Markets are turning cautiously positive as hopes build around a potential ceasefire that could reopen the Strait of Hormuz, easing the current supply-side shock. The tone has shifted from outright panic earlier in the week to a more measured phase of “probing for a bottom,” though conviction remains limited.

Oil remains the key anchor. Brent crude has eased back to around 100 level, suggesting that some war premium is being priced out. However, the move is tentative, reflecting that markets are not yet convinced a lasting resolution is imminent. Equities are responding more positively. Asian stock markets are rebounding as investors begin to price in the possibility of an “off-ramp” scenario, where tensions de-escalate and supply disruptions are reversed.

In contrast, currency markets are signaling greater skepticism. The performance profile still leans risk-off, with Aussie sitting at the bottom of the weekly ladder, followed by Kiwi and Loonie. On the other hand, Sterling is leading gains, with Euro and Yen also outperforming, while Dollar and Swiss Franc are holding in the middle.

This divergence highlights a key dynamic: while equities are pricing hope, FX markets remain focused on uncertainty and policy implications. The lack of alignment suggests that current optimism is still fragile and highly conditional.

At the center of the narrative is a reported 15-point ceasefire proposal from the US, delivered via Pakistani intermediaries. The plan outlines a one-month ceasefire designed to create a window for broader negotiations. For markets, the most critical element is the immediate reopening of the Strait of Hormuz. Such a move would quickly alleviate supply constraints, reduce energy prices, and ease global inflation pressures. In exchange, the US is reportedly offering full relief from economic sanctions, signaling a willingness to pursue a diplomatic off-ramp even as military pressure remains in place.

However, the response from Iran has been dismissive. Officials have described the proposal as “negotiating with themselves,” maintaining a defiant stance and reiterating demands for reparations and guarantees against future strikes. At the same time, the military backdrop remains tense. The Pentagon continues to deploy additional forces to the region, including elements of the 82nd Airborne, underscoring that escalation risks have not been removed.

This dual-track dynamic—diplomacy alongside military buildup—keeps markets in a state of cautious balance. Until there is concrete progress, such as a confirmed reopening of Hormuz, the current optimism is likely to remain constrained.

In Asia, at the time of writing, Nikkei is up 3.00%. Hong Kong HSI is up 0.81%. China Shanghai SSE is up 1.17%. Singapore Strait Times is up 0.76%. Japan 10-year JGB yield is down -0.014 at 2.257. Overnight, DOW fell -0.18%. S&P 500 fell -0.37%. NASDAQ fell -0.84%. 10-year yield rose 0.058 to 4.392.

Gold Price Today: Bounce Faces ‘Sell-the-Rally’ Test at 4,600–4,800 Resistance Cluster

Australia Inflation Eases Pre-War, RBA Still Faces Sticky Core Pressures

Pre-war data show modest easing in Australia inflation, though underlying pressures remain firm and could rise again as energy costs increase. Read more.

Fed Rate Cuts on Hold as Barr Seeks Clear Inflation Progress

Fed Governor Michael Barr signaled that rate cuts remain on hold, stressing the need for clear evidence that inflation is sustainably declining, with rising oil prices posing fresh risks. Read more.

Interest Rate Path May Shift as Fed’s Goolsbee Warns of New Inflation Shock

Fed’s Austan Goolsbee warned that a new energy-driven inflation shock could alter the interest rate path, stressing that rate cuts depend on clear progress toward 2% inflation. Read more.

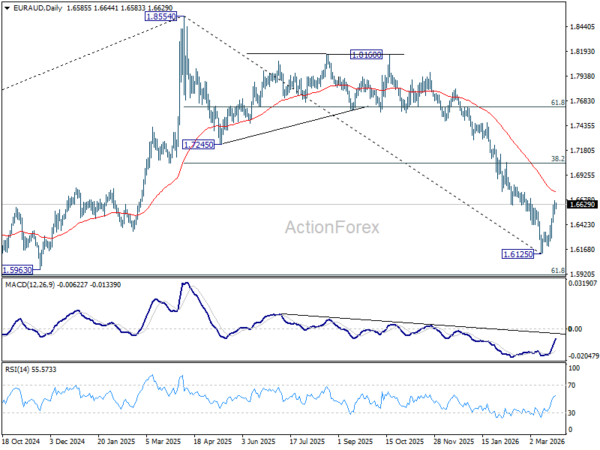

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6528; (P) 1.6600; (R1) 1.6664; More…

Intraday bias in EUR/AUD stays mildly on the upside at this point. Rebound from 1.6125 short term bottom should extend to 55 D EMA (now at 1.6757). Sustained break there will pave the way to 38.2% retracement of 1.8554 to 1.6125 at 1.7053. Nevertheless, below 1.6448 minor support will suggest that the recovery has completed, and bring retest of 1.6125 low.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7245) holds, even in case of strong rebound.