Asian equities surged to fresh record highs, with KOSPI jumping more than 2.5% and Nikkei advancing over 1.5%, extending what has become a powerful rally. The strength of the move signals more than just optimism—it reflects a market that is increasingly comfortable ignoring geopolitical noise and focusing on growth narratives.

The shift has been building since the announcement of the indefinite US–Iran ceasefire last week. While negotiations have stalled, the absence of escalation has been enough to anchor sentiment. With no escalation and no resolution, markets are treating geopolitics as background noise rather than a trading driver. Risk appetite has stabilized, and capital is rotating back into equities, particularly those linked to the AI theme.

Also, the focus now shifts decisively to monetary policy, with a dense lineup of central bank decisions scheduled for week.

The Bank of Japan kicks things off on Tuesday, and what was once a straightforward hold has turned into a genuinely “live” meeting. The base case is for no change at 0.75%, but rising and broadening inflation has reopened the door to a surprise hike toward 1.00%. Even if the BoJ stays on hold, the risk for markets lies in the messaging. Without a clear signal toward tightening, Yen weakness could intensify, especially with markets already pricing a strong probability of a June move. In that sense, a passive BoJ may be as market-moving as an active one.

Wednesday brings the Federal Reserve, where the outcome is far less uncertain but no less important. Rates are expected to be held at 3.50%–3.75% in what is likely to be Jerome Powell’s final meeting as Chair before the transition to Kevin Warsh. The decision itself may be uneventful, but the tone will not be. Markets will be watching for how the Fed frames oil-driven inflation risks and whether there are any signals around the pace or endgame of balance sheet reduction.

The Bank of Canada, also meeting on Wednesday, faces a different challenge. A hold is expected, but the focus will be on updated projections as policymakers weigh weak growth—GDP expanding just 0.7% in Q4—against rising fuel costs. The key question is whether the BoC chooses to look through the oil shock or signals concern about second-round inflation effects.

Thursday brings two major European decisions. The Bank of England is widely expected to hold at 3.75%, but its “Super Thursday” projections will be the real driver. With services inflation still persistent, any upward revision to medium-term inflation forecasts could shift expectations back toward tightening, even if rates remain unchanged for now. The risk is not in the decision, but in the signal.

The European Central Bank is also expected to stand pat, with the deposit rate held at 2.00%. The focus will be on President Christine Lagarde’s guidance, particularly whether she offers any clarity on the conditions required for a hike in June. For now, the ECB is firmly data-dependent, but markets are sensitive to any hint of timing or thresholds that could anchor expectations for the next step.

The macro calendar is equally demanding. US GDP, ISM manufacturing, and PCE inflation will provide key insights into the strength of the US economy and inflation trends. In addition, Eurozone GDP and CPI flash estimates, Canada GDP, and Australia CPI will all feed into global policy expectations, ensuring that markets remain highly reactive to incoming data.

In FX markets, the risk-on backdrop is clearly visible. Aussie is leading gains, supported by expectations of strong inflation data. Kiwi and Euro are also firm, while Dollar is under pressure. Swiss Franc and Sterling are lagging, while Yen and Loonie are holding in the middle.

In Asia, at the time of writing, Nikkei is up 1.47%. Hong Kong HSI is down -0.33%. China Shanghai SSE is up 0.09%. Singapore Strait Times is down -0.53%. Japan 10-year JGB yield is up 0.026 at 2.467.

Oil Stalls as ‘Frozen Conflict’ Replaces Escalation Fears in US–Iran Standoff

AUD/JPY Eyes Breakout Toward 120 as BoJ Decision and Australia CPI Set Up High-Stakes Week

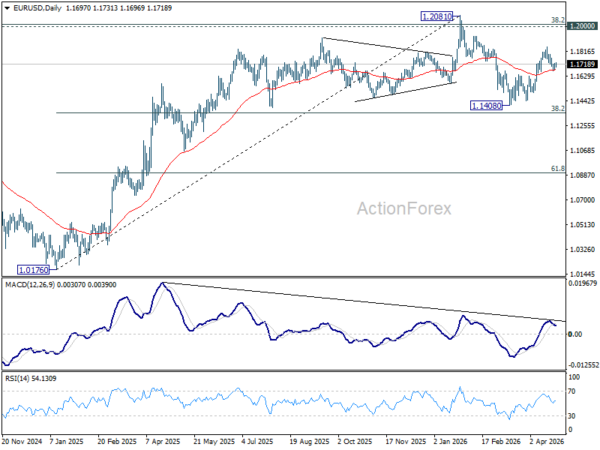

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1688; (P) 1.1706; (R1) 1.1741; More….

Intraday bias in EUR/USD remains neutral for the moment, and more consolidations could be seen. But further rally is expected with 1.1662 support intact. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1530). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.