Euro jumped notably higher following reports that Germany’s political leaders have reached a crucial agreement on the historic debt deal. According to sources close to the negotiations, Chancellor-in-waiting Friedrich Merz and the Greens have agreed on a massive increase in state borrowing, just days before a decisive parliamentary vote next week. While some details are still being finalized, the development marks a major step toward unlocking substantial funding for infrastructure, military expansion, and economic revival in Europe’s largest economy.

Merz has been pushing for the outgoing German parliament to approve a EUR 500B infrastructure fund alongside sweeping reforms to borrowing rules that would provide greater fiscal flexibility for future investments. However, securing a two-thirds majority for constitutional changes requires support not only from his own conservative bloc and his likely coalition partner, the Social Democrats , but also from the Greens. With the Greens now onboard, the proposal has gained significant momentum, boosting confidence in Germany’s economic outlook and supporting Euro in currency markets.

Overall for the week, Euro’s rally has helped it reclaim the top-performing spot, solidifying its strong positioning as trading nears a close. New Zealand Dollar has also performed well, buoyed by upbeat manufacturing data from New Zealand, which signaled faster-than-anticipated recovery. Meanwhile, British Pound has slipped to third place after UK GDP unexpectedly contracted in January.

At the other end of the spectrum, Swiss Franc and Japanese Yen are the weakest performers. Canadian Dollar has also struggled amid trade war uncertainties, keeping it in the lower tier of performers. Dollar and Australian Dollar are mixed, positioning somewhere in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.67%. DAX is up 1.92%. CAC is up 1.21%. UK 10-year yield is up 0.092 at 4.725. Germany 10-year yield is up 0.085 at 2.939. Earlier in Asia, Nikkei rose 0.15%. Hong Kong HSI rose 0.25%. China Shanghai SSE rose 0.23%. Singapore Strait Times fell -0.06%.

Japan 10-year JGB yield fell -0.002 to 1.544.

UK GDP down -0.1% mom in Jan, production drags while services support

The UK economy shrank by -0.1% mom in January, falling short of market expectations for a modest 0.1% expansion. The decline was primarily driven by weakness in the production sector, which saw output fall by -0.9% mom , while construction activity also dipped by -0.2% mom. On the other hand, the services sector—accounting for the bulk of the UK economy—managed a modest 0.1% mom gain, helping to cushion the overall contraction.

The broader three-month growth trend is weak too, with real GDP estimated to have expanded by 0.2% in the three months to January 2025 compared to the three months ending in October 2024. Services led the way with a 0.4% rise, while construction also posted a similar 0.4% gain. However, the production sector continued to struggle, contracting by -0.9% over the same period.

NZ BNZ manufacturing hits 53.9 as recovery gains unexpected momentum

New Zealand’s BusinessNZ Performance of Manufacturing Index rose from 51.7 to 53.9 in February, marking its highest level since August 2022.

This solid improvement was driven by stronger production (52.4) and new orders (51.5), both also reaching their best levels since August 2022. Meanwhile, employment surged to 54.0, climbing 3.2 points from January and hitting its highest level since September 2021.

Despite the stronger data, business sentiment remains cautious. The proportion of negative comments from respondents rose to 59.5% in February, up from 57.7% in January. Many manufacturers cited weak orders and sluggish sales as ongoing challenges, signaling that while expansion has resumed.

BNZ’s Senior Economist Doug Steel welcomed the sustained improvement, noting that “pickup may be a bit faster than we are currently forecasting”.

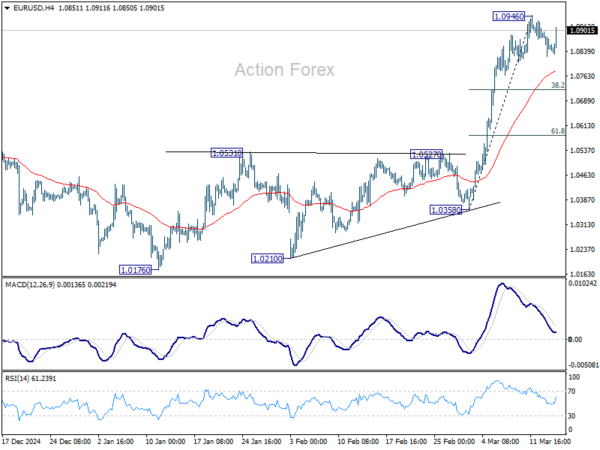

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0818; (P) 1.0857; (R1) 1.0892; More…

EUR/USD recovers mildly but stays below 1.0946 temporary top. Intraday bias remains neutral and more consolidations could be seen. In case of another fall, downside should be contained by 38.2% retracement of 1.0358 to 1.0946 at 1.0721. On the upside, break of 1.0946 will resume the rally from 1.0176 to retest 1.1274 key resistance next.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.