Dollar and oil are rising together today as ceasefires extend—but conflict persists. Despite a three-week extension of the Israel–Hezbollah truce and the ongoing “indefinite” pause in US–Iran conflicts, markets are increasingly focused on what is still happening rather than what has been paused. Maritime seizures, naval blockades, and localized escalations continue to define the situation, keeping risk elevated and supply disruption concerns firmly in place.

The US has maintained its naval blockade of Iranian ports, while Iran’s IRGC continues to seize vessels in the Strait of Hormuz. This evolving maritime standoff is reinforcing the idea that the ceasefire is a delay, not a resolution. As a result, oil prices are extending higher, reflecting expectations of prolonged disruption.

This backdrop is supporting Dollar strength. Rising oil prices are feeding into inflation expectations, reinforcing the higher-for-longer rate outlook while also attracting safe-haven demand. The combination of yield support and geopolitical uncertainty is keeping the Dollar bid, even as broader market conviction remains limited.

Euro, by contrast, is emerging as the weakest link. This week’s PMI data shows the Eurozone has already slipped into contraction, with services activity deteriorating sharply. Germany’s downgrade of its growth outlook, from 1.0% to just 0.5% in 2026, adds to the concern that the region is particularly exposed to the energy shock. If markets are moving toward a stagflation narrative, Europe appears to be leading the downturn.

Yen remains soft but is finding some support from intervention risks. Japan’s Finance Minister has reiterated warnings of “decisive action,” and traders remain cautious about pushing USD/JPY beyond the 160 level. This has limited downside momentum in Yen despite the broader Dollar strength.

Currency performance for the week reflects this fragmented environment. Dollar leads, followed by oil-supported Canadian Dollar. Euro is the weakest, with Yen and Swiss Franc also under pressure. Sterling, Aussie and Kiwi sit in the middle, lacking clear directional drivers.

In Asia, at the time of writing, Nikkei is up 0.85%. Hong Kong HSI is down -0.14%. China Shanghai SSE is down -0.68%. Singapore Strait Times is down -0.51%. Japan 10-year JGB yield is up 0.015 at 2.441. Overnight, DOW fell -0.36%. S&P 500 fell -0.41%. NASDAQ fell -0.89%. 10-year yield rose 0.029 to 4.323.

Silver Fails at $84—Will Oil and Dollar Strength Accelerate a Move to $60?

Japan’s Core Inflation Rises to 1.8% in March, Core-Core Ticks Down

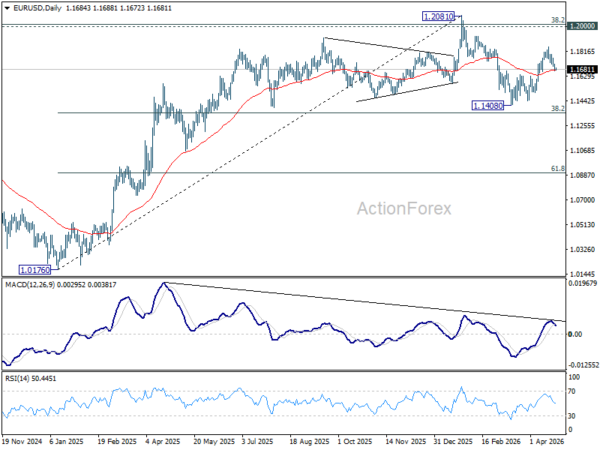

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1663; (P) 1.1691; (R1) 1.1712; More….

EUR/USD edged lower today but stays above 1.1662 support. Intraday bias remains on the upside and further rise is still in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.