Forex markets are relatively subdued today, with most major pairs and crosses confined within yesterday’s ranges. After recent volatility, positioning appears balanced as traders await a stronger catalyst to drive the next move.

Sterling is modestly firmer despite weaker-than-expected UK GDP data. December growth came in soft and the fourth quarter barely managed a positive reading, yet the currency’s resilience suggests markets are focusing on stabilization rather than disappointment.

Some economists argue that the latest figures point to an economy that has bottomed out rather than one sliding into contraction. Surveys indicate a pickup in manufacturing activity in January and early signs of revival in services, supporting hopes that growth momentum could improve as 2026 unfolds.

The National Institute of Economic and Social Research expects UK GDP to expand by 0.3% in the Q1. Associate economist Fergus Jimenez-England noted that while 2025 growth of 1.3% slightly undershot expectations and Q4 services were weak, business sentiment has improved after months of uncertainty surrounding the Autumn Budget.

Policy expectations are also lending support. BoE Monetary Policy Committee member Sarah Breeden said it is “reasonable to expect” another quarter-point rate cut by the end of April. Her comments that it is time to “take the foot off the monetary brake” reinforced expectations that easing could resume soon.

Elsewhere, Yen’s rally appears to be losing some immediate momentum. Technical resistance levels in key crosses may be limiting further gains for now, although the pullback remains shallow. The sustainability of Yen’s move will likely depend on broader market sentiment, particularly developments in Japan’s domestic equity market. The Nikkei continued its record run today, but signs of exhaustion are emerging after an extended rally.

Political optimism has been a key driver. Investors have embraced Prime Minister Sanae Takaichi’s strong electoral mandate and the prospect of higher spending, tax relief and a more assertive economic agenda. However, questions remain over how new fiscal initiatives will be funded. A shift in domestic risk appetite could help underpin a more durable Yen reversal.

For the week so far, Dollar remains the weakest performer, followed by Sterling and Euro. Yen leads gains, with Aussie and Kiwi also firm. Swiss Franc and Loonie are trading in the middle of the pack as markets wait for the next catalyst.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 1.38%. CAC is up 1.00%. UK 10-year yield is down -0.018 at 4.463. Germany 10-year yield is flat at 2.797. Earlier in Asia, Nikkei fell -0.02%. Hong Kong HSI fell -0.86%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield fell -0.002 to 2.235.

US initial jobless claims fall to 227k, above exp 222k

US initial jobless claims fell -5k to 227k in the week ending February 7, above expectation of 222k. Four-week moving average of initial claims rose 7k to 219.5k.

Continuing claims rose 21k to 1,862, in the week ending January 31. Four-week moving average of continuing claims fell -3k to 1,847k, lowest since October 5, 2024.

UK GDP misses at 0.1% mom growth, production and construction drag

UK GDP rose just 0.1% mom in December, undershooting expectations for a 0.2% gain and pointing to a subdued end to 2025. While services output expanded by 0.3% on the month, weakness in production, which fell -0.9%, and construction, down -0.5%, capped overall growth.

For the fourth quarter as a whole, GDP grew 0.1% quarter-on-quarter compared with Q3. Production output provided the largest positive contribution, rising 1.2%, while services showed no growth and construction contracted sharply by -2.1%.

On a broader basis, GDP expanded 1.0% in the three months to December 2025 compared with a year earlier, with services and production both up 1.0%. Annual GDP growth for 2025 came in at 1.3%, driven primarily by 1.4% growth in services, while production posted its first annual increase since 2021 at 0.2%. Construction grew 1.8%.

Japan PPI eases to 2.3%, but import costs accelerate

Japan’s producer price index slowed slightly to 2.3% year-on-year in January from 2.4%, matching expectations and suggesting pipeline price pressures are stabilizing. The moderation came despite sharp divergences across components.

Fuel prices dropped -12.9% yoy, providing a significant drag on overall wholesale inflation. In contrast, nonferrous metal prices surged 33%, while agricultural goods rose 22.4%. Food and beverage prices also remained elevated, increasing 4.7% from a year earlier, highlighting persistent cost pressures in parts of the supply chain.

Meanwhile, Yen-based import prices climbed 0.5% yoy, up from a 0.2% gain in December. Despite a recent rebound in the currency, Yen’s broader weakness over recent months has raised the cost of imported energy and raw materials.

RBA’s Bullock says inflation above 3% “unacceptable,” keeps door open to more hikes

RBA Governor Michele Bullock reinforced the hawkish stance at a Senate estimates hearing today, making clear that further tightening remains on the table. “If we need to go up further because inflation is entrenched, the board will do so,” she said, stressing that returning inflation to target remains the central bank’s primary mandate.

Bullock said inflation running “with a three in front of it” is unacceptable. She noted that, at present, total demand is judged to be exceeding the economy’s capacity to supply, helping to explain ongoing inflation pressures. At the same time, she struck a more balanced tone on growth, pointing to the labour market as a key “positive”. While productivity remains weak and limits how fast the economy can expand, employment conditions are holding up. “We’re in this position because the economy is actually doing okay,” Bullock said,.

The RBA raised the cash rate by 25 bps last week to 3.85%, reversing one of last year’s cuts, after underlying inflation accelerated to 3.4% in the latest quarter. With forecasts pointing to inflation reaching 3.7% this year, markets now price roughly a 75% chance of another hike to 4.10% at the May meeting.

RBA’s Hunter: Job market tightness consistent with inflation pressure

RBA Assistant Governor Sarah Hunter signalled that Australia’s labour market remains tight despite signs of moderation elsewhere in the economy. In a speech today, she said the RBA’s full employment and NAIRU frameworks indicate that conditions have stabilized and remain “a bit tight,” consistent with “some inflationary pressure in the economy.”

She described the relationship between labour tightness and inflation as “like the entwined double helix,” arguing that persistent capacity constraints continue to underpin price pressures. Recent data support that view, with unemployment unexpectedly falling to a seven-month low of 4.1% in December, raising the possibility that the labor market may be tightening again.

Hunter noted that the slowdown over the past few years has occurred primarily through fewer vacancies, reduced job switching, and slower hiring rather than a material rise in unemployment.

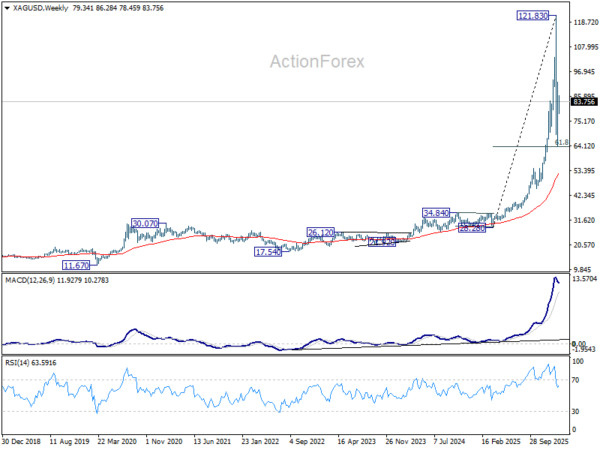

Silver push toward 100 hinges on 85/86 key barrier break

Silver is now pressing into a critical near-term resistance cluster around 85–86, a zone that could determine whether the sharp selloff from 121.82 has already bottomed at 63.98 or whether another leg lower is still ahead. The area combines 55 4H EMA (now at 85.27) and 38.2% retracement of 121.83 to 63.98 at 86.07, creating a technically dense barrier. Price reaction here is likely to set the tone for the next multi-week move.

Stepping back briefly, strong support emerged at 63.98, around 61.8% retracement of 28.28 to 121.83 at 64.04. That the decline from 121.82 is a correction to the up trend from 28.28 only. While the larger picture still points to prolonged medium-term consolidation, the immediate question is whether the next short-term upswing is about to unfold.

If Silver can sustain trading above the 85/86 zone, it would solidify the case that the first corrective leg completed at 63.98 and that a second leg higher is underway. In that scenario, further rise should be seen to 61.8% retracement of 121.83 to 63.98 at 99.73. However, the psychological 100 level sits just above that target and is likely to cap upside.

Conversely, rejection at 85/86 followed by a break below 78.68 support would shift the bias back to the downside. That would put 63.98 back in view and raise the probability that the correction is deeper than initially thought. In that case, the pullback could extend into a broader correction of the uptrend from 17.54 (2022 low), or even the larger advance from 11.69 (2020 low), before a durable base forms.

For now, the technical picture argues for patience rather than conviction. Silver is sitting at a clear decision point, and clarity should emerge within days. A confirmed break above 86 would favor positioning for a push toward 100, while failure at resistance would suggest waiting for another dip before considering fresh long positions.

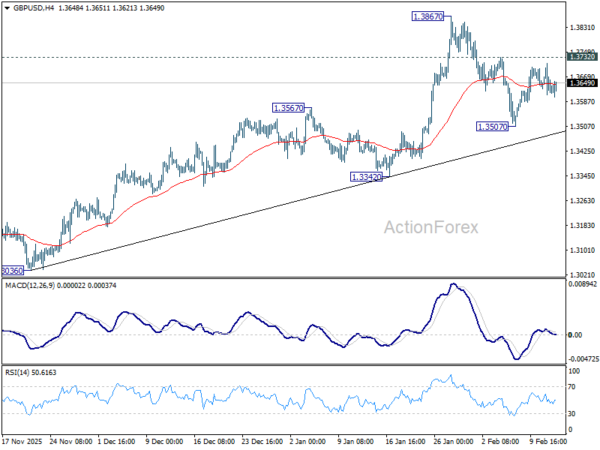

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3650; (R1) 1.3691; More…

GBP/USD is still gyrating in tight range below 1.3732 resistance and intraday bias remains neutral. On the upside, firm break of 1.3732 will suggest that pullback from 1.3867 has completed as a correction at 1.3507. Retest of 1.3867 should be seen first. Firm break there will resume larger up trend towards 1.4284 key resistance. On the downside, however, sustained trading below 55 D EMA (now at 1.3505) will raise the chance of larger scale correction, and target 1.3342 support for confirmation.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.