Markets moved into a more cautious tone today as the deadlock in US-Iran peace negotiations continued to drag on, while renewed volatility in UK government bonds added another layer of political and fiscal uncertainty. However, despite the rising tension, broader market behavior still stopped short of outright panic.

Brent crude remained elevated near $103 after earlier surging above $105 as traders continued pricing persistent disruption risks around the Strait of Hormuz. Dollar initially rebounded broadly following President Donald Trump’s rejection of Iran’s latest peace proposal as “TOTALLY UNACCEPTABLE,” but follow-through momentum faded as the session progressed. US stock futures also recovered from earlier declines and were pointing to a broadly flat Wall Street open, highlighting that investors were merely becoming uneasy rather than fully risk-averse.

The diplomatic standoff itself appears increasingly entrenched. Iranian state media framed Tehran’s latest response as a rejection of what it described as a US demand for “surrender.” Iran’s counterproposal reportedly included demands for war reparations, recognition of full Iranian sovereignty over the Strait of Hormuz, the lifting of sanctions, and the release of frozen Iranian assets. President Masoud Pezeshkian also adopted a defiant tone over the weekend, insisting that negotiations “do not mean surrender or retreat.”

Markets had previously hoped for some form of controlled de-escalation after weeks of ceasefire discussions. Instead, the latest exchange suggests both sides remain fundamentally divided on core issues including sanctions, nuclear restrictions, and control over Hormuz. Nevertheless, investors still believe some form of eventual diplomatic framework can emerge, even if negotiations remain stalled in the near term.

At the same time, another source of nervousness emerged from the UK. British bond markets came under renewed pressure today, with the 10-year gilt yield climbing back toward the 5% level. The move reflects growing investor concern over political instability following Labour’s heavy losses in last week’s local elections.

Prime Minister Keir Starmer is reportedly facing mounting internal pressure to resign, with media reports suggesting more than 40 Labour MPs have privately called for him to step down. Potential successors including Wes Streeting and Andy Burnham are already being discussed publicly. Markets appear increasingly concerned that either a leadership change or a weakened government could eventually push Labour toward more expansionary fiscal policies.

The key market fear is not immediate political collapse, but rather a gradual erosion of fiscal credibility. Investors worry that efforts to stabilize Labour politically could involve looser fiscal rules, higher government borrowing, or more populist spending measures. Unless Starmer can decisively stabilize his leadership position, or Chancellor Rachel Reeves can reassure markets that fiscal discipline will remain intact, pressure on Gilts may continue.

Interestingly, Sterling itself remained relatively calm despite the bond market volatility. That divergence suggests markets are currently treating the UK as a riskier fixed-income story rather than a full-blown currency crisis. In FX markets today, Loonie is the strongest performer, supported by elevated oil prices, followed by Dollar and Aussie. Swiss Franc is the weakest, followed by Kiwi and Yen,. Overall, today’s market tone reflects controlled nervousness rather than outright panic.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is down -0.30%. CAC is down -0.88%. UK 10-year yield is up 0.09 at 5.002. Germany 10-year yield is up 0.034 at 3.041. Earlier in Asia, Nikkei fell -0.47%. Hong Kong HSI rose 0.05%. China Shanghai SSE rose 1.08%. Singapore Strait Times rose 0.42%. Japan 10-year JGB yield rose 0.049 to 2.525.

Silver Refuses to Break Despite Dollar Rebound, But Bulls Still Need One More Catalyst

BoE’s Greene Says Waiting on Iran War Is Better Than Rushing Rate Hikes

China Inflation Heats Up as PPI Hits 45-Month High

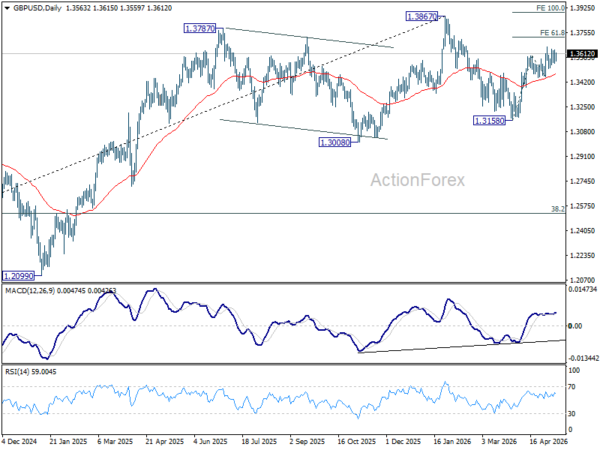

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3568; (P) 1.3602; (R1) 1.3659; More…

Range trading continues in GBP/USD and intraday bias stays neutral for the moment. With 1.3453 support intact, further rise is expected. On the upside, break of 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).