Swiss Franc has emerged as one of the weakest major currencies this week. As US-Iran negotiations drag on without a clear resolution, markets are steadily pricing out a swift agreement. Brent crude remains well above $90 and is threatening a return to triple-digit territory. While the situation has not escalated into a broader regional conflict, the persistence of high energy costs is increasingly feeding inflation concerns across Europe and North America.

This is where Switzerland’s problem begins. For the ECB, BoE, and even the Fed, oil above $90 is a policy headache. Every week that energy prices stay elevated increases the risk that businesses pass higher costs on to consumers, workers demand higher wages, and inflation becomes embedded again. Central bankers across Europe are increasingly talking about “second-round effects” and the need to act preemptively. Markets are now treating a June ECB hike as almost certain and continue to debate how many additional hikes could follow. Even the Fed is seeing growing discussion about whether another increase might eventually be needed.

The SNB, by contrast, is living in a different world. May CPI to be released today is expected at just 0.8%. Not 2.8%. Not 3.8%. Just 0.8%. That number would still sit comfortably within the SNB’s target range and near the lower end of what policymakers consider desirable. While other central banks are worrying about inflation becoming entrenched, the SNB is worrying about almost nothing at all. Chairman Martin Schlegel has signaled this week that medium-term inflation pressures remain broadly unchanged and that price stability is maintained.

Ironically, that stability is becoming a weakness. Currency markets reward central banks that are expected to tighten. They punish central banks that have no reason to do anything. Every additional day of elevated oil prices strengthens the argument for tighter policy elsewhere while reinforcing expectations that the SNB can remain comfortably parked at 0.00%. In effect, the US-Iran stalemate is widening monetary-policy divergence even without a single additional missile being fired.

That divergence is increasingly showing up in the charts. EUR/CHF’s break above 0.9169 resistance suggests the pullback from 0.9264 has already completed at 0.9094. As long as 0.9137 minor support holds, a retest of 0.9264 should be seen. Firm break there resume the rally from 0.8979 and target 100% projection of 0.8979 to 0.9264 from 0.9094 at 0.9379. Break of 0.9137, however, will dampen this bullish view and mix up the outlook.

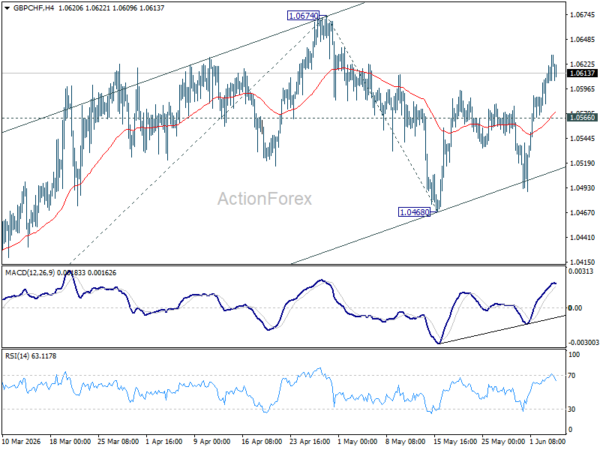

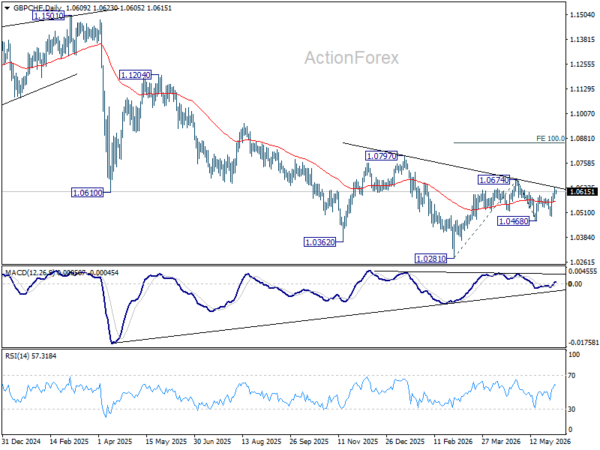

GBP/CHF is showing a similar structure, with the correction from 1.0674 likely ending at 1.0468. A move back to 1.0674 should be seen first. Firm break there will resume the rally from 1.0281 and target 100% projection of 1.0281 to 1.0674 from 1.0468 at 1.0861. However, below 1.0566 minor support turn bias neutral again first.

The key risk to this view remains a sudden collapse in oil prices. A breakthrough in US-Iran negotiations that rapidly removes geopolitical risk premiums from energy markets would immediately reduce inflation concerns in Europe and the UK. That would diminish the need for further policy tightening and narrow the divergence that is currently weighing on Swiss Franc. Until such a development occurs, however, the path of least resistance appears to favor higher EUR/CHF and GBP/CHF.