Markets appear to be entering a new phase of post-conflict positioning, with oil prices falling again on hopes of a full reopening of the Strait of Hormuz while precious metals begin rebuilding bullish momentum. The sharp moves across commodities suggest investors are increasingly looking beyond the immediate US-Iran conflict and starting to reposition for a more normalized global macro environment.

The clearest signal is coming from oil markets. Brent crude extended its decline again today and broke below the $97 level, while WTI moved closer toward the key $90 handle. The price action suggests traders are becoming increasingly confident that the Strait of Hormuz could soon reopen fully to international shipping and energy flows if a peace agreement between Washington and Tehran materializes.

Oil traders now appear increasingly hopeful that commercial normalization could return to the region, allowing tankers to move freely again without disruption or informal “tolls” imposed by Iran’s Islamic Revolutionary Guard Corps on vessels passing through the Strait. That shift represents a major unwind of the geopolitical premium that had fueled the earlier oil surge.

Elsewhere, equities and currencies were notably calmer today after this week’s powerful risk-on rally. US stock futures traded largely steady following the record-breaking gains in S&P 500 and NASDAQ earlier in the week. Dollar also stabilized within recent ranges and appears to be awaiting a fresh directional catalyst from broader market sentiment.

Meanwhile, the strongest momentum today has shifted toward precious metals, particularly Silver. Silver surged above the psychologically important $80 mark, significantly outperforming Gold and reinforcing the idea that investors are increasingly rotating back into higher-beta opportunities rather than pure defensive positioning.

Some investors are already beginning to argue that the record-breaking bull markets in Gold and Silver could resume later this year if a durable US-Iran peace settlement is achieved and the temporary pressure from higher interest rates fades. Both metals posted extraordinary gains during 2025, with Gold surging 66% and Silver soaring 135%, before experiencing sharp and volatile corrections this year.

Recent declines in precious metals had been driven by fears of higher interest rates, a stronger Dollar linked to rising oil prices, and heavy position liquidation during periods of market stress. But as oil retreats and the inflation shock potentially eases, investors are revisiting the longer-term structural bullish case for metals.

That longer-term story remains centered on central bank diversification away from US government debt, persistent physical Silver supply tightness, and expanding demand tied to green energy technologies and AI infrastructure. In many ways, the US-Iran conflict may have strengthened rather than weakened those structural themes by reinforcing the strategic importance of energy diversification and renewable technologies.

For now, markets appear to be transitioning away from “war panic” and toward “post-conflict positioning.” Oil is pricing normalization, equities are consolidating record highs, and Silver’s breakout suggests investors are once again willing to chase higher-beta opportunities tied to long-term structural growth themes.

In the currency markets, for the week so far, Kiwi is the best performer, followed by Aussie, and then Swiss Franc. Loonie is the worst, followed by Dollar, and then Sterling. Euro and Yen are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.05%. CAC is up 0.09%. UK 10-year yield is down -0.035 at 4.913. Germany 10-year yield is down -0.026 at 2.980. Earlier in Asia, Nikkei surged 5.58%. Hong Kong HSI rose 1.57%. China Shanghai SSE rose 0.48%. Singapore Strait Times rose 0.30%. Japan 10-year JGB yield fell -0.023 to 2.483.

Silver Breaks 80 as Markets Rotate From Defense to Offense

US Jobless Claims Edge Higher to 200k, Labor Market Still Stable

Eurozone Retail Sales Slip -0.1% mom in March as Fuel Demand Weakens

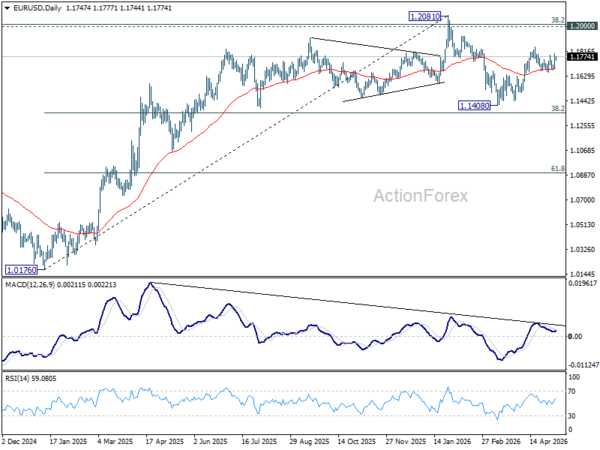

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1693; (P) 1.1746; (R1) 1.1801; More….

Outlook in EUR/USD is unchanged as range trading continues. Intraday bias remains neutral, and with 1.1642 support intact, rise from 1.1408 is expected to continue. On the upside, firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.