Geopolitics is once again dominating global markets today, with investors rapidly shifting between optimism over a potential US-Iran peace framework and fears of renewed escalation. Earlier in the session, risk appetite improved sharply after reports suggested Washington and Tehran were nearing a one-page, 14-point memorandum of understanding designed to end the war and establish a framework for broader nuclear negotiations.

The initial reaction was significant. Brent crude briefly broke below the psychologically important $100 level as traders aggressively unwound part of the geopolitical risk premium built during weeks of conflict around the Strait of Hormuz. Dollar also came under broad selling pressure, while Gold rebounded strongly. The move was reinforced after a Pakistan government official reportedly said that the prospect of a proposal to end the war was “very likely” in the coming days, while Iran’s foreign ministry confirmed it was “evaluating” the US proposal.

However, market optimism turned into caution after US President Donald Trump sharply raised the stakes later in the day. In a Truth Social post, Trump warned that Iran would face bombing “at a much higher level and intensity than it was before” if Tehran rejected the deal. He simultaneously stated that the war “will be at an end” if Iran accepts the proposals and allows the Strait of Hormuz to reopen “to all.” The rhetoric effectively transformed the market narrative from de-escalation into a binary geopolitical outcome: either a comprehensive peace deal or a renewed escalation cycle.

That shift explains why the earlier market optimism became more restrained as the session progressed. Oil prices recovered part of their losses, while broader risk sentiment turned more cautious. Markets generally dislike uncertainty more than negative outcomes themselves, and Trump’s comments highlighted how fragile the current diplomatic momentum still is.

One key concern is the internal political structure inside Iran. While diplomats and the foreign ministry may be evaluating the proposal, the Islamic Revolutionary Guard Corps still controls much of the military infrastructure surrounding Hormuz, including missile batteries and fast-attack naval units. It is being questioned whether Iran’s diplomatic leadership can actually enforce a ceasefire if elements within the IRGC oppose the proposed framework.

The issue is particularly sensitive because some factions inside Iran could view a broad 14-point agreement as a strategic surrender rather than a negotiated settlement. That creates a significant “veto risk,” where even meaningful diplomatic progress may not guarantee operational de-escalation on the ground.

Another uncertainty surrounds Israel’s position. Any durable US-Iran arrangement has required at least tacit Israeli acceptance. If Israel remains publicly skeptical or openly critical of the proposed framework, traders may quickly reduce confidence that the agreement can stabilize the region sustainably.

For now, markets are clearly trying to price both possibilities simultaneously. Dollar remains the weakest major currency on the day, followed by Loonie and Swiss Franc, while Kiwi, Yen, and Aussie are outperforming on improved risk appetite and falling oil prices. But beneath the surface, while optimism exists, confidence remains conditional.

In Europe, at the time of writing, FTSE is up 2.24%. DAX is up 2.16%. CAC is up 3.11%. UK 10-year yield is down -0.103 at 4.961. Germany 10-year yield is down -0.065 at 2.999. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 1.22%. China Shanghai SSE rose 1.17%. Singapore Strait Times rose 0.14%.

Gold Roars Back as Peace Hopes Crush Dollar

Brent Breaks Below $100 as US and Iran Near Peace MOU to End War

Will $80K Become Bitcoin’s New Floor and Trigger Another ETF Buying Wave?

US ADP Jobs Growth Accelerates to 109k as Hiring Strengthens at Small and Large Firms

Eurozone PPI Surges 3.4% mom as Energy Costs Drive Sharp Producer Inflation

Eurozone PMI Falls Into Contraction as Energy Shock Hits Services Hard

UK PMI Services Climbs to 52.7 as Inflation Signals Strengthen

NZ Labor Data Gives RBNZ Room to Stay on Hold

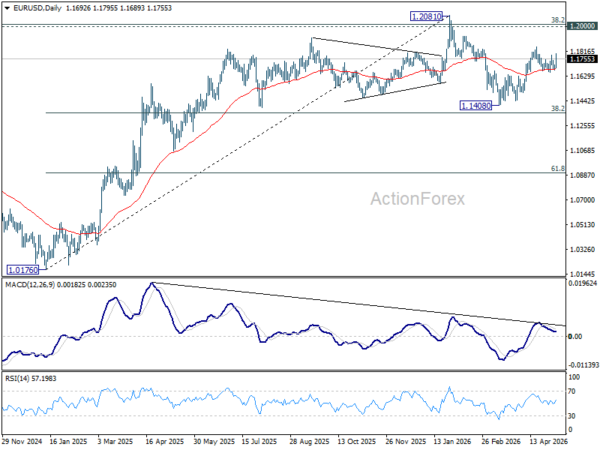

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1695; (R1) 1.1713; More….

EUR/USD is still bounded below 1.1848 resistance despite today’s rebound. Intraday bias remains neutral at this point. With 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.