Markets were driven by two competing sources of uncertainty today as Brent crude surged toward the $80 mark while investors awaited the release of the June FOMC minutes for the first real insight into Chair Kevin Warsh’s policy thinking. Dollar traded firmer alongside oil, while Kiwi outperformed following the Reserve Bank of New Zealand’s rate hike. Yen, meanwhile, gave back recent gains and was the weakest major currency as intervention concerns continued to fade.

Oil dominated market attention after Brent rebounded from around $72 just a day earlier to briefly trade above $79. The initial leg higher followed US strikes against Iranian targets in retaliation for attacks on commercial shipping transiting the Strait of Hormuz. That move appeared largely driven by short covering after Brent had fallen back to pre-war levels on expanding OPEC+ supply and improving shipping conditions through the Gulf.

The rally gathered fresh momentum after President Donald Trump declared at the NATO summit in Ankara that the Iran ceasefire was “over,” even as he added that negotiations could still continue. More importantly, the US Treasury withdrew the waiver allowing Iran to continue selling oil, marking the first concrete policy tightening of sanctions since the ceasefire framework was established. That directly challenges expectations that Iranian crude exports would gradually normalize, giving markets a more fundamental reason to rebuild part of the geopolitical risk premium.

Still, traders stopped well short of pricing a return to full-scale conflict. Trump’s remarks themselves contained an important contradiction. While describing the ceasefire as effectively finished, he simultaneously left the door open for further negotiations. Likewise, although Tehran condemned the US strikes as a “gross violation” of the June memorandum and vowed to defend its territorial integrity, neither side has formally declared the diplomatic framework abandoned. Markets have now witnessed several similar cycles of military confrontation followed by renewed negotiations since the April ceasefire, making investors reluctant to assume each flare-up represents a lasting escalation.

Whether today’s rebound develops into a broader repricing of geopolitical risk may depend on what follows next rather than what has already occurred. Additional sanctions, military deployments or direct disruptions to regional oil exports would point to a genuine breakdown of the ceasefire. In contrast, if recent events once again give way to diplomatic engagement, today’s rally may ultimately prove another positioning adjustment rather than the beginning of a sustained return of the war premium. From a technical perspective, a decisive break above the $80 psychological level would be the first stronger indication that markets are beginning to price a more durable deterioration in the geopolitical backdrop.

Away from geopolitics, attention now shifts to the June FOMC minutes. Their significance is greater than usual because they represent the first detailed account of policy discussions under Kevin Warsh’s leadership. Unlike previous Fed chairs, Warsh declined to submit an interest-rate projection in the Summary of Economic Projections and deliberately avoided providing meaningful forward guidance after the meeting. As a result, the minutes become the primary source for understanding how policymakers debated the outlook.

Markets will be looking beyond the unanimous decision to hold rates steady and instead focusing on the arguments made by the three emerging camps within the Committee. The June dot plot showed nine participants expecting at least one rate hike this year, eight projecting no further change and one anticipating a cut. Investors will pay particular attention to whether several officials argued that a rate increase was already warranted in June, as such language would reinforce the Fed’s hawkish shift despite last week’s softer-than-expected payroll report.

Iran Strikes Give Oil Bears a Reason to Cover—Not a Reason to Panic

NZD/USD Recovers After RBNZ, but Higher Bar for Next Hike Caps Rally

RBNZ Raises OCR, Consensus Masks Diverging Inflation Views

BoJ’s Asada: Demand-Driven Inflation Needed Before Another Rate Hike

RBA’s Hunter: Supply Shocks Don’t Mean Inflation Can Be Ignored

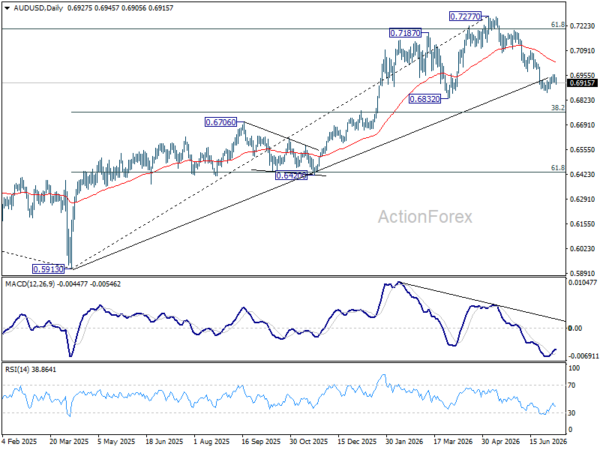

AUD/USD Daily Report

Intraday bias in AUD/USD remains neutral and consolidations could continue above 0.6864. Further fall is expected as long as 0.6977 support turned resistance holds. Below 0.6864 will target 0.6832 support. Firm break there will target 0.6756 fibonacci level. However, sustained break of 0.6977 will bring stronger rebound to 0.7087 resistance instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.