Risk sentiment was mixed in Asia today as Japan returned from holiday with Nikkei extending its post-election surge and briefly breaching the 58,000 mark for the first time on record. The breakout, however, lacked follow-through, with the index quickly trimming gains and hinting that near-term momentum may be stretched. Elsewhere in the region, trading was subdued. Broader Asian markets mirrored the near-flat close in the US overnight.

In currency markets, Yen remains the standout performer, extending its rally. The move partly reflects repeated official vigilance over currency volatility. Japan’s top currency diplomat, Atsushi Mimura, issued fresh warnings today. While declining to comment on speculation over rate checks following US employment data, he stressed that authorities are maintaining a “high sense of urgency” and have “not lowered our guard at all.” Mimura also confirmed that Tokyo remains in close contact with US authorities, reinforcing the perception that officials are prepared to act jointly if volatility becomes excessive.

Technically, the breach of near-term Fibonacci support in both EUR/JPY and GBP/JPY suggests that Yen’s reversal may be gaining traction. However, confirmation would require USD/JPY to break corresponding support levels to solidify the broader trend shift.

For Dollar, the boost from stronger-than-expected US payrolls proved short-lived. While the report effectively cemented expectations that the Fed will hold rates steady in March, it did little to firm up pricing for June. Attention now turns to January CPI data due tomorrow. A single inflation print may trigger volatility, but unless it materially shifts the inflation outlook, it is unlikely to establish a durable trend in Fed expectations.

In the US fiscal backdrop, January’s deficit narrowed compared to a year earlier as tariff collections surged. Customs duties reached USD30 billion for the month, lifting fiscal year-to-date revenue to USD124 billion — more than triple the level seen over the same period in 2025.

However, legal and political risks around tariffs remain elevated. The Supreme Court has yet to rule on challenges to the legal basis for the measures, keeping concerns that an adverse decision could force reimbursement of collected duties. Meanwhile, the House narrowly passed a resolution opposing tariffs on Canada, though any legislative reversal is unlikely given the high bar required to override a presidential veto.

On performance, Dollar remains the weakest currency of the week so far, followed by Sterling, which is awaiting UK GDP data. Euro is the third-worst performer. Yen leads gains, followed by Aussie and Loonie, while Swiss Franc and Kiwi trade mid-pack.

In Asia, at the time of writing, Nikkei is up 0.24%. Hong Kong HSI is down -0.89%. China Shanghai SSE is up 0.12%. Singapore Strait Times is up 0.63%. Japan 10-year JGB yield is down -0.02 at 2.217. Overnight, DOW fell -0.13% S&P fell -0.00%. NASDAQ fell -0.16%. 10-year yield rose 0.025 to 4.172.

Japan PPI eases to 2.3%, but import costs accelerate

Japan’s producer price index slowed slightly to 2.3% year-on-year in January from 2.4%, matching expectations and suggesting pipeline price pressures are stabilizing. The moderation came despite sharp divergences across components.

Fuel prices dropped -12.9% yoy, providing a significant drag on overall wholesale inflation. In contrast, nonferrous metal prices surged 33%, while agricultural goods rose 22.4%. Food and beverage prices also remained elevated, increasing 4.7% from a year earlier, highlighting persistent cost pressures in parts of the supply chain.

Meanwhile, Yen-based import prices climbed 0.5% yoy, up from a 0.2% gain in December. Despite a recent rebound in the currency, Yen’s broader weakness over recent months has raised the cost of imported energy and raw materials.

RBA’s Bullock says inflation above 3% “unacceptable,” keeps door open to more hikes

RBA Governor Michele Bullock reinforced the hawkish stance at a Senate estimates hearing today, making clear that further tightening remains on the table. “If we need to go up further because inflation is entrenched, the board will do so,” she said, stressing that returning inflation to target remains the central bank’s primary mandate.

Bullock said inflation running “with a three in front of it” is unacceptable. She noted that, at present, total demand is judged to be exceeding the economy’s capacity to supply, helping to explain ongoing inflation pressures. At the same time, she struck a more balanced tone on growth, pointing to the labour market as a key “positive”. While productivity remains weak and limits how fast the economy can expand, employment conditions are holding up. “We’re in this position because the economy is actually doing okay,” Bullock said,.

The RBA raised the cash rate by 25 bps last week to 3.85%, reversing one of last year’s cuts, after underlying inflation accelerated to 3.4% in the latest quarter. With forecasts pointing to inflation reaching 3.7% this year, markets now price roughly a 75% chance of another hike to 4.10% at the May meeting.

BoC minutes stress geopolitical risks, keep policy optionality

The BoC left its benchmark overnight rate at 2.25% in January, and the published summary of deliberations underlined how elevated uncertainty has reshaped policy discussions. Members agreed that maintaining “optionality” in setting monetary policy was critical given the unusually turbulent backdrop.

The minutes highlighted that recent geopolitical events — including tensions in Venezuela, Iran and Greenland — along with perceived threats to the independence of the Fede — have amplified global uncertainty. U.S. trade policy, increasingly seen as driven by geopolitical aims, was identified as a key source of unpredictability that could disrupt global supply chains and impact economic activity.

BoC officials also flagged downside risks associated with the upcoming review of the United States-Mexico-Canada Agreement (USMCA), suggesting that unresolved trade negotiations could weigh on Canadian growth.

Against this backdrop, the minutes reinforce the view that the BoC is likely to stay on hold for now, with flexibility to respond as data evolve.

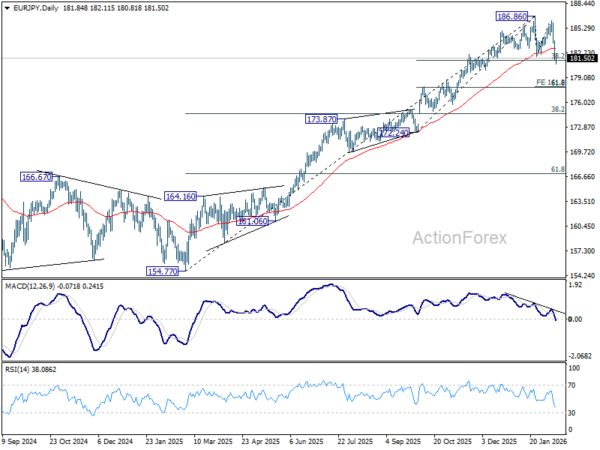

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.91; (P) 182.36; (R1) 183.39; More…

Immediate focus is now on 38.2% retracement of 172.24 to 186.86 at 181.27 as EUR/JPY’s fall accelerated lower. Decisive break there will argue that fall from 186.86 is correcting whole up trend from 154.77. Next near term target will be 161.8% projection of 186.86 to 181.76 from 186.22 at 177.96. Nevertheless, strong rebound from current level, followed by break of 182.99 minor resistance will retain near term bullishness, and bring retest of 186.86 high first.

In the bigger picture, up trend from 114.42 (2020 low) is in progress. Upside momentum has been diminishing as seen in bearish divergence condition in D MACD. But there is no clear sign of topping yet. On resumption, next target is 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next. Meanwhile, outlook will stay bullish as long as 55 W EMA (now at 174.22) holds, even in case of deep pullback.