The New Zealand dollar received the boost that normally accompanies a rate hike, but the rally quickly lost momentum. The Reserve Bank of New Zealand delivered a widely anticipated 25 basis point increase in the Official Cash Rate to 2.50%, yet investors stopped short of pricing a more aggressive tightening cycle. Instead, the market came away with the impression that while another hike is still likely, policymakers have set a considerably higher hurdle before taking the next step.

At first glance, the statement appeared hawkish. The Committee said “some further reduction in monetary stimulus is likely to be required” and that “further OCR increases appear likely at upcoming meetings.” But those remarks were balanced by equally strong caveats. The RBNZ repeatedly emphasized that medium-term inflation remains uncertain and that future decisions will depend on incoming data, firms’ price-setting behaviour and the strength of the recovery, adding that the timing of future hikes is “highly uncertain.”

That balance was reflected in the Record of Meeting. While all six members agreed to raise the OCR, they were not fully aligned on the inflation outlook. Prasanna Gai and Hayley Gourley believed risks remained tilted to the upside. However, Governor Anna Breman, Chief Economist Paul Conway, Assistant Governor (Money) Karen Silk and external member Carl Hansen judged the risks to be broadly balanced instead.

Those differences matter because the balanced camp included the Governor and two of the Bank’s most senior policy officials. Breman argued that weak demand could continue limiting businesses’ ability to pass higher costs on to consumers. Conway questioned how quickly the recovery would spread beyond stronger parts of the economy even while acknowledging firms might eventually rebuild margins. Silk pointed to two-way risks, noting that a weaker exchange rate could add to imported inflation, but slower immigration could simultaneously restrain growth, housing and inflationary pressure. Together, their comments suggest the Committee is looking for clearer evidence that inflation is becoming genuinely persistent before tightening again.

That explains the Kiwi’s muted reaction. The RBNZ reinforced its inflation-fighting credentials with another rate hike, but it deliberately avoided creating expectations of an automatic follow-up move. Investors appear to have concluded that policymakers are comfortable pausing at 2.50% until the data justify another increase, rather than feeling compelled to keep tightening simply because the cycle has begun.

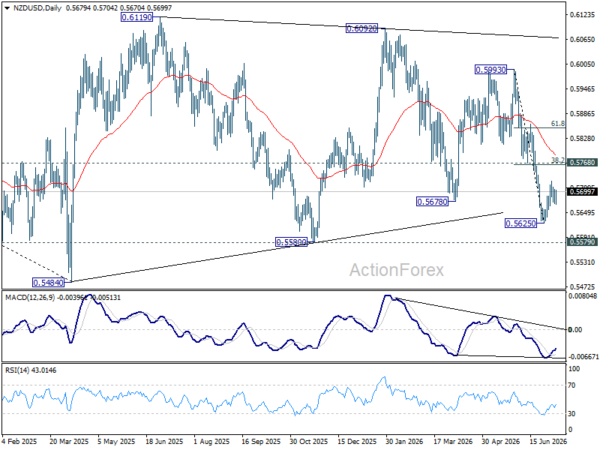

The charts tell a similar story. NZD/USD recovered after the decision but remained comfortably below last week’s high at 0.5726, suggesting buyers have yet to seize full control. The rebound from 0.5625 may still extend in the near term, but it continues to resemble a corrective recovery within a broader downtrend.

Even if another leg higher develops, upside should be capped by the 0.5768 resistance cluster, including the 38.2% retracement of 0.5993 to 0.5625 at 0.5766. Once the corrective rebound is complete, a break below 0.5625 remains the preferred scenario. A subsequent move through 0.5580 would shift focus back to the 2025 low at 0.5484.