The market narrative is becoming more complicated. Dollar and oil are rising again as Iran negotiations stall, yet semiconductor-driven equity rallies continue pushing Asian tech markets higher, highlighting how AI momentum is still partially insulating risk assets from geopolitical stress.

Markets entered the weekend expecting at least some form of diplomatic breakthrough between Washington and Tehran. Instead, they woke up Monday facing another reminder that the Middle East crisis may be drifting into something much longer and more dangerous than a simple “deal or war” scenario. Oil prices jumped sharply, Dollar rebounded broadly, and traders began rebuilding geopolitical risk premium after the highly anticipated US-Iran agreement failed to materialize.

Brent crude surged back above $105 after Iran rejected the Trump administration’s hardline 14-point memorandum of understanding. Tehran responded with its own counterproposal, reportedly demanding immediate sanctions relief, a broader regional military halt, and a phased long-term approach toward nuclear restrictions. US President Donald Trump responded late Sunday with a series of Truth Social posts calling the proposal “TOTALLY UNACCEPTABLE,” signaling that negotiations remain deeply deadlocked.

Yet the broader market reaction was far from classic panic. Gold softened and slipped back below $4700, while Asian technology stocks continued powering higher. South Korea’s KOSPI exploded another 4.5% to fresh record highs as semiconductor names extended their AI-fueled rally. Strong leads from US technology stocks again overwhelmed regional geopolitical concerns. Japan’s Nikkei also briefly touched fresh record highs before pulling back modestly.

The divergence across asset classes was striking. Oil and Dollar traded like geopolitical stress mattered again. Equities, particularly semiconductors, continued trading as though the AI cycle remained the dominant force in global markets. That split may continue to be the defining theme for the week ahead.

Attention is now shifting toward Trump’s upcoming state visit to China from May 13–15, the first trip by a US president to Beijing in nearly nine years. Trump and Xi Jinping are expected to discuss trade, Taiwan, artificial intelligence competition, rare earth export restrictions, and perhaps most critically, the Iran conflict and Hormuz security situation.

There is also a growing theory circulating across markets that Iran may intentionally be delaying negotiations until after the Trump-Xi summit. That could be referred to as the “Dragon Factor” — the belief that Tehran hopes China could negotiate some form of energy-security arrangement or oil corridor that weakens US leverage over Hormuz and sanctions enforcement. Whether realistic or not, the theory highlights how deeply interconnected geopolitics, trade, and energy markets have become.

Before the summit itself, Chinese Vice Premier He Lifeng and US Treasury Secretary Scott Bessent are expected to meet in South Korea on Wednesday for preliminary trade discussions. Any signs of coordination between Washington and Beijing regarding energy stability could quickly become the single most important driver for oil markets.

Meanwhile, this week also carries major monetary policy implications. On Tuesday, the US Senate is expected to approve Kevin Warsh as the next Federal Reserve Chair ahead of Jerome Powell’s departure later this week. Inflation data will follow closely behind, with April CPI forecast to rise to 3.7% yoy while Core CPI could accelerate to 2.9%. If energy-driven inflation begins spilling further into core prices, markets may have to reassess whether the current “Fed on hold” consensus can survive a prolonged oil shock.

Other major releases include the BoC Summary of Deliberations, which is expected to reinforce a cautious hold stance despite mounting oil-driven inflation pressure. German ZEW sentiment is likely to deteriorate further as industrial weakness deepens, while UK GDP later this week may show the first meaningful “war drag” from higher energy cost

In currency markets today, Dollar is currently the strongest performer, followed by Loonie and Euro. Kiwi is the weakest, followed by Swiss Franc and Sterling. Aussie and Yen are trading more mixed.

In Asia, at the time of writing, Nikkei is down -0.37%. Hong Kong HSI is down -0.36%. China Shanghai SSE is down -0.31%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.35%. Japan 10-year JGB yield is up 0.033 at 2.510.

| Event | Timing | Market Focus |

|---|---|---|

| Trump-Xi Summit | May 13–15 | Trade, AI, Taiwan, rare earths, Iran/Hormuz |

| He Lifeng–Bessent Meeting | May 13 | Pre-summit US-China economic and trade discussions |

| Fed Chair Transition Vote | May 12 | Senate vote on Kevin Warsh replacing Powell |

| US CPI | May 12 | Headline CPI expected at 3.7% yoy. Core at 2.9%. |

| BoC Summary of Deliberations | May 13 | Oil shock vs rate hold debate |

| German ZEW Sentiment | May 12 | Weak industrial outlook and trade deterioration |

| UK GDP | May 14 | Economic impact of energy shock |

US-Iran Peace Deal Failed — Brent Oil’s Triangle Pattern Warns Bigger Shock Ahead

China Inflation Heats Up as PPI Hits 45-Month High

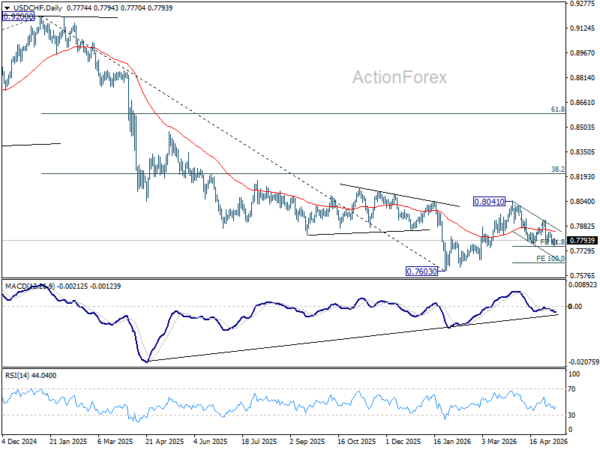

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7746; (P) 0.7777; (R1) 0.7793; More….

Intraday bias in USD/CHF is turned neutral again with current recovery. On the downside, decisive break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will resume the whole decline form 0.8041, and target 100% projection at 0.7656. However, firm break of 0.7847 resistance will indicate short term bottoming, and bring stronger rebound back to 0.7923 resistance.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.