Aussie is mildly firmer in quiet trading, though momentum remains restrained. Broader market conditions are subdued, with most major pairs still trapped inside Friday’s ranges, reflecting wait-and-see stance. RBA February meeting minutes are due tomorrow, followed by January employment data on Thursday. These releases will help shape expectations for whether the central bank is preparing another rate hike.

After raising rates earlier this month, the key question is whether tightening cycle extends further. Markets broadly expect a 25bps hike in May, contingent on Q1 CPI confirming persistent inflation pressure. For now, that remains base case.

However, counterarguments are building too. Aussie has appreciated nearly 5% since start of year, which should help dampen import inflation. Stronger currency, combined with already tight monetary settings and restrained fiscal impulse, may cool growth momentum in coming quarters. That dynamic raises possibility that RBA could be done with policy fine-tuning. If inflation moderates faster than expected, policymakers may opt for extended pause rather than another hike.

The tone of upcoming minutes is likely to emphasize vigilance on inflation risks. Such messaging would reinforce tightening bias and lend near-term support to Aussie. Still, RBA has shown flexibility in rhetoric in recent months, adjusting tone quickly as incoming data shifts.

Ultimately, sustainable direction will hinge more on labor market strength. A firm jobs print would reinforce expectations for May tightening, while softer figures could challenge rate hike pricing.

For now, Aussie leads modest gains, followed by Dollar and Kiwi. Yen underperforms alongside Swiss Franc and Sterling, while Euro and Loonie sit mid-pack. Yet with nearly all major pairs confined to narrow ranges, meaningful direction likely awaits catalysts later this week.

In Europe. at the time of writing, FTSE is up 0.36%. DAX is up 0.01%. CAC is up 0.48%. UK 10-year yield is down -0.022 at 4.398. Germany 10-year yield is down -0.01 at 2.75. Earlier in Asia, Nikkei fell -0.24%. Hong Kong HSI rose 0.52%. China was on holiday. Singapore Strait Times rose 0.02%. Japan 10-year JGB yield rose 0.002 to 2.215.

Eurozone industrial output contracts -1.4% mom in December, capital goods drag

Eurozone industrial production fell -1.4% mom in December, slightly better than expectation of -1.5% mom, but still signaling weak momentum into year-end. .

By category, capital goods output in Eurozone dropped sharply by -1.9%, highlighting fragile business investment conditions. Production of intermediate goods edged down -0.1%, energy slipped -0.3%, and non-durable consumer goods fell -0.3%. Durable consumer goods provided limited offset, rising 0.2%.

Across the broader EU, production declined -0.8% mom. Slovakia (-4.9%), Germany (-2.9%), and Spain (-2.6%) recorded the steepest contractions, while Luxembourg (+6.4%), Sweden (+4.4%), and Malta (+4.2%) posted solid gains.

BoJ’s Ueda holds first post-election talks with Takaichi

BoJ Governor Kazuo Ueda met Prime Minister Sanae Takaichi for the first time since the LDP’s decisive election win, in talks closely watched by markets for clues on policy direction. The timing is notable, with expectations growing that inflation pressures tied to Yen weakness could accelerate interest rate normalization.

Following the meeting, Ueda described the talks as a “general exchange of views on economic and financial developments,” adding that the prime minister made no specific monetary policy requests. Pressed on whether he secured political backing for the BoJ’s rate hikes, Ueda declined to provide details, saying there was nothing he could disclose about the substance of the discussion.

Speculation has intensified in recent weeks that rising cost-of-living pressures may prompt the BoJ to consider raising rates as early as March or April. While the meeting yielded no explicit signals, the absence of public disagreement may be interpreted as tacit support for the central bank’s cautious path toward policy tightening.

Japan sidesteps technical recession as Q4 growth barely grows by 0.1% qoq

Japan’s economy narrowly avoided a technical recession in Q4, but the rebound fell short of expectations. GDP rose just 0.1% qoq, below the 0.4% forecast, though an improvement from Q3’s -0.6% contraction. On an annualized basis, growth came in at 0.2%, recovering from -2.6% but well under the expected 1.6%.

Private consumption, which accounts for more than half of output, edged up 0.1%. Demand for mobile phones provided support, though spending on food and autos declined. External demand was weak, with exports falling -0.3% qoq, dragged down by soft automobile shipments.

Investment provided modest offsets. Business spending rose 0.2%, supported by strong demand for semiconductor-manufacturing equipment, while housing investment jumped 4.8%.

NZ BNZ services falls to 50.9, employment weakness offsets sales strength

New Zealand’s BusinessNZ Performance of Services Index eased from 51.7 to 50.9 in January, slipping further below the survey’s historical average of 52.8. While the index remains marginally in expansion territory, the details reveal a mixed picture. Activity and sales improved from 52.5 to 54.2, but employment deteriorated from 49.6 to 49.1, staying firmly in contraction. New orders edged lower from 52.1 to 51.8, suggesting demand momentum is softening at the margin.

Sentiment remains subdued. The proportion of negative comments rose sharply to 58.7%, up from 50.4% in December and 52.9% in November. Respondents cited seasonal disruptions from Christmas–New Year holidays, fewer enquiries, and a prolonged post-holiday lull. Elevated living and operating costs continue to weigh on business confidence, underscoring fragile recovery conditions.

Still, BNZ Senior Economist Doug Steel struck a more constructive tone, noting that data since late 2025 has reinforced confidence that positive momentum can be sustained. While services growth is hardly robust, the economy appears to be expanding gradually.

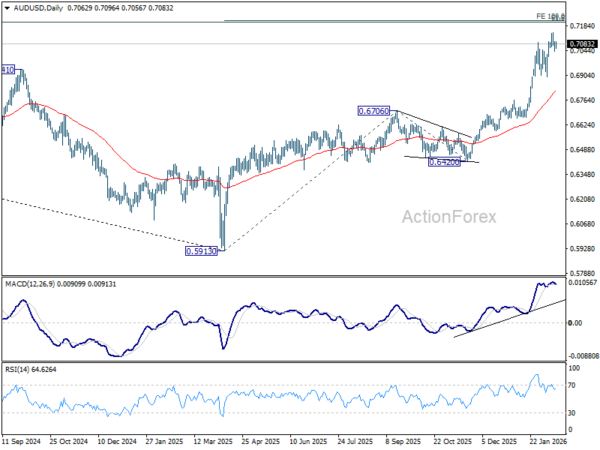

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.7046; (P) 0.7072; (R1) 0.7100; More…

AUD/USD recovers mildly after hitting 55 4H EMA, but stays below 0.7146 short term top. Intraday bias stays neutral at this point, and more consolidations would be seen. Deeper retreat cannot be ruled out, but downside should be contained above 0.6896 support to bring another rally. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.