Markets began the week trading as if the Strait of Hormuz is already reopening — even though the final agreement has not yet been signed. Investors rushed into a full-scale “peace dividend” trade after reports suggested the US and Iran are edging closer toward a framework agreement that could end the conflict, restore shipping through Hormuz, and dramatically reduce the risk of a prolonged global energy shock.

The reaction across markets was immediate and aggressive. Oil prices collapsed as traders rapidly unwound geopolitical supply premiums. Brent crude plunged more than -4.5%, crashing through the $100 threshold and sliding to $95 a barrel as fears of a catastrophic energy squeeze eased. The collapse in oil immediately fed through into lower inflation expectations, softer global yields, and a powerful risk-on rally across equities.

Asian markets led the celebration. Japan’s Nikkei 225 exploded 2.9% higher, blasting through 65,000 as energy-importing economies emerged as the biggest beneficiaries of the de-escalation trade. European stocks climbed to their highest levels in more than two months as investors priced a world with lower oil prices, reduced inflation pressure, and less need for central banks to keep policy aggressively tight.

The FX market told a similar story, though with more caution underneath the surface. Dollar weakened broadly as safe-haven demand eased, while Canadian Dollar sank alongside oil prices. Yen also underperformed as traders rotated back into risk assets. Aussie led gains, followed by Sterling and Kiwi, as lower energy costs improved the broader global growth outlook.

But beneath the relief rally, skepticism has not disappeared. Precious metals rose modestly only, suggesting investors are still unwilling to fully abandon geopolitical hedges.

And on the diplomatic side, negotiators continue sending mixed signals. US President Donald Trump warned that any agreement would either be “great and meaningful, or there will be no deal at all,” while Marco Rubio said Washington still has “alternatives” if talks fail.

Iran also poured some cold water on the optimism. Foreign ministry spokesperson Esmaeil Baghaei acknowledged that progress had been made on many issues, but stressed that this does not mean “we’re close to signing an agreement.”

In other words, markets are already trading the reopening of Hormuz before negotiators themselves are willing to declare victory.

That tension may define the next stage of the move. If the deal is finalized and oil continues collapsing, markets could push even deeper into the peace-dividend trade. But if negotiations break down at the final stage, the speed of the current repricing suggests volatility could return just as violently in the opposite direction.

Gold and Silver Bounce, but Traders Still Need Proof on Hormuz Normalization

Hawkish RBNZ, Fragile Aussie: Why AUD/NZD Could Break Hard This Week

RBNZ Shadow Board Backs Hold at 2.25%, Three Call for Immediate Hike

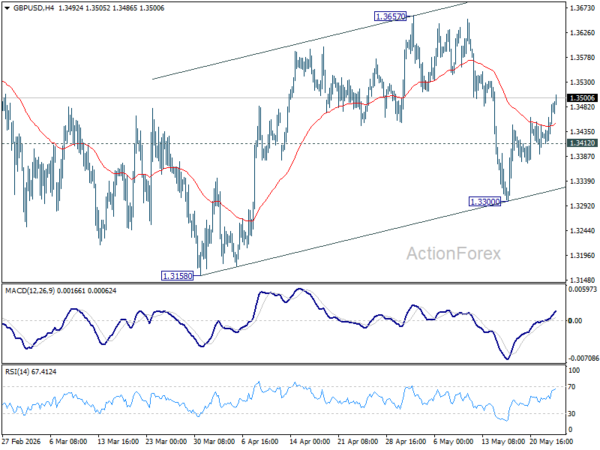

GBP/USD Daily Outlook

GBP/USD’s extended rebound suggests that pullback from 1.3657 has completed at 1.3300. Intraday bias is back on the upside for 1.3657 first. Firm break there will resume the rally from 1.3158. On the downside, below 1.3412 minor support will turn intraday bias neutral again.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.