Global markets were forced to face three major developments last week, each capable on its own of destabilizing sentiment. Instead of buckling under the weight of legal, monetary, and geopolitical shocks, investors responded with surprising composure.

At the end of the week came a landmark legal decision in the US that struck at the core of the administration’s trade strategy. What initially appeared to be a dramatic policy reversal quickly morphed into something more nuanced. The headline shock faded almost as quickly as it arrived.

Before that, the Fed delivered minutes that were more hawkish than anticipated. Hopes for a smooth glide path toward rate cuts were tempered, and the policy debate subtly widened. Yet even that failed to meaningfully dent risk appetite.

Meanwhile, tensions between the U.S. and Iran escalated to levels not seen in years. The rhetoric sharpened, timelines narrowed, and analysts began openly discussing conflict probabilities. Oil and precious metals responded swiftly.

But broader markets? They hesitated rather than panicked. Equity indexes held firm, Treasury yields stabilized, and high-beta currencies remained resilient. If there was fear, it was selective.

The clearest signal came from foreign exchange. Rather than fleeing risk, investors rotated into it. The week’s top performer was not a defensive cross but one typically associated with global growth. That alone speaks volumes about the market’s underlying confidence.

A Legal Setback, Not a Policy Reversal: Tariffs Reconfigured

The long-awaited U.S. Supreme Court ruling on President Donald Trump’s sweeping tariff policy finally arrived late on Friday, delivering what appeared at first glance to be a decisive blow. In a 6–3 decision, the Court ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the president authority to impose broad, country-wide tariffs without congressional approval. The so-called “Liberation Day” tariffs, which had ranged from 10% to 50% on nearly all trading partners, were effectively invalidated.

From a constitutional standpoint, the decision was significant. It reaffirmed limits on executive authority and potentially opened the door for importers to seek refunds on an estimated USD 160–200 billion in duties collected since 2025. In legal terms, it was a landmark moment.

In market terms, however, it barely registered.

Within hours of the ruling, the administration pivoted. A temporary 10% global tariff was imposed under Section 122 of the Trade Act of 1974, a statute designed to address balance-of-payments concerns. While capped at 150 days without congressional approval, it effectively replaced much of the invalidated structure in the short run.

Simultaneously, new Section 301 and Section 232 investigations were launched, laying the groundwork for more durable, sector-specific measures. Steel, aluminum, automotive, and lumber tariffs remain intact under national security provisions. The trade war did not end—it simply changed its legal scaffolding.

The practical implication is that the average U.S. tariff rate may fluctuate, potentially moving from roughly 15% back toward 8–10%. But the broader message is unchanged: tariffs are not disappearing. They are becoming more targeted, more complex, and more embedded.

Investors appear to have concluded that trade friction is now a structural feature of the global economy. Whether imposed under emergency powers or through traditional trade statutes, the direction of policy remains restrictive.

In that sense, the Supreme Court ruling was less a turning point than a transition—from sweeping, across-the-board tariffs to a more intricate, sector-by-sector trade confrontation. Markets, having already priced in persistent trade tension, treated it largely as a wash.

Hawkish Pause: The Fed Reopens the Door to Two-Sided Risk

If markets were expecting reassurance from the Federal Reserve last week, they did not get it. The minutes from the January 27–28 FOMC meeting revealed a tone that was distinctly more hawkish than anticipated, challenging the narrative of an orderly glide path toward rate cuts.

Investors had largely framed the current stance as a “dovish pause” — a temporary hold before easing resumes. Instead, the minutes suggested something closer to a “hawkish pause.” Policymakers emphasized that inflation risks remain alive, and several participants argued that the Committee should adopt explicitly “two-sided” language in its guidance.

That shift matters. Two-sided language implies that rate hikes are not entirely off the table. While no immediate tightening is imminent, the mere reintroduction of that possibility underscores how conditional the easing cycle has become.

Crucially, the “vast majority” of officials judged that downside risks to employment have moderated. With the labor market seen as stabilizing rather than deteriorating, the Fed appears to feel it has room to wait. Patience, not urgency, now defines the policy stance.

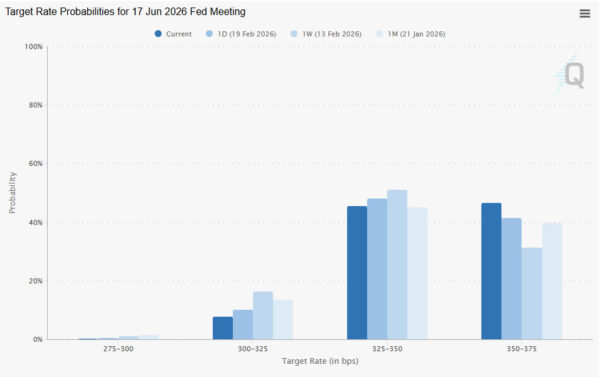

Market pricing adjusted, but only modestly. Odds of a March cut fell further, while expectations for June softened at the margin from 69% to 54%. Yet there was no wholesale repricing of the rate path.

War Premium Returns: Markets Weigh a Narrowing Diplomatic Window

Geopolitical risk re-entered the spotlight last week as tensions between the US and Iran escalated sharply. Rhetoric hardened, diplomatic timelines narrowed, and the market began to price in a non-trivial probability of conflict.

President Trump’s explicit “10-day” decision window transformed a slow-moving standoff into a defined countdown. That framing alone was enough to reintroduce a measurable war premium into oil and precious metals, even if broader markets remained composed.

The core difficulty lies in the widening gap between the two sides’ red lines. Washington is reportedly pushing for a sweeping framework that would effectively dismantle Iran’s nuclear and missile capabilities. Tehran, by contrast, views those programs as existential safeguards against regime change.

The situation is increasingly a collision course. Regional experts and intelligence briefings suggest that the perceived probability of military confrontation has risen to levels not seen in decades, with some framing the odds as close to even.

Yet markets are drawing a distinction between elevated risk and imminent action. While crude prices surged and gold caught a bid, equity indices and high-beta currencies showed limited signs of stress.

For now, investors appear to be adopting a wait-and-see posture. The war premium has returned — but it remains contained to assets most directly exposed to energy supply disruption and geopolitical tail risk.

Equities Hold the Line, Yields Stabilize

Despite the convergence of trade uncertainty, hawkish Fed signals, and rising geopolitical tension, US equity markets showed remarkable stability. On the surface, at least, risk appetite appears intact, with major indexes consolidating just below record highs rather than retreating.

Technically, DOW continued to trade in tight range beneath 50,499.04 peak. The broader technical outlook remains bullish, with scope for another leg higher toward 78.6% projection of 41,981.14 to 48,431.57 from 45,728.93 at 50,798.97. Firm break there would confirm renewed upside momentum and open the door toward 100% projection at 52,179.36.

Yet beneath the surface, caution is quietly building. Daily momentum indicators are flashing bearish divergence, suggesting upside conviction may be fading. Decisive break below 48,349.88 support would argue that a medium-term top is already in place, potentially marking the start of a broader correction to the whole up trend from 36,611.78 (2025 low).

10-year yield recovered after dipping to 4.025, but quickly recovered. While further fall is expected as long as 55 D EMA (now at 4.160) holds, strong support could emerge between 3.947 (October low) and 4.000 psychological level to floor downside.

Dollar Index Gains Tactical Support, But Easing Cycle Still Ahead

Dollar drew modest support last week as markets recalibrated expectations following the more hawkish FOMC minutes. Reduced odds of near-term easing gave the greenback a tactical boost, particularly against lower-yielding currencies. However, the move lacked strong follow-through.

Expectations remain that the policy stance will gradually turn less restrictive, particularly once Kevin Warsh formally assumes the Fed chairmanship. Under that leadership, rate cuts are still anticipated, though probably delivered later and at a less aggressive pace than previously priced.

Dollar Index resumed its rebound from the 95.55 short-term low and briefly pushed above its 55 D EMA (now at 97.59). That technical break suggests short-term momentum has improved, but it does not yet alter the bigger picture.

The broader structure still points to a corrective recovery rather than the start of a fresh bull cycle. Price action from 96.37 can be interpreted either as a completed three-wave pattern at 100.39 or as part of a larger expanding triangle. In both cases, upside should be capped below 100.39 resistance. Meanwhile, below 96.49 support will bring retest of 95.55 low. Firm break there will resume the medium term down trend.

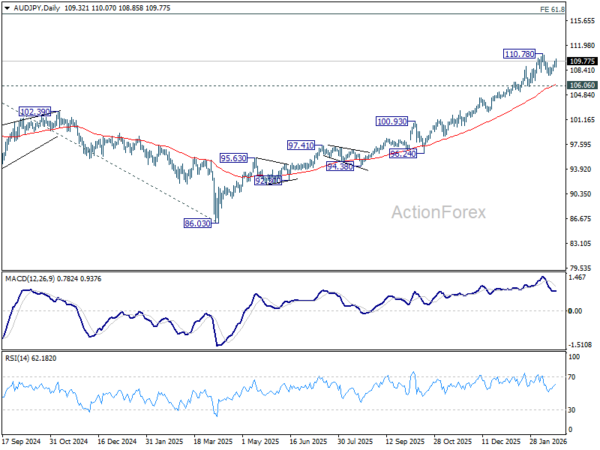

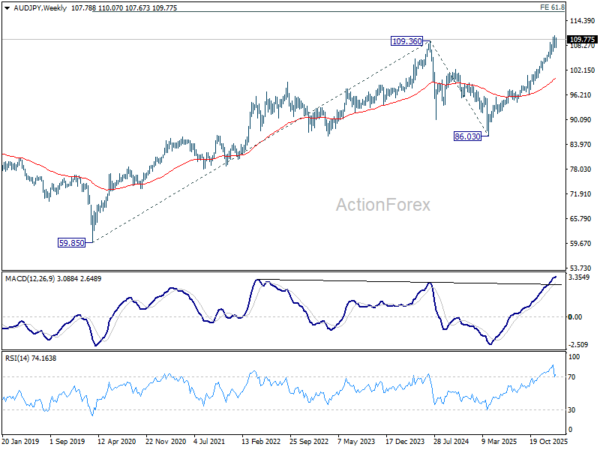

AUD/JPY Signals Calm: Risk Appetite Overrides Macro Noise

Among all the macro crosscurrents last week, AUD/JPY stood out as the clearest expression of investor sentiment. The cross ended as the top mover, gaining around 1.7% — a performance that would be highly unlikely in an environment of genuine panic.

The rally reflects a combination of domestic and global drivers. In Australia, expectations for further tightening from the RBA firmed following hawkish meeting minutes and a resilient labor market report. On the Japanese side, the Yen’s earlier post-election strength appears to be fading. As risk appetite stabilized, the currency resumed its familiar inverse relationship with global equities.

Technically, while more near-term consolidation below 110.78 cannot be ruled out, downside should be contained by 106.06 support, which sits near 55 D EMA (now at 106.23). As long as that floor holds, the broader uptrend remains intact, with the next medium-term target at 61.8% projection of 59.85 (2020 low) to 109.36 (2024 high) from 86.03 (2025 low) at 116.60. However, decisive break below 106.06 would send a very different signal — one of deteriorating risk sentiment – and drag AUD/JPY down for deeper correction.

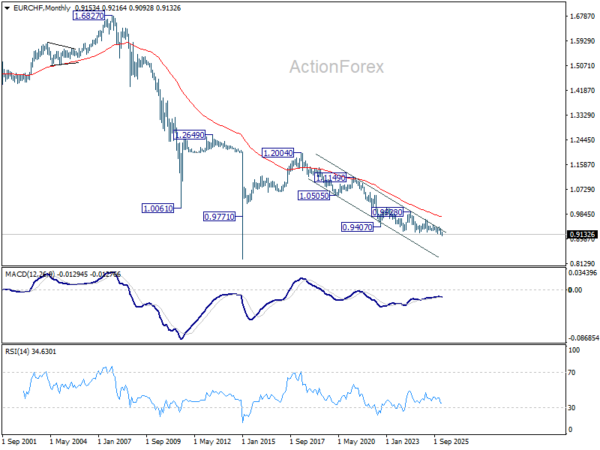

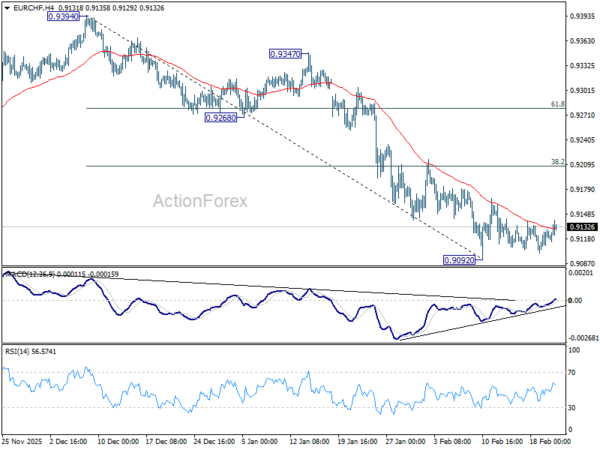

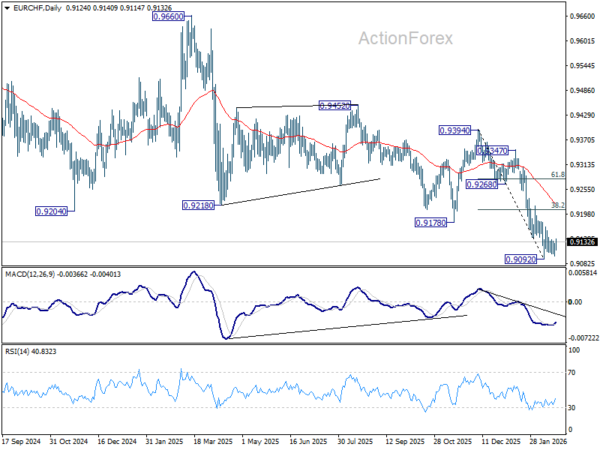

EUR/CHF Weekly Outlook

EUR/CHF stayed in range trading above 0.9092 low last week. Current development suggests that 0.9092 is already a short term bottom, and slightly lengthier consolidation is underway. Strong rebound might be seen to But upside should be limited by 38.2% retracement of 0.9394 to 0.9092 at 0.9207. On the downside, firm break of 0.9092 will resume larger down trend.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9326) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

In the long term picture, EUR/CHF is also holding well inside long term falling trend channel. Down trend from 1.2004 (2018 high) is still in progress. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9739) holds.