After days dominated by fears of an intensified tech rout and structural disruption from artificial intelligence, markets ended the week on a steadier footing. While volatility picked up meaningfully, Friday’s price action made clear that talk of an imminent trend reversal remains premature. Investors responded to midweek stress not by abandoning equities wholesale, but by rotating and selectively re-engaging. Sharp rebounds in some of the hardest-hit names underscored that confidence in long-term growth themes has weakened, but not collapsed.

This behavior reflects a maturing bull market rather than a broken one. As the cycle moves deeper into its later stages, investors are becoming more opportunistic and less complacent, choosing their entry points carefully instead of reflexively buying every dip. Such a shift almost inevitably brings more choppy conditions. Markets are now more sensitive to narratives, earnings expectations, and policy signals, which increases short-term volatility even as longer-term trends remain broadly intact.

Across asset classes, this has translated into consolidation rather than continuation. Big moves earlier in the week were followed by hesitation, suggesting participants are reassessing risk rather than repositioning aggressively. In that sense, the message from last week is clear that volatility is rising, leadership is narrowing, but the broader market structure still argues for caution against calling an outright top too early.

Currency markets reflected this selective risk adjustment. Aussie ended the week as the strongest performer, supported by the RBA’s hawkish turn, while the Dollar held firm amid bouts of risk aversion. Kiwi also outperformed on improved sentiment into the close. At the other end, Yen was the weakest major as election positioning and fading intervention risk weighed, with Sterling also under pressure after the BoE’s dovish hold. Euro and Swiss franc traded more neutrally.

US Stocks Hold Their Nerve Despite Tech Turbulence

After spending much of last week fixated on AI disruption risks and the threat of an intensified tech rout, Friday’s performance in US equities delivered an important counterpoint. Price action suggested that markets are not ready to abandon the broader uptrend, even as volatility rises and leadership narrows.

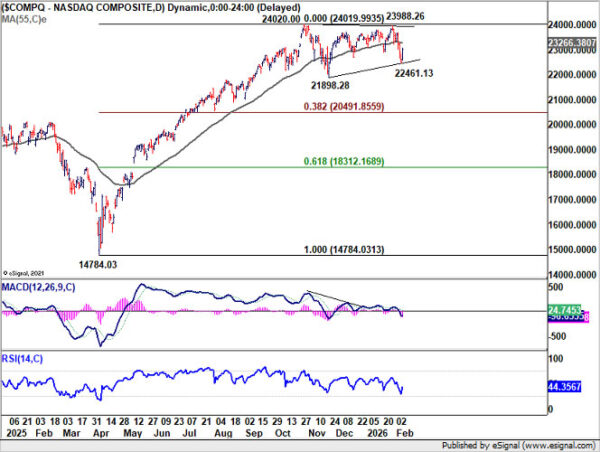

The standout move came from DOW, which surged nearly 2.5% on Friday to close above the 50,000 psychological level for the first time, and set a fresh record. The S&P 500 and NASDAQ both finished the week in the red. However, the sharp intraweek selloff now looks more like part of a near-term consolidation phase rather than the start of a broader trend reversal.

Crucially, Friday’s rebound within the tech sector itself challenges the bearish narrative. Some of the week’s hardest-hit names staged decisive recoveries, suggesting that positioning had become stretched rather than structurally broken. Nvidia jumped nearly 8% on Friday, while Broadcom rallied around 7%, both following steep declines earlier in the week. That behavior signals that investors have not meaningfully given up on the AI investment theme.

Instead, it appears markets are reassessing valuation, timing, and earnings delivery rather than rejecting the growth story outright. AI remains central to medium-term expectations, but the tolerance for disappointment has clearly diminished.

Some analysts have described the current environment as a bull market that is aging rather than dying. As this cycle moves into its fourth year, earnings expectations are rising and becoming more demanding, leaving less room for error. That shift naturally changes investor behavior Pullbacks are increasingly being viewed as opportunities, but not automatic ones. Investors are becoming more selective about where and when to add exposure.

Technically, DOW’s up trend is now eye next hurdle at 78.6% projection of 41,981.14 to 48,431.57 from 45,728.93 at 50,798.97 and close to medium-term rising channel ceiling. Decisive break above that zone would suggest the uptrend is entering a new phase of acceleration, opening the way toward the 100% projection at 52,179.36. Until then, the broader bullish outlook remains intact as long as 48,459.88 support holds on any pullback.

For NASDAQ, the corrective pattern from 24,020.00 remains in play. Rather than a straight decline through 21,898 support, Friday’s bounce suggests that it’s in for of a sideway pattern. The flat 55 D EMA (now at 23,266.38) is a focus in the coming days. Firm break there will affirm this case of sideway consolidations, and bring retest of 24,020.00 high. In this case, there is prospect of breaking through to new record if sentiment in other parts of the markets turn more positive.

Dollar Index to Face Test from 55 D EMA as Rebound Extends

Dollar Index extended the rebound from 95.55 last week, and breached 97.74 support turned resistance.

Relief surrounding the nomination of Kevin Warsh as the next Fed chair helped calm nerves. In the near term, the development reduced tail risks and lent Dollar some stability. Risk-off sentiment also played a role, particularly as US equities wobbled midweek on renewed tech-sector stress. That environment briefly favored Dollar.

However, as equity markets stabilized into Friday, the dollar’s upside momentum slowed. A more constructive risk backdrop could quickly turn the recent rebound into nothing more than a corrective pause in the larger down trend.

Technically, Dollar Index is approaching a critical decision zone. In the more bearish scenario, 55 D EMA (now at 98.28) should act as a key barrier to reject the current rise. That would set up downtrend resumption through 95.55 quickly. Next target will be 61.8% projection of 110.17 to 96.37 from 100.39 at 91.86.

Alternatively, in the less bearish case, sustained break above 55 D EMA would suggest that corrective pattern from 96.37 is developing into a five wave expanding triangle. In this case, stronger rebound could be seen towards 100.39 first, before seeing strong resistance from there to cap upside and bring larger down trend resumption through 95.55 later.

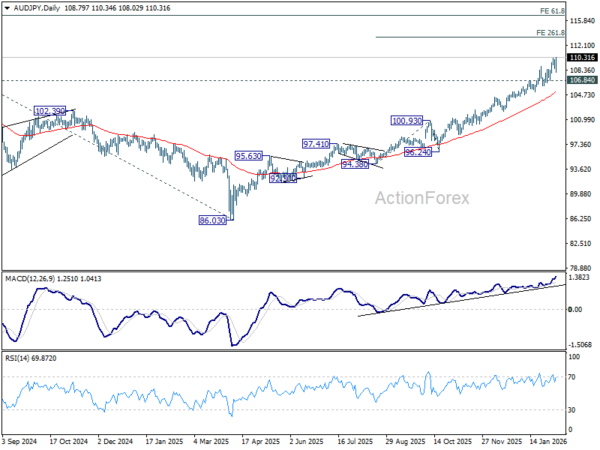

RBA Hawkish Turn Meets Yen Weakness as AUD/JPY Hits Record

In the currency markets last week, Aussie clearly stood out as the strongest performer, while Yen sank to the bottom of the table. That divergence made AUD/JPY the top mover of the week, with the cross gaining more 2.34% and pushing decisively into record territory.

Support for the Aussie came from the RBA, which delivered a decisively hawkish rate hike. The move to lift the cash rate to 3.85% confirmed that the RBA has shifted back into inflation-fighting mode after evidence of renewed price pressures late last year. Crucially, the RBA’s messaging suggested the tightening cycle may not be finished. Stronger consumption, a still-tight labour market, and capacity constraints have all raised the risk that inflation could remain above target for longer than previously assumed.

Some economists have already moved ahead of the curve. Analysts at Westpac, among others, now expect another rate hike in May, taking the cash rate to 4.10%. That repricing of the policy path has given the Aussie a durable yield advantage.

Risk-off sentiment during the middle of the week briefly capped the Australian Dollar’s upside. However, as broader market conditions stabilized into the close, the underlying rate support reasserted itself, leaving the Aussie well positioned for further gains if risk appetite improves ahead.

On the other side of the cross, Yen’s weakness has re-emerged as intervention risks faded. Talk of coordinated action between Japan and the US has cooled, removing a key deterrent that had previously limited speculative pressure on the currency.

Election positioning has compounded that pressure. Markets are increasingly confident for a strong outcome for Prime Minister Sanae Takaichi and, more importantly, the ruling Liberal Democratic Party in this weekend’s snap election, reinforcing expectations of fiscal expansion and looser financial conditions.

Takaichi’s standing received a further boost after US President Donald Trump offered what he described as his “total endorsement,” alongside confirmation of a White House meeting scheduled for March 19. That endorsement has strengthened perceptions of political stability and external support.

Polls suggest the LDP and its coalition partner Ishin could secure around 300 seats in the 465-seat lower house, a decisive improvement from their current razor-thin majority. Such an outcome would embolden fiscal stimulus plans and add further pressure to Japanese government bonds and Yen.

Against that backdrop, AUD/JPY surged to a fresh record high, closing the week at 110.31. Technically, D MACD point to renewed upside acceleration. Near term outlook will stay bullish as long as 106.84 support holds. Next target is 261.8% projection of 94.38 to 100.93 from 96.24 at 113.38.

Looking further out, the medium-term technical roadmap points to a more ambitious target at 61.8% projection of 59.85 (2020 low) to 109.36 (2024 high) from 86.03 (2025 low) at 116.62.

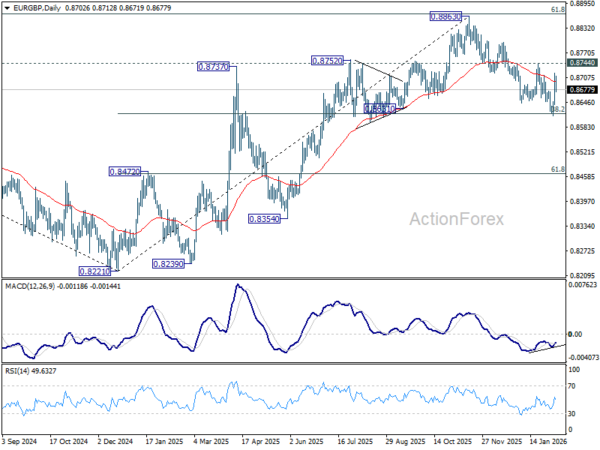

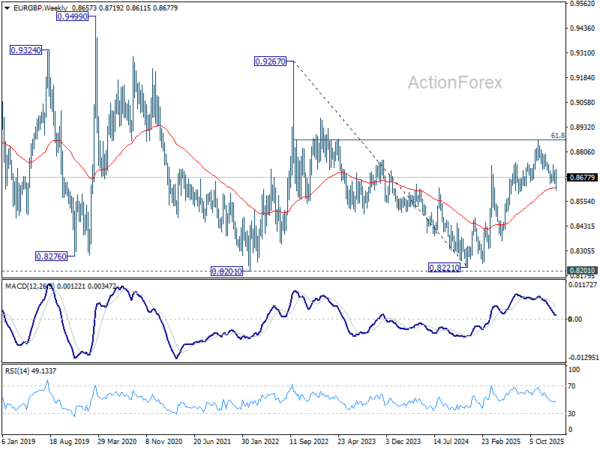

EUR/GBP Bounces After Dovish BoE, But Faces Both Heavy Support and Resistance

EUR/GBP ended last week on a firmer footing after bouncing sharply from a key technical support area. The move disrupted bearish momentum but stopped short of delivering a decisive bullish signal, leaving the cross trapped in a mixed picture.

On the Euro side, there was little in the latest ECB meeting to justify a sustained rally. The ECB left the deposit rate unchanged at 2.00% and reiterated that policy is appropriately calibrated, with no appetite for near-term adjustments. ECB officials remain comfortable with a prolonged pause. Despite softer near-term inflation readings, policymakers continue to view medium-term price dynamics as stable, allowing them to resist pressure for either easing or tightening.

Instead, the real catalyst for EUR/GBP came from the UK side. The BoE delivered a surprise dovish hold at 3.75%, with a narrow 5–4 vote that sharply raised the perceived probability of a March rate cut.

The BoE’s updated economic outlook reinforced that dovish shift. Under the new projections, CPI inflation is expected to fall to 1.7% by the first quarter of 2027, down from 2.2% previously. Annual GDP growth has been revised 0.3 percentage points lower to 1.2%.

Even so, the timing of the next cut remains highly data-dependent. With two labor market reports and two inflation prints due before the March meeting, the MPC still has scope to reassess if incoming data surprise meaningfully.

Technically, EUR/GBP is boxed in a tightly contested zone. On the upside, it’s facing resistance from 61.8% retracement of 0.9267 (2022 high) to 0.8221 (2024 low) at 0.8867, a level that previously capped advances. On the downside, support is provided by rising 55 W EMA (now at 0.8624) and 38.2% retracement of 0.8221 to 0.8663 at 0.8618. These opposing forces are compressing price action and setting the stage for a directional break.

These countervailing forces have turned the current zone into a battleground. Nevertheless, break of 0.8744 resistance in the coming days would reveal that the bulls are having more underlying control. That would suggest that fall from 0.8863 has probably completed as a corrective move. And then set up the stage for resuming the rise from 0.8221 through 0.8867 key fibonacci level mentioned.

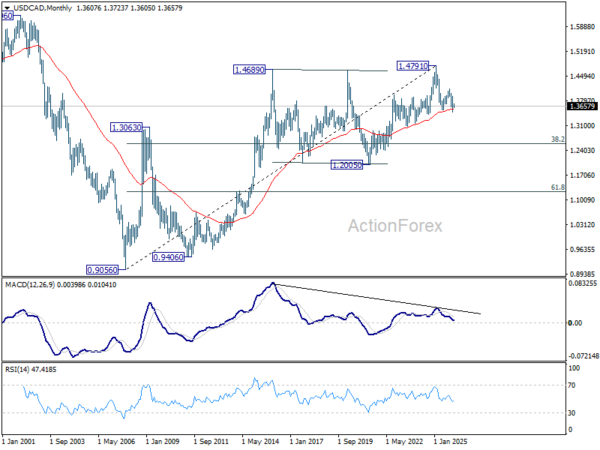

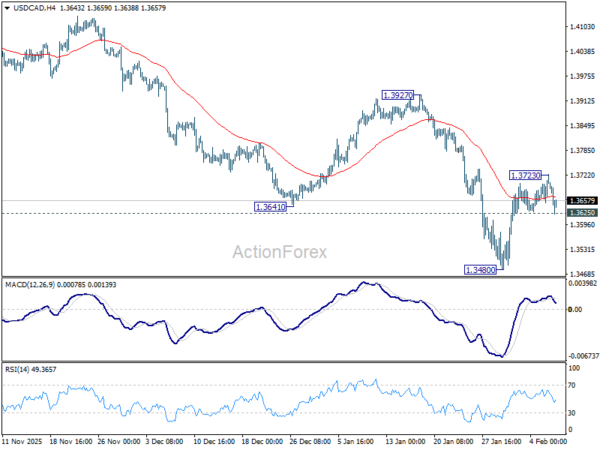

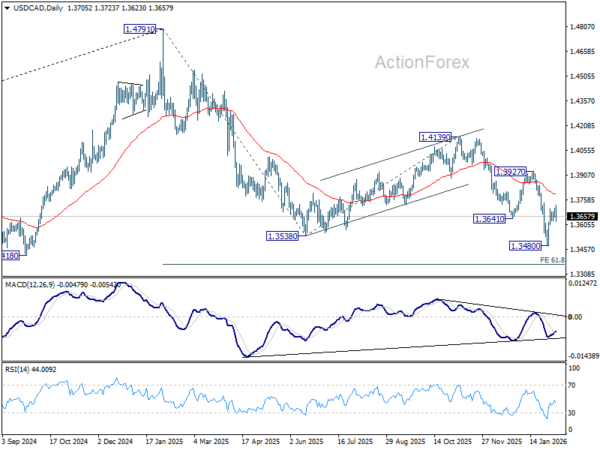

USD/CAD Weekly Outlook

USD/CAD’s rebound from 1.3480 short term bottom extended higher last week but lost momentum after hitting 1.3723. Initial bias is turned neutral this week first. In case of another rise, upside should be limited by 55 D EMA (now at 1.3791) to complete the corrective bounce. On the downside, break of 1.3625 will bring retest of 1.3480. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.