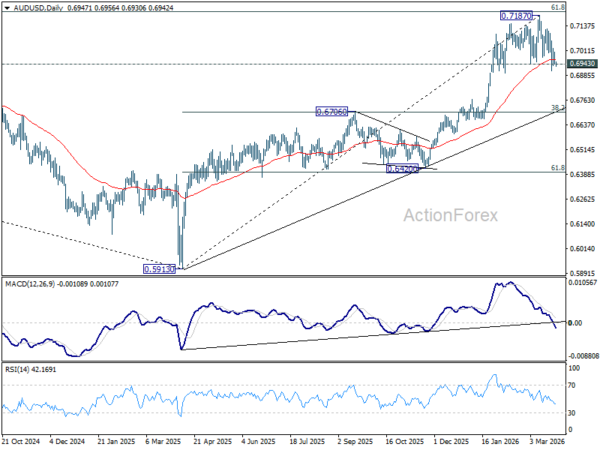

AUD/USD Daily Report

Daily Pivots: (S1) 0.6925; (P) 0.6965; (R1) 0.6987; More…

AUD/USD continues to press 0.6943 key support but there is no clean break yet. Intraday bias remains neutral first. On the downside, decisive break of 0.6943 should confirm rejection by 0.7206 key fibonacci resistance. That would set up deeper correction to the whole up trend from 0.5913, and target 38.2% retracement of 0.5913 to 0.7187 at 0.6700. Nevertheless, break of 0.7061 minor resistance will retain near term bullishness, and bring retest of 0.7187 high first.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.