- January data reinforce expectations of a 25 basis point rate cut in March

- Industrial production declined, with construction down 12.8 percent year on year

- Weakness was broad based, affecting most monitored sectors

- Producer prices fell by 2.6 percent year on year, deepening deflation

- Wage growth showed early signs of moderation

- Disinflationary trends support a more dovish monetary policy outlook

- EUR/PLN is approaching recent multi month highs near 4.2240, with a potential head and shoulders pattern suggesting further upside risk for the pair and continued pressure on the zloty in the medium term.

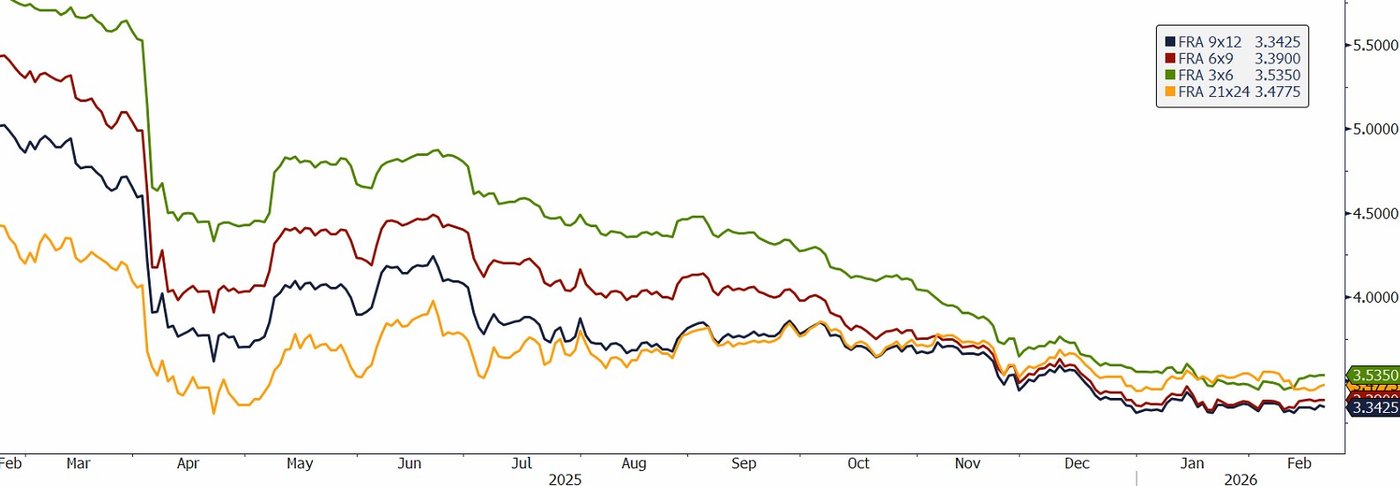

- PLN FRA rates indicate that markets expect a sustained easing cycle, with forward pricing pointing to policy rates falling toward 3.5 percent within six months and signaling confidence in further monetary accommodation.

Industrial slowdown becomes more visible

The latest macroeconomic releases from Poland have further strengthened the case for a 25 basis point interest rate cut at the March meeting of the Monetary Policy Council. Recent remarks from National Bank of Poland Governor Adam Glapiński and several MPC members, including Gabriela Masłowska, Przemysław Litwiniuk, Ludwik Kotecki and Henryk Wnorowski, had already suggested growing confidence that inflation pressures are receding. The January data now provide tangible evidence supporting that view.

Industrial output fell short of expectations and posted a notable decline. The construction sector stood out negatively, contracting by 12.8 percent year on year. Although unusually low temperatures were cited as a partial explanation, weakness was widespread, with 21 out of 34 monitored sectors reporting declines. More broadly, the region has been experiencing a downward trend in the level of industrial production, not merely a moderation in growth rates, following the temporary post pandemic rebound. The latest figures do little to challenge that pattern.

Producer price deflation intensifies

Producer prices fell by 2.6 percent year on year in January, undershooting market expectations and marking the deepest decline since December 2024. This points to subdued cost pressures in the manufacturing sector and lowers the likelihood of renewed price pass through to consumers in the months ahead. The data reinforce the narrative that disinflationary forces remain firmly in place.

Labour market momentum gradually moderates

Early signs of cooling are also emerging in the labour market. Monthly wage dynamics slowed slightly, indicating that upward pressure on pay growth may be easing. Together with weak industrial activity and falling producer prices, this strengthens the broader picture of a softening inflation environment.

Implications for monetary policy and the zloty

Against this backdrop, a March rate cut appears increasingly plausible. Should the central bank move forward with easing, the Polish zloty could remain relatively softer compared with regional currencies. However, relative performance will also depend on policy developments elsewhere.

Is a head and shoulders pattern forming on EUR/PLN?

The zloty is steadily losing value. EUR/PLN is currently trading around 4.2240, bringing the exchange rate close to the highs recorded in December 2025 as well as January and February 2026. Recently, the upper boundary of the accelerated downward channel has been breached. On the chart, a potential head and shoulders pattern can be identified, which at least in theory signals further upside in the medium term.

PLN FRA curve signals further monetary easing ahead

The chart presents PLN FRA (Forward Rate Agreement) rates, which reflect market expectations for future short term interest rates. The current pricing indicates that investors anticipate further monetary easing in Poland, with forward rates suggesting that policy rates could decline toward the 3.5 percent area within the next six months.

Across different FRA tenors, the downward shift in rates points to a broadly shared view that the National Bank of Poland is likely to continue loosening monetary policy. The convergence of shorter and medium term contracts at lower levels suggests that the market expects a series of rate cuts rather than a one off adjustment.

Overall, the FRA curve implies that participants see a sustained easing cycle ahead, driven by moderating inflation pressures and softer macroeconomic conditions. This forward pricing reflects growing confidence that the policy stance will become more accommodative over the coming quarters.

Opinions are the authors’; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. The provided publication is for informational and educational purposes only.

If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please refer to the MarketPulse Terms of Use.

Visit https://www.marketpulse.com/ to find out more about the beat of the global markets.

© 2026 OANDA Business Information & Services Inc.