Markets are still waiting for the real signals. As US President Donald Trump’s two-day summit with Chinese President Xi Jinping began in Beijing today, investors largely avoided making aggressive bets, preferring instead to wait for the kinds of concrete announcements and joint language that typically emerge near the end of high-level diplomatic visits. Beneath the surface calm, however, the summit could shape the direction of everything from oil prices and AI stocks to inflation expectations and global trade stability.

The biggest issue remains the Strait of Hormuz crisis.

Washington is reportedly asking Beijing to use its enormous economic leverage over Iran to help reopen the vital shipping corridor. China is currently the largest buyer of Iranian oil, giving it influence over Tehran that no other governments possess. Trump may be willing to offer selective sanctions relief for Chinese firms tied to Iranian shipments if Beijing pressures Iran toward de-escalation and maritime reopening.

Markets are watching closely for any joint language mentioning “maritime stability” or “de-escalation in the Gulf.” Such wording would likely be interpreted as a major diplomatic breakthrough and could trigger a sharp fall in oil prices from current elevated levels near $106 Brent. Airline and logistics shares, which have suffered under rising fuel costs, would likely rally strongly, while Dollar could weaken as safe-haven demand fades.

But the summit is about far more than oil alone.

One of the biggest surprises of the visit was Nvidia CEO Jensen Huang joining the delegation alongside Elon Musk and Apple CEO Tim Cook. Their presence intensified speculation that AI chip restrictions may be part of a broader geopolitical negotiation framework involving rare earth exports, technology access, and cooperation over Iran. There is possibility of selective carve-outs on advanced semiconductor exports if China helps stabilize the Hormuz situation or loosens restrictions on critical minerals.

Such a development would likely provide another major boost to US technology shares, particularly as NASDAQ continues extending its record-setting rally on AI optimism despite elevated geopolitical tensions.

Another important area of discussion is the proposed US-China “Board of Trade” framework — a permanent institutional mechanism designed to manage disputes and reduce the risk of repeated tariff escalations. While probably less immediately market-moving than oil or semiconductor announcements, institutional investors would likely welcome any framework that increases long-term trade predictability between Washington and Beijing.

Meanwhile, Kevin Warsh was officially confirmed by the Senate as the next Chair of the Federal Reserve in a historically partisan 54–45 vote. Warsh is expected to formally assume the role on May 14 ahead of his first policy meeting in June. Markets continue monitoring the leadership transition carefully following this week’s hotter-than-expected CPI and PPI data, which further strengthened expectations that the Fed may need to maintain restrictive policy for longer.

In currency markets, the overall picture remains unusually mixed rather than purely risk-on or risk-off. Aussie is now the strongest major currency this week thanks to resilient risk appetite and AI-driven optimism. Dollar stayed supported by rising Fed expectations after hot inflation data. Loonie benefited from elevated crude prices. On the other hand, Sterling remained pressured by Britain’s political instability, and Yen continued struggling as intervention effects faded.

In Asia, at the time of writing, Nikkei is down -0.69%. Hong Kong HSI is up 0.36%. China Shanghai SSE is down -0.76%. Singapore Strait Times is down -0.38%. Japan 10-year JGB yield is up 0.037 at 2.630. Overnight, DOW fell -0.14%. S&P 500 rose 0.58%. NASDAQ rose 1.20%. 10-year yield rose 0.02 to 4.48.

Fed’s Kashkari Reinforces Hawkish Stance Amid Iran-Driven Inflation

Collins: Fed Should Hold for Now but Hike Risk Has Increased

ECB’s Lane Lays Out Case for June Hike Amid Global Energy Shock

BoE’s Mann Warns Bond Market Fragility Matters for Future Rate Hikes

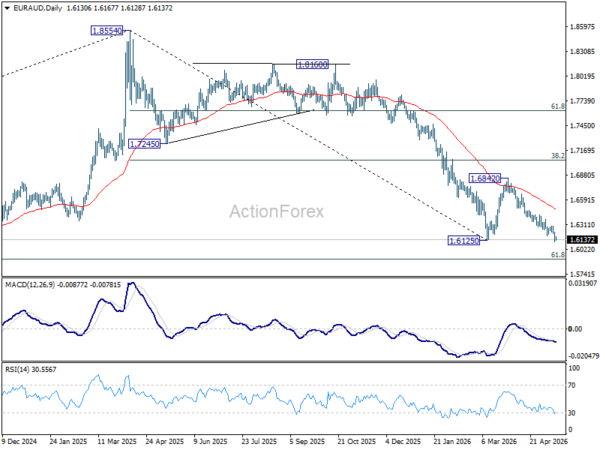

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6082; (P) 1.6153; (R1) 1.6196; More…

Intraday bias in EUR/AUD stays on the downside at this point. Decisive break of 1.6125 will resume larger fall from 1.8554. Next target is 1.5913 fibonacci level. Nevertheless, break of 1.6293 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.6491).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7039) holds, even in case of strong rebound.