Dollar regained momentum today as two important market narratives moved in its favor simultaneously. First, investors became increasingly skeptical that a US-Iran agreement would be reached quickly, pushing oil prices higher again. Second, stronger-than-expected US employment data reinforced confidence in the economy and strengthened the case for maintaining restrictive monetary policy. Together, those developments helped lift the Dollar broadly across the foreign exchange market.

The biggest shift came from the geopolitical front. Brent crude climbed through $98 as traders reassessed the likelihood of a near-term diplomatic breakthrough. While US President Donald Trump said Iran had agreed not to possess nuclear weapons, he also warned that the country could still reverse its position. Meanwhile, hostilities continued to flare in the Gulf region, with attacks in Kuwait highlighting the fragile security environment. Markets appear to be pricing not an immediate escalation, but a prolonged period of uncertainty that keeps a risk premium embedded in energy prices and sustains inflation concerns.

The second pillar of Dollar strength came from the labor market. ADP private employment increased by 122k in May, beating expectations and indicating hiring remains healthy. Wage growth also remained elevated, suggesting underlying inflation pressures have not faded. The report reinforces the view that the Fed does not need to worry about labor-market weakness and can remain focused on inflation risks. Markets now see around a 60% probability of a Fed rate hike by the end of the year, a figure that could rise further if oil prices stay elevated at current or even higher levels.

Adding to the inflation story was a new trade development. The Office of the U.S. Trade Representative proposed additional tariffs of up to 12.5% on imports from 60 economies, including China, the European Union, and Japan. If implemented, the measures would add another source of upward pressure on import costs at a time when energy-driven inflation risks are already increasing.

Against this backdrop, the divergence between the US and Eurozone remains a key driver in currency markets. While the ECB is expected to raise rates next week, weak PMI surveys suggest recession risks are rising. The Fed, by contrast, faces an economy that continues to generate jobs and absorb higher interest rates. That difference in growth dynamics is helping preserve the Dollar’s yield advantage.

Among major currencies, Dollar emerged as the strongest performer of the day so far. Yen ranked second as intervention warnings from Japan slowed the advance in USD/JPY, while Canadian Dollar benefited from the rebound in crude oil. Commodity-linked currencies such as Aussie and Kiwi struggled alongside Swiss Franc as markets shifted toward a more defensive posture. The combination of rising oil, resilient US data, and fading hopes for a quick Iran deal is increasingly becoming a powerful Dollar story.

US ADP Employment Tops Forecasts With 122k Growth as Hiring Broadens Across Industries

Market Heard Japan’s Intervention Warning. But USD/JPY 160 Test Still Alive.

Eurozone PPI Jumps 0.6% mom, 4.9% yoy as Pipeline Inflation Pressures Build

Eurozone PMI Signals 4% Inflation and GDP Contraction. ECB Faces Tough Choice.

UK Services PMI Finalized Below 50 as Inflation and Geopolitics Hurt Confidence

Bitcoin’s Next Stop Could Be $60k. The Bigger Risk May Be $40k.

Australia Q1 GDP Grows 0.3% qoq, Misses Forecasts as Exports and Mining Drag Growth

Japan’s PMI Services Stagnates While Cost Pressures Surge

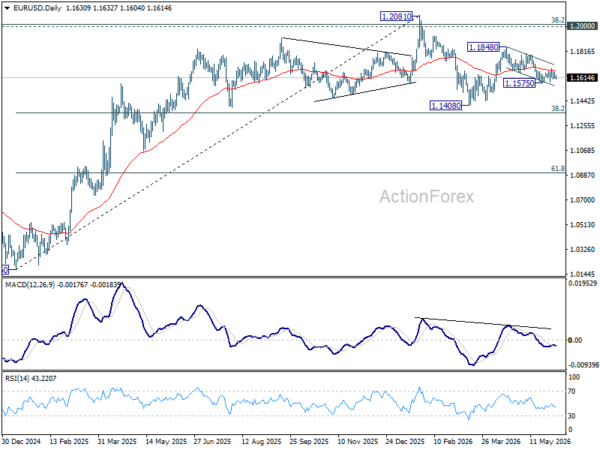

EUR/USD Daily Outlook

Intraday bias in EUR/USD stays neutral as range trading continues. On the downside, break of 1.1575 support will resume the fall from 1.1848 to retest 1.1408 low. Above 1.1865 will target 1.1795 resistance. Firm break there will argue that rise from 1.1408 is ready to resume through 1.1848.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1542). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.