Dollar weakened broadly in early US trading today, though price action remained largely rangebound against most major currencies as markets struggled to find a decisive macro direction. Elevated Treasury yields, with the US 10-year yield holding near 4.5%, continued offering support to the greenback even as softer-than-expected monthly PCE inflation data eased immediate fears of sharp near-term inflation acceleration. At the same time, ongoing uncertainty surrounding the US-Iran conflict prevented investors from aggressively rebuilding short Dollar positions.

The latest inflation figures were generally viewed as modestly reassuring for markets. Both headline and core monthly PCE readings came in slightly below expectations, reinforcing the recent message from Federal Reserve officials that policymakers are not rushing toward tightening despite increasingly vocal concerns over persistent oil-driven inflation risks.

With the federal funds rate already sitting in a mildly restrictive 3.50–3.75% range, many policymakers appear comfortable maintaining a wait-and-see approach while assessing whether the energy shock develops into broader second-round inflation pressure. Unlike Europe, the United States also retains a relative advantage through greater energy independence, allowing the Fed more flexibility to treat recent oil volatility as a temporary supply-side distortion rather than an immediate monetary-policy emergency.

Nevertheless, the geopolitical backdrop remains highly fragile. The United States and Iran continue exchanging direct military strikes even while negotiations toward a potential interim agreement remain alive. Markets still appear to view diplomacy as the most likely endgame, however, with Brent crude unable to sustain rallies toward the key $100 psychological level despite renewed escalation headlines. That relatively restrained oil behavior suggests investors are not yet pricing a full regional energy shock scenario, even if confidence in a rapid agreement has faded.

In currency markets, Kiwi remained the week’s strongest performer following the hawkish hold from the Reserve Bank of New Zealand, which sharply increased expectations for another rate hike in coming meetings. Euro stayed firmly supported after the latest European Central Bank meeting accounts revealed policymakers were already debating hikes aggressively back in April, reinforcing expectations for tightening in June. Aussie remained surprisingly resilient despite softer domestic inflation data, suggesting broader risk sentiment remains constructive.

Meanwhile, Swiss Franc lagged as elevated global yields continued weighing on traditional low-yielding defensive currencies. Loonie remained pressured by the sharp collapse in oil prices earlier in the week. Sterling and Dollar are trading near the middle of the weekly performance rankings.

Oil Holding Below $100 Suggests Markets Still See Room for a US-Iran Deal

Iran Peace Hopes Collapse After New Strikes as Gold Eyes 4,000 and Silver Tests 70

ECB Minutes Reveal June Rate Hike Momentum Growing Rapidly

US Core PCE Inflation Stays Hot as Annual Price Pressures Accelerate to 3.3%

US Durable Goods Orders Smash Forecasts as Transportation Demand Jumps

US Jobless Claims Edge Higher to 215k as Continuing Claims Rise Too

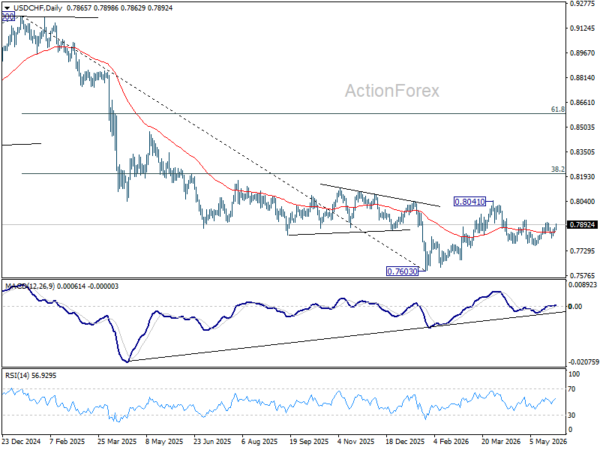

USD/CHF Daily Outlook

Intraday bias in USD/CHF remains neutral first. Firm break of 0.7906/23 will indicate that fall from 0.8041 has already completed as a correction. Further rally should be seen to retest 0.8041. On the downside, though, below 0.7807 will resume the fall from 0.8041 through 0.7760.

In the bigger picture, as long as 55 W EMA (now at 0.8035) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.