Risk sentiment stabilized somewhat today as Brent crude eased back below $109 and US equity futures pointed to a modest recovery at the open. Still, the broader market mood remains tense as investors continue grappling with elevated global bond yields and persistent uncertainty surrounding the Middle East conflict. While oil prices stepped back temporarily, Treasury yields remained firmly near cycle highs, signaling that underlying financial conditions continue tightening aggressively.

The bond market is increasingly becoming the dominant macro concern. US 10-year Treasury yield recently surged above 4.65%, while the 30-year yield pierced 5.15%, reaching its highest level since 2007. Some market participants warn that if the 10-year yield breaks decisively above 4.75%, markets could enter a deeper structural rotation phase, with capital shifting more aggressively out of equities and into bonds. Near-5% risk-free yields would significantly challenge the valuation support behind recent equity resilience, particularly in growth and AI-related sectors.

There is also growing concern that the bond market itself may begin forcing policy adjustments. A sustained move toward 5% on the 10-year yield could increase pressure on the Federal Reserve to abandon any lingering easing bias and potentially reopen discussions about further tightening if inflation remains sticky. At the same time, elevated yields and persistently high oil prices could intensify pressure on the White House to pursue a diplomatic resolution to the Middle East conflict in order to cool energy markets and ease broader inflation risks.

Meanwhile, attention now turns to the release of FOMC minutes from the April meeting later today. Markets are bracing for a notably hawkish tone following the unusually divided decision to keep rates steady at 3.50%–3.75%. One Fed member, Governor Stephen Miran dissented in favor of a cut. Three influential regional presidents — Neel Kashkari, Lorie Logan, and Beth Hammack — opposed the statement’s easing bias. Investors will closely examine whether concerns about inflation persistence and elevated energy prices were more widespread within the committee than previously understood.

If the minutes confirm that a growing faction inside the Fed is shifting toward a neutral or even hawkish bias, the recent bond rout could extend further. Higher Treasury yields would likely strengthen Dollar further while weighing on equities, Gold, and other non-yielding assets. Nvidia earnings later today also add another layer of importance, particularly given the technology sector’s sensitivity to rising discount rates.

In currency markets, Sterling is currently the strongest performer of the week so far despite softer-than-expected UK CPI data, suggesting markets still expect the Bank of England to maintain a relatively restrictive stance. Kiwi and Dollar also outperformed, while Swiss Franc lagged sharply as rising global yields reduced the attractiveness of low-yielding safe havens. Aussie also remained weak, signaling that broader risk appetite has yet to fully recover despite today’s modest stabilization.

On the trade front, markets received some constructive news after the European Union finalized the legislative text of its long-delayed trade agreement with the United States. The breakthrough reduces the risk of an escalating transatlantic trade conflict after US President Donald Trump had threatened major tariffs if Brussels failed to implement the deal before the July 4 deadline. European Commission President Ursula von der Leyen said the agreement would help ensure “stable, predictable, balanced, and mutually beneficial transatlantic trade.”

Bitcoin Wanted $80K to Be a Launchpad, It Becomes an Exit Door Instead

10-Year Yield Eyes 4.75 After Violent Breakout, Opening Risk Toward 5%

Eurozone Inflation Accelerates to 3.0% as Energy Costs Push Headline Higher

UK Inflation Slows Sharply to 2.8%, Easing Immediate Pressure on BoE

China’s PBoC Holds Key Lending Rates Steady as Policymakers Avoid Rush to Ease

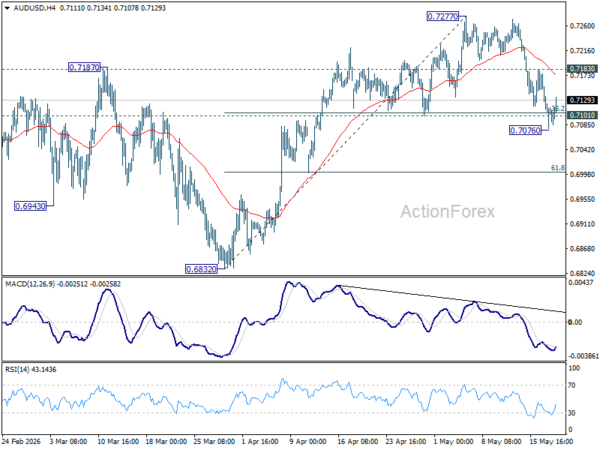

AUD/USD Daily Report

AUD/USD dipped to 0.7076 but quickly recovered. Intraday bias stays neutral first. On the upside, above 0.7183 minor resistance will suggest that pullback from 0.7277 has completed. Intraday bias will be back on the upside for retesting this high. However, decisive break of 0.7076 will bring deeper decline back towards 0.6832 support.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.