While US tariff chaos dominated headlines, its market impact has been surprisingly contained. Equities in Asia are brushing aside the latest escalation. In South Korea, the Kospi extended gains for a third consecutive session to fresh highs, signaling confidence that trade rhetoric has not yet translated into real economic disruption. Hong Kong’s Hang Seng Index also advanced strongly, reinforcing the view that regional investors are willing to look through Washington’s turbulence. Japanese markets were closed for holiday, limiting broader regional participation.

Currency markets paint a more nuanced picture. The clear underperformer is Dollar. The Supreme Court’s ruling against reciprocal tariffs and subsequent developments have shifted the debate beyond trade policy and into the realm of constitutional stability. For investors, the legal framework underpinning US trade measures now appears fluid and potentially contested. That perception of institutional instability is weighing on the Dollar more than the tariff level itself. It is no longer framed simply as a trade war, but as a legal and governance issue. This shift has helped fuel safe-haven flows into precious metals, with Gold and Silver extending gains alongside lingering Middle East war risk.

Among major currencies, Yen is the strongest performer, followed by Swiss Franc and Euro. Traditional defensive currencies are benefiting from Dollar weakness rather than outright risk aversion. Kiwi and Sterling sit mid-pack, reflecting balanced positioning. Australian Dollar is softer on the day but largely consolidating recent strength. Traders are reluctant to take fresh positions ahead of this week’s Australian CPI release, which could solidify expectations for further tightening by the RBA. Canadian Dollar is also under modest pressure, though downside is cushioned by firm oil prices. Markets are awaiting Q4 GDP data, which will determine whether the BoC can maintain its current policy stance without reopening easing debate.

Overall, the Supreme Court ruling is viewed as a procedural setback rather than a structural reversal of US trade policy. President Donald Trump’s quick move to raise global tariffs from 10% to 15% reinforces that the broader agenda remains intact.

International reaction, though, highlights increasing tension. The European Commission demanded clarity from Washington, insisting that terms of last year’s EU–US trade agreement be respected. “A deal is a deal,” officials stressed, highlighting concerns that unilateral changes undermine negotiated commitments.

India is reportedly rescheduling trade talks with Washington, pending evaluation of the latest developments. Meanwhile, China’s Commerce Ministry said it is conducting a “full assessment” of the ruling and urged the US to lift unilateral tariffs, warning that continued confrontation is harmful.

Lagarde says “I’m not done,” reaffirms commitment to ECB’s term

In an interview with CBS on Sunday, ECB President Christine Lagarde dismissed speculation that she could leave the the central bank before the end of her mandate. Reports had suggested an early departure might serve as political insurance to allow the French president to influence succession. Lagarde responded clearly that her “baseline” plan is to serve until the end of her term.

Lagarde emphasized her focus remains firmly on price stability and financial stability, highlighting that inflation has returned to target while growth, though not strong, is resilient at around 1.5%. She highlighted record-low unemployment across the euro area as evidence that policy normalization has achieved tangible results. However, she cautioned that consolidation is still required to safeguard those gains.

Her remarks aim to reinforce continuity at a time when markets are sensitive to leadership stability within major central banks. By stating “I’m not done,” Lagarde sought to anchor expectations that policy direction at the ECB will remain steady, with no abrupt shift tied to political developments.

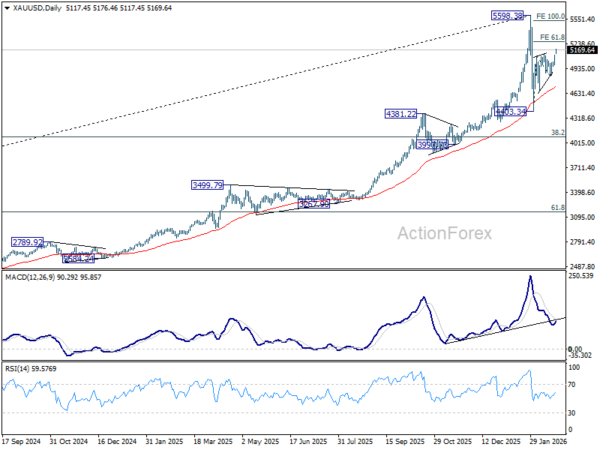

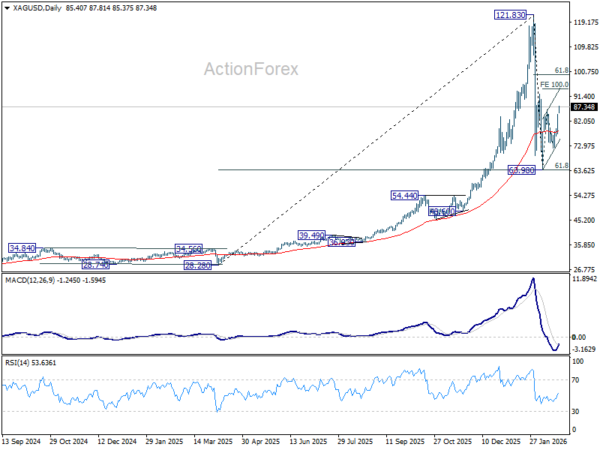

Tariff chaos and war risk put 5,530 in sight for Gold; Silver eyes 94+

Gold and silver extended their surge into early week trading, propelled by a “perfect storm” of US tariff confusion and escalating Middle East tension. The move defied earlier bearish expectations and marked a clear resumption of the rebound that began in early February.

In the near term, Gold’s decisive move back above 5,000 psychological level marks a clear turn in momentum. Further rise is expected to 5,270. Should geopolitical tensions escalate further, Gold has scope to extend toward 5,530. Silver is also advancing, with 94 emerging as the next target, though gains are likely to encounter resistance near 100 level. Given that the rally is being driven primarily by geopolitical risk rather than broad reflation dynamics, Gold is expected to outperform in terms of structure.

The primary catalyst remains policy instability in Washington. After the US Supreme Court struck down the administration’s reciprocal tariffs last week, President Donald Trump quickly countered by announcing a 10% blanket tariffs increase, but then be raised to 15% “effective immediately”, as written in a Truth Social post.

The complication lies in implementation. A formal White House proclamation signed Friday night maintained a 10% tariff rate effective 12:01 a.m. ET on February 24. Whether the higher rate is immediate or delayed matters less than the broader takeaway: policy direction appears fluid and unpredictable. For markets, uncertainty around legal basis, enforcement timing and tariff collection creates credibility risk.

At the same time, geopolitical risk in the Middle East has intensified. The White House issued a 10-to-15-day ultimatum for Iran to sign a new nuclear agreement, backed by a visible US military build-up. Key dates now anchor volatility expectations: nuclear talks are scheduled to resume in Geneva on February 26, full US naval deployment is expected in early March, and the unofficial deadline falls between March 5 and March 10.

In the background, additional support is emerging from Asia. Monday marked the first full trading session for many regional markets after Lunar New Year. Physical demand from China is re-entering a market already primed by last week’s developments. Broad-based Dollar softness has added incremental support.

Technically, Gold’s rebound from 4,403.34 resumed decisively after breaking above 5119.18 resistance. The move confirms that the second leg of the corrective pattern from 5598.38 high remains in progress. As long as 4990.81 holds as near-term support, further gains are favored.

Silver’s break above 86.28 similarly confirms continuation of its rebound from 63.98, viewed as the second leg of the corrective pattern from 121.83 peak. Upside remains intact while 79.78 holds, with 100% projection of 63.98 to 86.28 from 71.94 at 94.24 as next target. That said, Silver’s upside should be capped near 61.8% retracement of 121.83 to 63.98 at 99.73 to conclude the rebound.

Aussie CPI test, Canada GDP risk: Data week ahead

The final week of February finds global markets in a state of high alert. While investors are still grappling with US trade policy and geopolitical tensions, the focus is also on some “hard data” of inflation and growth. This week is defined by two high-stakes events that could trigger high volatility in the markets, and two “silent killers” that have the power to derail the current market equilibrium.

The High-Stakes Events:

First major event arrives from Australia. January Monthly CPI Indicator lands Wednesday, just weeks after the RBA raised rates to 3.85% with a hawkish tone. Headline CPI is expected to ease slightly to 3.7%, but focus will be on Trimmed Mean inflation — the RBA’s preferred gauge of underlying price pressure.

If Trimmed Mean prints at 3.3% or higher, market conviction around a May hike will harden further. Traders already assign high probability to another 25bps increase to 4.10%. Further out, implied yields suggest cash rate could peak between 4.20% and 4.45% into late 2026 should Q1 inflation fail to show meaningful moderation.

Friday shifts focus to Canada. Q4 GDP will test whether economic resilience is holding under tariff pressure. Bank of Canada remains on hold at 2.25%, and the OIS curve implies little policy change through year-end, with December 2026 pricing near 2.26%.

However, a flat or negative GDP reading could alter that narrative. It might force policymakers to reconsider easing, particularly if domestic demand shows strain.

The Silent Killers:

A potentially disruptive release is Tokyo CPI on Friday. As leading indicator for national inflation, it provides an early read on price momentum in Japan. Core CPI has eased to 2%, yet service inflation remains sticky, suggesting wage dynamics may still be firm. However, a weaker than expected Tokyo print would cast some doubts of whether BoJ is ready to act again in the near term.

US PPI also lands Friday and now carries elevated importance. After January FOMC minutes reintroduced hike optionality, producer price pressures are no longer secondary. Persistent input costs, especially linked to tariffs, would give hawkish members further justification to delay rate cuts.

Below are some highlights for the week:

United States (USD):

- Conference Board Consumer Confidence – Tuesday

- Producer Price Index (PPI) – Friday

- Fed Speakers: Several officials, including Governor Christopher Waller, are scheduled to speak.

Eurozone (EUR):

- German Ifo Business Climate – Monday

- Preliminary February Inflation (CPI) – Thursday/Friday: Major releases from Germany, France, and Spain.

Japan (JPY):

- Tokyo CPI – Friday

- Industrial Production & Retail Sales – Friday

Canada (CAD):

Australia (AUD):

- Australia Monthly CPI Indicator – Wednesday

China (CNY):

- Loan Prime Rate (LPR) Decision – Tuesday

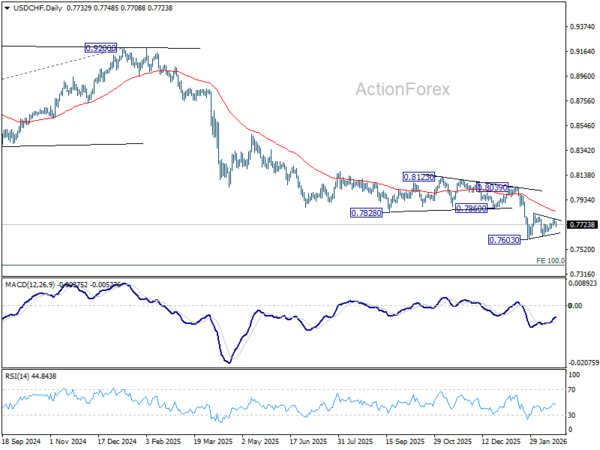

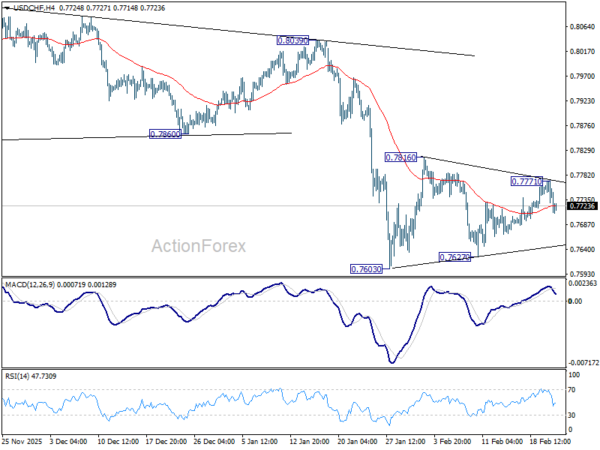

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7754; (R1) 0.7777; More….

USD/CHF dips mildly today but overall outlook is unchanged. Initial bias stays neutral and consolidations from USD/CHF’s consolidation pattern from 0.7603 could extend further. In case of stronger rise, upside upside should be limited by 55 D EMA (now at 0.7834) to complete the pattern. On the downside, below 0.7627 will bring retest of 0.7603. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.