The Euro weakened broadly after June inflation data came in softer than expected, reinforcing the view that the European Central Bank has won an important battle against the recent energy-driven inflation shock. Headline inflation slowed from 3.2% to 2.8%, while core inflation eased from 2.6% to 2.4%, both undershooting market expectations. The figures suggest the surge in oil prices during the second quarter failed to generate meaningful second-round inflation pressures, significantly reducing the urgency for further monetary tightening.

For markets, the implications extend well beyond the ECB’s July meeting. A pause next month was already widely anticipated, but the latest inflation data have also substantially lowered the probability of another rate hike in September. If inflation continues to moderate over the coming months, investors may soon begin shifting their focus toward the possibility of ECB rate cuts early next year. Such a repricing would remove one of the Euro’s key sources of support, particularly as the Federal Reserve continues to maintain a comparatively hawkish stance.

The Dollar, meanwhile, held firm despite June ADP employment growth slowing to 98k from 112k and falling short of expectations. Traders largely dismissed the report, reflecting the increasingly weak relationship between ADP employment and the official Non-Farm Payrolls data. Attention has instead shifted to Federal Reserve Chair Kevin Warsh’s appearance at the ECB Forum in Sintra. While Warsh is unlikely to offer explicit forward guidance, reaffirming his commitment to restoring price stability could reinforce the Dollar ahead of Thursday’s payrolls report, which remains the week’s defining event for Fed expectations.

Elsewhere, the Japanese Yen continued to underperform, falling to fresh four-decade lows against the Dollar as Tokyo refrained from escalating its verbal intervention campaign. The Canadian Dollar was the second weakest performer, followed by the Swiss Franc. At the other end of the spectrum, the New Zealand Dollar led gains, supported by resilient risk appetite, with Sterling and the Australian Dollar also outperforming. The Dollar and Euro sat near the middle of the weekly rankings, but for very different reasons—the Dollar gradually climbing as markets looked ahead to payrolls, while the Euro slipped as expectations for further ECB tightening faded.

Why Fed’s Warsh Could Trigger Silver’s Next Selloff Without Saying Much

NASDAQ Has Finished Consolidating. Now It Needs Permission from Goldilocks NFP

US ADP Employment: Hiring Slows While Wage Growth Holds Firm

Eurozone CPI Slows to 2.8%, Strengthening Case for ECB Pause

Eurozone PMI Manufacturing Shows Resilience, but Inventory Tailwind May Be Ending

UK Manufacturing PMI Slips from Four-Year High as Stockpiling Boost Fades

BoJ Tankan: Manufacturing Sentiment Climbs to Highest Since 2018, Outlook Turns More Cautious

Japan Manufacturing PMI Hits 12-Year Quarterly High as AI Demand Drives Growth

Australia Manufacturing PMI Finalized at Five-Month High Despite Middle East Disruptions

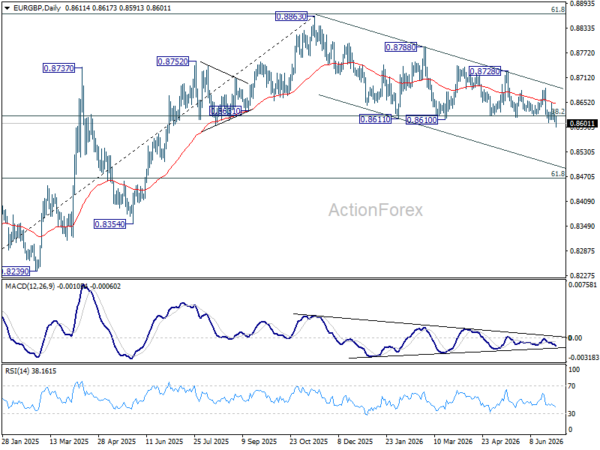

EUR/GBP Daily Outlook

Intraday bias in EUR/GBP is back on the downside with break of 0.8601 support. Sustained trading below 0.8618 fibonacci level should confirm bearish reversal. Next target is 0.8466. For now, risk will stay on the downside as long as 0.8686 resistance holds.

In the bigger picture, focus is staying on 38.2% retracement of 0.8221 to 0.8863 at 0.8618. Strong rebound from there will retain medium term bullishness. Rise from 0.8221 should resume through 0.8863 at a later stage. Nevertheless, sustained break of 0.8618 will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least.