Japan dominated the Asian session as markets reacted to Prime Minister Sanae Takaichi’s decisive election victory over the weekend. The scale of the win, which delivered a supermajority in parliament, triggered a powerful relief rally in domestic equities and set the tone for the broader region. Nikkei surged to a fresh record above 57,000 before trimming some gains, but it continues to hold the bulk of the move. That momentum spilled across the region, lifting Asian equities broadly.

The move was also supported by improving global sentiment after US markets showed renewed resilience late last week. DOW surged to a new record above 50,000 last Friday, signaling that concerns over AI-driven disruption and capex excess have not derailed the broader bull market. With US equities regaining their footing, risk appetite in Asia found an additional tailwind.

Despite the equity surge, Yen’s initial selloff was restrained. Rather than extending sharply lower, the currency stabilized and even firmed modestly as the session progressed, reflecting traders’ sensitivity to renewed intervention risk.

Japanese officials were quick to step up verbal warnings. Finance Minister Satsuki Katayama reiterated over the weekend that authorities stand ready to engage markets to stabilize the Yen, stressing that Japan retains the right to intervene against moves that deviate from fundamentals. Katayama also confirmed close coordination with US Treasury Secretary Scott Bessent, reinforcing the credibility of Japan’s warnings.

That message was echoed today by top currency diplomat Atsushi Mimura, who said authorities were watching FX developments “with a high sense of urgency.” Chief Cabinet Secretary Minoru Kihara added to the chorus, voicing concern over one-sided currency moves. The coordinated messaging appears to have been effective in discouraging aggressive Yen selling, at least for now.

In currency markets, Yen emerged as the strongest performer of the day so far, followed by Aussie and Euro. On the other side, Dollar lagged the most, followed by Sterling and Kiwi, while Swiss Franc and Loonie traded more neutrally. Looking ahead, attention will shift quickly to a heavy US data slate, headlined by the delayed non-farm payrolls report and January CPI. Those releases will determine whether the current rebound in risk sentiment has legs.

In Asia, Nikkei rose 4.22%. Hong Kong HSI is up 1.71%. China Shanghai SSE is up 1.26%. Singapore Strait Times is up 0.50%. Japan 10-year JGB yield is up 0.055 at 2.289.

Nikkei celebrates Takaichi landslide, USD/JPY faces post-election reality check

Japan enters the week riding a powerful post-election wave after equities surged to fresh record highs. Nikkei jumped above 57,000 following Prime Minister Sanae Takaichi’s historic election victory. Although the index has since retreated modestly, it is still holding on to the bulk of its gains, up nearly 4.5% on strong domestic risk appetite.

Takaichi’s win was historic in scale. Her Liberal Democratic Party captured 315 seats in the lower house, its strongest showing ever, and together with coalition partner Ishin now controls 351 seats. That gives the ruling bloc a two-thirds supermajority, allowing it to override the upper house and advance legislation with unprecedented ease.

That supermajority significantly strengthens Takaichi’s hand. It opens the door not only to aggressive fiscal measures but also to constitutional changes, while easing the path for defense spending increases amid a more challenging global environment. For equity investors, political uncertainty has collapsed, and policy execution risk has been sharply reduced.

Yen, however, has not followed equities in a straight line. USD/JPY initially jumped at the Asian open but quickly retreated. Traders remain alert to the risk of intervention should the Yen weaken too sharply, limiting follow-through on election-driven selling. This leaves currency markets in wait-and-see mode. With the election result now fully realized, the question is whether Yen selling momentum can re-emerge as focus shifts back to fiscal expansion, or whether the pair has already priced in the bulk of the political shock.

Technically, momentum is already showing signs of fatigue. USD/JPY’s 4H MACD is falling below its signal line, indicating that the rebound from 152.07 is losing steam. That move is viewed as the second leg of a broader corrective pattern from 159.44. While further gains remain possible as long as 155.51 holds, strong resistance is expected near 159.44 high. A clear break below 155.51 would argue that the third leg of the correction is already underway, reopening the path back toward the 152.07 support ahead.

Japan’s nominal pay accelerates to 2.4% in December, but real wages still negative

Japan’s real wages fell -0.1% yoy in December, marking the 12th consecutive monthly decline, though the contraction was the smallest seen in 2025. While the pace of erosion is clearly slowing, the data underline how inflation continues to outpace pay gains for households.

Nominal wages rose 2.4% yoy, extending a 48-month streak of increases, but the outcome fell short of expectations for a 3.0% rise. The acceleration from November’s 1.7% growth points to improving momentum, but not yet at a pace sufficient to deliver sustained real income gains.

Breaking down the components, base salaries rose 2.2% yoy, picking up from November’s 1.7% yoy. Overtime pay increased 0.9%, slightly slower than the prior month’s 1.2%. Special payments, largely winter bonuses, rose 2.6% up from 1.5%.

Attention now shifts firmly to the upcoming spring wage negotiations. The key questions are whether large firms can again deliver pay hikes above 5% for the third straight years, and whether those gains finally spill over to smaller companies.

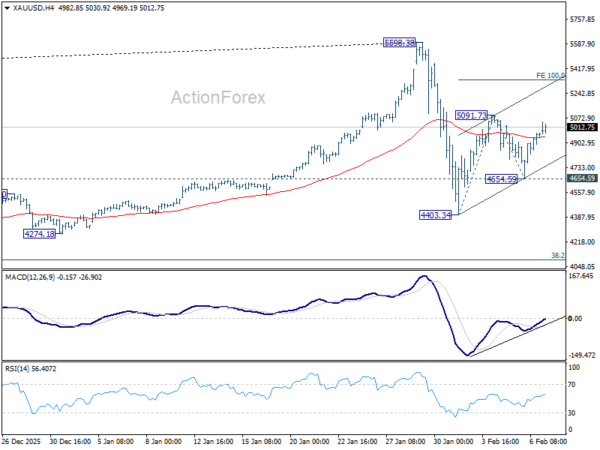

Gold eyes 5,300 after surviving shakeout, but longer-term reset will take more time

After two volatile weeks, Gold appears to have regained its footing. Prices have stabilized around the 4,400 area and have since pushed back above 5,000, signalling that the first wave of profit taking has likely run its course. The sharp pullback from the record high was forceful, but the subsequent price action suggests sellers have become less aggressive, opening room for a tradable rebound in the near term.

Technically, the decline from 5,598.38 to 4,403.34 is seen as the initial phase of a broader medium-term correction. That phase now appears complete. Price action since 4,403.34 marks the second phase of this corrective process, which can unfold in a more complex and time-consuming manner rather than a simple straight-line rebound.

For short-term traders, the outlook is constructive. The exhaustion of the initial profit-taking wave raises the prospect of further upside in the near term. As long as pullbacks remain contained, momentum favours additional gains before sellers re-emerge in force.

In this context, 4,654.49 serves as the key tactical line. Any near-term dip should be contained above this level. On the upside, decisive break of 5,091.73 would open the way toward 100% projection of 4,403.34 to 5,091.73 from 4,654.59 at 5,342.98. . That level is a natural target for the current rebound and represents the upper boundary of what short-term traders should reasonably expect from this phase.

However, strength into the 5,340–5,598 zone is likely to attract another round of profit taking, particularly from longer-term holders. That supply should cap near-term upside and prevent Gold from immediately resuming its larger bull trend.

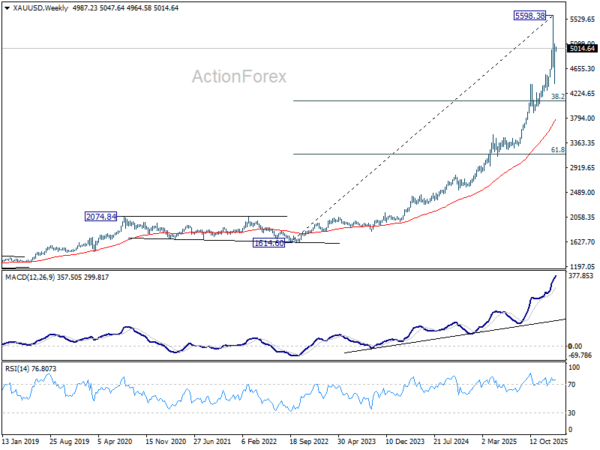

For long-term investors, patience is essential. The current rebound is not viewed as a trend resumption but as part of a broader consolidation correcting the entire advance from 1,614.50 (2022 low). While the long-term structure remains bullish, the market still needs time to absorb prior gains.

Any deeper pullback is expected to find stronger demand near the 4,000–4,400 accumulation zone, reinforced by 38.2% retracement of 1,614.60 to 5,598.38 at 4,076.57. Until fresh catalysts emerge, that area is the preferred zone for rebuilding long positions ahead of the next major uptrend, likely months rather than weeks away.

Delayed US jobs report to drive the next shift in Fed pricing

The week is set to be dominated by US economic data, with markets focused on the delayed January non-farm payroll report and January CPI. While both releases speak directly to the Fed’s mandate, it is the labor market that will ultimately shape near-term policy expectations.

The payroll report, postponed by several days due to the temporary government shutdown, arrives after a volatile stretch for risk assets. Last week’s tech-sector rout briefly lifted expectations for a March rate cut, but that shift has already begun to unwind. A hold at the March FOMC meeting remains the central scenario. The late-week recovery in equities, capped by a record close in DOW, has eased pressure on policymakers to act quickly.

Markets remain more confident about easing later in the year. The June meeting is firmly in focus, with roughly a three-in-four chance priced for a cut to the 3.25–3.50% range.

Inflation data this week will be watched closely but is unlikely to prove decisive unless it shows renewed and persistent acceleration. Fed officials have repeatedly stressed that tariff-related price pressures should be temporary, reducing the risk of overreaction to modest upside surprises.

The labor market, however, presents a different risk profile. Signs of a sharp slowdown in hiring would be harder to dismiss and could prompt renewed discussion around more insurance cuts. This imbalance sets up asymmetric market reactions, with downside surprises in jobs likely to move pricing more than upside inflation shocks.

In the UK, GDP figures will attract growing attention after the BoE’s surprising dovish hold last week. Markets have become increasingly confident that a March rate cut is possible, putting incoming data under greater scrutiny. The UK economy struggled for momentum at the end of 2025, and policymakers are now assessing whether fiscal measures from the Autumn Budget have meaningfully lifted activity. The durability of any such support into early 2026 remains an open question.

With the committee deeply split, marginal data surprises could easily tip the balance ahead of the March meeting. Growth data that disappoints would reinforce the case for easing, while resilience could embolden the more cautious camp.

Beyond the US and UK, secondary releases including Eurozone Sentix confidence, Swiss CPI, and China’s inflation data will provide additional color on global demand conditions, but they are likely to play a supporting role in a week dominated by US labor market risk.

Here are some highlights for the week:

- Monday: Japan average cash earnings; Swiss SECO consumer climate; Eurozone Sentix investor confidence.

- Tuesday: Australia Westpac consumer sentiment; Australia NAB business confidence; US retail sales, import prices, employment cost index.

- Wednesday: China CPI, PPI; US non-farm payrolls; BoC deliberations.

- Thursday: Japan PPI; UK GDP, production, trade balance; US jobless claims.

- Friday: New Zealand BNZ manufacturing; New Zealand inflation expectations; Swiss CPI; Eurozone GDP revision, trade balance; US CPI.

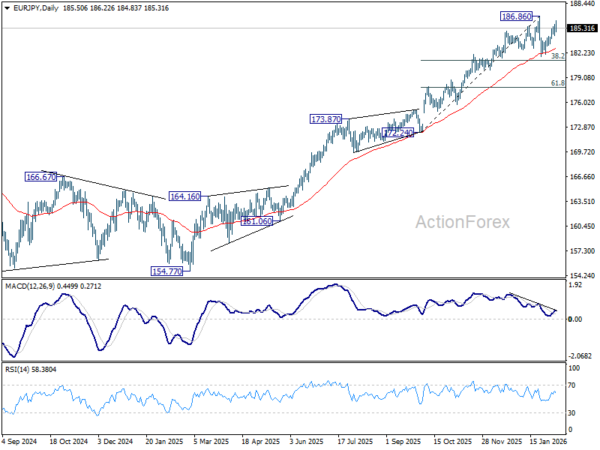

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.76; (P) 185.28; (R1) 186.21; More…

Intraday bias in EUR/JPY stays neutral for the moment. Price actions from 186.86 are developing in to a near term consolidation pattern. On the downside, below 184.26 support will bring another fall as the third leg. But downside should be contained by 38.2% retracement of 172.24 to 186.86 at 181.27 to bring rebound. On the upside, decisive break of 186.86 will resume larger up trend.

In the bigger picture, up trend from 114.42 (2020 low) is in progress. Upside momentum has been diminishing as seen in bearish divergence condition in D MACD. But there is not clear sign of topping yet. On resumption, next target is 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next. Meanwhile, outlook will stay bullish as long as 55 W EMA (now at 174.22) holds, even in case of deep pullback.