Dollar strengthened broadly today as rising oil prices and firmer-than-expected US inflation data continued pushing markets toward a more hawkish Federal Reserve outlook. However, the overall move remained relatively measured as broader risk sentiment stayed resilient, with investors still reluctant to fully embrace defensive positioning ahead of the Trump-Xi summit later this week.

Oil prices remained a key driver. Brent crude climbed back above %107 while WTI traded above %100 as stalled US-Iran peace negotiations continued sustaining geopolitical risk premium in energy markets. Nevertheless, both benchmarks remain largely trapped within the broad consolidation ranges established after the sharp March spike, suggesting traders still see the Hormuz crisis as unresolved but not yet spiraling into a full-scale crisis. The eventual direction of the Strait of Hormuz situation may depend heavily on the outcome of Thursday’s Trump-Xi summit.

The second major support for Dollar came from US inflation data. April CPI showed headline inflation accelerating from 3.3% yoy to 3.8% yoy, while core CPI rose from 2.6% yoy to 2.8% yoy, both slightly above expectations. The firmer core readings in particular raised concern that energy-driven inflation pressures may now be spreading more broadly into underlying consumer prices. Fed fund futures subsequently pushed further toward pricing no rate cuts this year, while implied odds of a rate hike rose toward 28%.

Still, Dollar’s rally remained restrained overall. US equities held relatively firm, and broader risk appetite continued receiving support from ongoing optimism surrounding AI-related investment themes and semiconductor demand. The market tone suggests investors are pricing higher inflation risk without yet fully shifting toward outright crisis positioning.

Sterling was among the weakest major currencies earlier in the session as UK political concerns intensified following the first ministerial resignation calling for Prime Minister Keir Starmer to step down. Markets had already become uneasy after Labour’s poor local election results last week, but Miatta Fahnbulleh’s resignation turned the leadership crisis into a more immediate market concern. However, the Pound later stabilized after senior Cabinet ministers rallied behind Starmer following a critical internal meeting where he insisted he would not resign voluntarily without a formal leadership challenge.

Yen also experienced significant intraday volatility. Initially, the currency weakened alongside rising oil prices, continuing the recent pattern where higher energy costs pressure Japan’s import-heavy economy. However, Yen later rebounded strongly after US Treasury Secretary Scott Bessent reaffirmed that both the United States and Japan believe excessive currency volatility is undesirable.

Speaking after meeting Prime Minister Sanae Takaichi, Bessent said Washington remained in close contact with Japanese authorities on exchange rate developments and expressed confidence that BOJ Governor Kazuo Ueda would successfully avoid falling behind the curve on inflation. The remarks were interpreted by markets as broad US support for Japan’s recent Yen-buying intervention efforts. The comments followed similar remarks earlier from Japanese Finance Minister Satsuki Katayama, who confirmed close coordination with Washington on currency market developments.

In the currency markets, Dollar is the strongest one for the day so far, followed by Kiwi, and then Loonie. Sterling is the worst, followed by Swiss Franc, and then Aussie. Euro and Yen are positioning in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.30%. DAX is down -0.95%. CAC is down -0.57%. UK 10-year yield is up 0.105 at 5.11. Germany 10-year yield is up 0.049 at 3.092. Earlier in Asia, Nikkei rose 0.52%. Hong Kong HSI fell -0.22%. China Shanghai SSE fell -0.25%. Singapore Strait Times rose 0.07%. Japan 10-year JGB yield rose 0.019 to 2.544.

US CPI Hits Highest Since 2023, Core Inflation Beats Expectations

EUR/GBP Surges as Markets Price “Zombie Government” Risk as Starmer Crisis Deepens

German ZEW Sentiment Rises to -10.2, But Economy Still Burdened by Energy Shock

BoJ Summary Shows Growing Support for Near-Term Rate Hike

Australia NAB Survey Shows Cost Growth Jumps to 4.5% as Margin Squeeze Intensifies

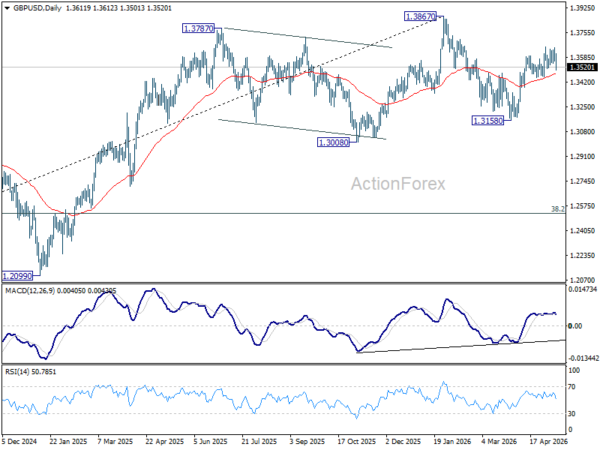

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3603; (R1) 1.3656; More…

GBP/USD falls notably today but stays above 1.3453 support. Intraday bias remains neutral and further rally is in favor. On the upside, firm break of 1.3657 will resume the rally fro 1.3158 to retest 1.3867 high. However, decisive break of 1.3453 will argue that the rebound has already completed, and turn bias to the downside for retesting 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).