Is USD/JPY heading back to 160? For now, the answer is no—but the risk is clearly building as global yield dynamics shift and geopolitical tensions intensify. The Yen is back under pressure today, driven primarily by widening rate differentials as US and European yields continue to climb.

The US 10-year Treasury yield has surged above 4.45% and is now approaching the key 4.5% mark, a level that has previously acted as a psychological ceiling. The move is being fueled by a combination of factors: renewed geopolitical tensions in the Middle East, rising inflation concerns linked to higher energy prices, and a shift in Federal Reserve expectations away from rate cuts.

Energy markets remain on high alert as the fragile ceasefire between the US and Iran shows signs of breaking down. Elevated oil prices are reinforcing inflation risks, which in turn are pushing bond yields higher. Markets are increasingly concerned that sustained energy-driven price pressures could delay disinflation and force the Fed to tighten policy again.

This repricing is already visible in interest rate markets. Fed funds futures are now assigning nearly a 30% probability of a rate hike by year-end, while expectations for rate cuts have largely been priced out. The shift marks a significant turnaround in policy expectations and is providing strong support for US yields.

The global yield move is not limited to the US. Germany’s 10-year Bund yield has risen above 3.05%, while the UK 10-year gilt yield has climbed to 5.04%. These moves reflect both the global nature of the inflation shock and the possibility that the ECB and BoE would also need to maintain or even tighten policy at the next meeting.

For the Yen, widening yield differentials are once again driving weakness. USD/JPY has rebounded following last week’s sharp decline, though the current move still appears to be driven more by short covering than fresh directional positioning.

That said, the outlook could change quickly if key thresholds are breached. A sustained move in US 10-year yields above 4.5% would likely trigger a stronger wave of algorithmic selling in the Yen, amplifying upward pressure on USD/JPY. At the same time, a further rise in oil prices toward the $120 level would reinforce inflation fears and strengthen the case for higher global yields.

Intervention risk remains a complicating factor. Japanese authorities are reported to have deployed more than USD 30 billion in last week’s operations that helped push USD/JPY back toward the 155 area. Officials have also signaled a willingness to act again, even during the Golden Week holiday period.

However, intervention may prove less effective if underlying market forces intensify. Acting against a backdrop of rising yields and surging oil prices would present a much more difficult challenge. In such a scenario, attempts to stabilize the Yen could slow the move, but are unlikely to reverse the broader trend.

For now, USD/JPY remains contained within last week’s range, suggesting that markets are not yet fully committed to a renewed push higher. But with yields and oil prices approaching key trigger levels, the risk of a move back toward 160 is no longer hypothetical—it is conditional.

For the day so far, Yen is currently the worst performer, followed by Dollar, and then Euro. Kiw is the strongest, followed by Aussie and then Loonie. Sterling and Swiss Franc are positioning in the middle.

Swiss CPI Accelerates to 0.6% YoY as Energy Import Costs Rebound

RBA Hikes to 4.35%, Signals It’s Not Done Yet

RBA raise interest rate as expected, and signaled a clear shift to higher-for-longer policy. Inflation is now expected to peak higher and fall more slowly, while growth forecasts are being downgraded. With rates projected near 4.7% through 2028, the central bank is preparing for a prolonged fight against persistent price pressures. Read more.

Gold Slides on Hormuz Attacks, 4,400 Breakdown in Focus, 4,000 Next

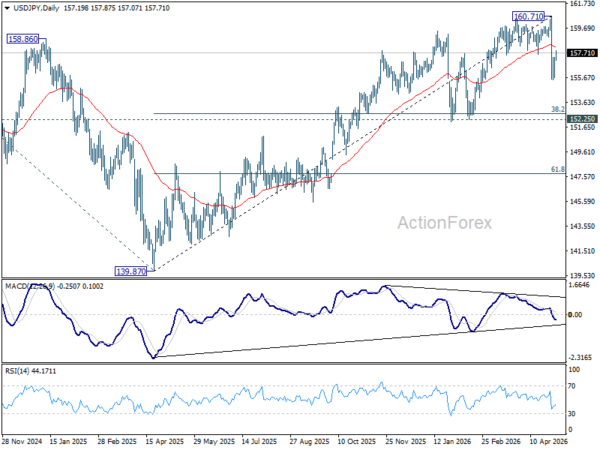

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.22; (P) 156.76; (R1) 157.79; More…

USD/JPY’s recovery from 155.48 accelerates higher today, but it stays below 55 4H EMA (now at 158.27). Intraday bias remains neutral and further decline is still in favor. Below 156.55 minor support will bring retest of 155.48. Break there will extend the fall from 160.71 and target 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74). However, sustained break of the 55 4H EMA will bring stronger rebound back to retest 160.71 high.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.03) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.