Risk aversion has returned to global markets following US President Donald Trump’s escalation signals on the Iran war, but a more important shift is unfolding in oil markets. While oil prices surged after the address, the internal dynamics are far more telling: Brent is struggling below key resistance at $113.93, while WTI has broken through $107.29 and pushed above $110, driving a sharp collapse in the Brent-WTI spread into what can be described as a “stress signal” zone.

This development suggests that the market could now be pricing a “supply shift”, not just a price spike. For the past month, Brent has carried the “war premium” as a regional benchmark for the Middle East conflict. However, the current catch-up play in WTI indicates that traders are beginning to discount the availability of waterborne crude entirely. This is no longer about the cost of oil; it is about the deliverability risk associated with barrels that must transit increasingly contested maritime corridors.

In the past decade, Brent maintains a $3–$6 premium over WTI, reflecting transportation costs and its role as the global seaborne benchmark. This spread has only briefly flipped or hit parity during periods of acute disruption—such as the 2011 US shale bottlenecks and isolated logistical dislocations.

What makes the current episode different is the underlying driver. This is not a demand shock or pipeline bottleneck—it is a “deliverability crisis” in the making. The spread compression is acting as a “stress signal” that markets are beginning to prioritize access and security of supply over geographic benchmarks.

At the core is what can be described as the “safety of the barrel” theory. Brent represents waterborne crude, much of it tied to supply routes vulnerable to disruption in the Strait of Hormuz. In a scenario involving tanker attacks or a full blockade, the value of Brent as a tradable asset becomes uncertain—not just in price, but in physical delivery. Traders holding Brent are not just exposed to price volatility but to the possibility that cargoes cannot be delivered safely or on time. This is fundamentally different from traditional war premium pricing.

By contrast, WTI could be increasing treated as the “safe supply” benchmark. US crude, produced and stored domestically, is insulated from direct geopolitical disruption in the Middle East. As a result, traders are rotating into WTI as triggered by positioning ahead of potential weekend escalation. With Trump signaling an intensified campaign that would bring Iran back to “Stone Age”, and markets heading into a long weekend, traders are front-running massive weekend disruption. The logic is straightforward: if supply routes are hit while markets are closed, the scramble for alternative supply will begin immediately.

In such a scenario, global buyers—particularly in Asia—would pivot toward US exports, driving demand for WTI-linked barrels. The result would be further spread compression, and potentially a full inversion where WTI trades above Brent. If that flip on spread occurs, it would mark a profound shift in market structure. It would signal that oil is no longer being priced based on origin, but on security and deliverability. In effect, WTI would replace Brent as the global reference for “reliable” supply.

An even more extreme scenario cannot be ruled out. If WTI were to break above 120 ahead of Brent, it would indicate that the crisis has moved beyond regional disruption into a global supply breakdown. This would suggest that US spare capacity—the world’s safety valve—is being overwhelmed too. In that case, the implications would be severe. The global oil market would lose its stabilizing anchor, raising the risk of a systemic energy shock reminiscent of past crises. The current spread compression may therefore be more than a technical move—it may be an early warning of deeper structural stress.

In the currency markets, Dollar is currently the best performer for the day so far, followed by Loonie, and then Yen. Aussie is the worst, followed by Kiwi, and then Sterling. Euro and Swiss Franc are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.72%. DAX is down -2.59%. CAC is down -1.54%. UK 10-year yield is up 0.083 at 4.859. Germany 10-year yield is up 0.060 at 3.049. Earlier in Asia, Nikkei fell -2.38%. Hong Kong HSI fell -0.70%. China Shanghai SSE fell -0.74%. Singapore Strait Times fell -0.57%. Japan 10-year JGB yield rose 0.091 to 2.395.

US Jobless Claims Fall to 202k, Labor Market Remains Tight

US jobless claims fell to 202k, beating expectations and signaling a still-tight labor market. While continuing claims edged higher, the broader trend remains stable, pointing to resilience in employment conditions. Read more.

Swiss CPI Rises to 0.3% yoy, But Underlying Inflation Stays Soft

Swiss inflation remained subdued in March, with CPI missing expectations and core prices flat. While imported costs rose on higher energy prices, weak domestic inflation continues to cap overall price pressures. Read more.

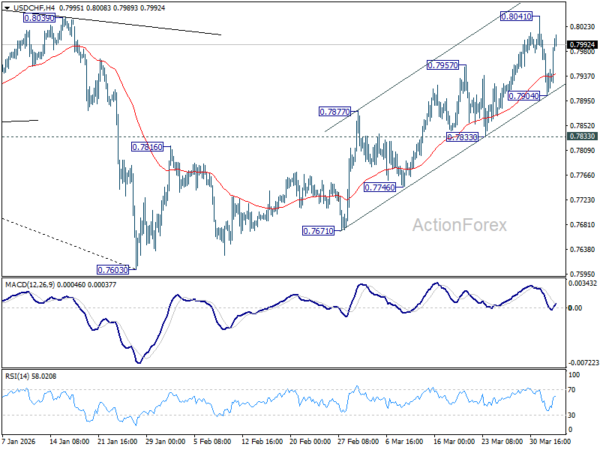

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7895; (P) 0.7953; (R1) 0.8001; More….

Range trading continues in USD/CHF below 0.8041 temporary top and intraday bias stays neutral. Further rally is expected with 0.7833 support intact. On the upside, break of 0.8041 will resume the whole rally from 0.7603, and target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, decisive break of 0.7833 support will argue that the rebound has completed, and turn bias back to the downside for deeper fall.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8088) will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.