Global markets were gripped by a technology-led selloff today, with investors abruptly shifting their attention away from the fading Middle East energy shock and toward mounting concerns over stretched valuations, leverage, and financial conditions. The sharp decline in Asian equities spilled into Europe and U.S. futures, driving classic risk-off positioning across currencies. Yen led gains, followed by Dollar and Swiss Franc, while Aussie, Kiwi and Euro underperformed.

The immediate catalyst appeared to come from South Korea, where the KOSPI plunged -9.99%, its steepest drop in more than three months. The selloff was severe enough to trigger a mandatory 20-minute market-wide trading halt. Unlike many sudden market declines, this move was not driven by a vague deterioration in sentiment. Instead, it followed comments from Financial Supervisory Service Governor Lee Chan-jin, who expressed deep regret over approving a large batch of highly leveraged single-stock ETFs linked to Samsung Electronics and SK Hynix. The remarks triggered a rapid unwinding of an estimated USD 9.1B retail-heavy leveraged trade, amplifying selling pressure throughout the broader market.

Japan, however, appeared to be experiencing something more than simple contagion from Korea. The Nikkei 225 fell -3.55%, while the Nikkei Semiconductor Stock Index plunged more than -9%. The scale of the losses suggested a broader liquidation of technology and AI-related positions rather than merely a reaction to events in Seoul. Weakness then spread beyond Asia, with NASDAQ futures trading more than -2.5% lower in European hours, raising concerns that investors are beginning to reassess the lofty valuations built during the AI-driven rally.

Not everyone sees the selloff as a fundamental threat to the long-term AI story. Many economists and market strategists continue to argue that artificial intelligence will drive earnings growth for years to come and justify massive capital expenditure programs. From that perspective, today’s weakness could ultimately prove to be a buying opportunity rather than the beginning of a bear market. However, even the strongest secular trends are vulnerable to cyclical corrections, particularly after periods of aggressive positioning and elevated valuations.

A more immediate concern for markets is the relationship between the Yen and Japanese equities. The Nikkei reached a record high of 72,353.96 just yesterday, helped significantly by USD/JPY’s rise to a multi-decade high near 161.7. A weak Yen has been a major pillar supporting Japanese exporters by boosting overseas earnings when translated back into local currency. That relationship now risks working in reverse.

If risk aversion continues to drive investors into the Yen, a stronger Japanese currency would undermine earnings expectations for exporters and place additional pressure on the Nikkei. Further declines in equities could then reinforce global risk aversion, generating additional safe-haven demand for Yen and creating a self-reinforcing cycle. Such feedback loops have played a significant role during previous global deleveraging episodes. With the Yen still close to multi-decade lows against Dollar, the potential magnitude of any reversal could be amplified.

Meanwhile, not all developments were negative. On the geopolitical front, the United States took another major step toward normalizing relations with Iran by issuing a broad 60-day exemption allowing Iranian crude oil, petroleum products and petrochemicals to be traded in U.S. dollars through August 21. The move represents the most significant rollback of U.S. oil sanctions since the 1979 Islamic Revolution and follows positive progress in Swiss negotiations aimed at securing a permanent peace agreement. Together with last week’s memorandum of understanding, the measures continue to remove the energy shock premium that dominated markets earlier this year. Ironically, just as one major source of market anxiety fades, investors appear to have discovered another.

Gold’s $4,000 Floor Faces Fresh Threat as Tech Rout Fuels Dollar Surge

UK PMI Signals Second Month of Contraction as Services Slump Deepens

Eurozone PMI: Economy Stays Out of Recession as Services Recover

Katayama-Bessent Talks Trigger Mild USD/JPY Pullback, But Intervention Fears Stay Contained

Japan PMI Growth Accelerates as Manufacturing Boom Extends

Australia Composite PMI Climbs Toward Growth, But Demand Remains Weak

Fed’s Goolsbee: Key Question Is Whether Inflation Stays at 3%-4%

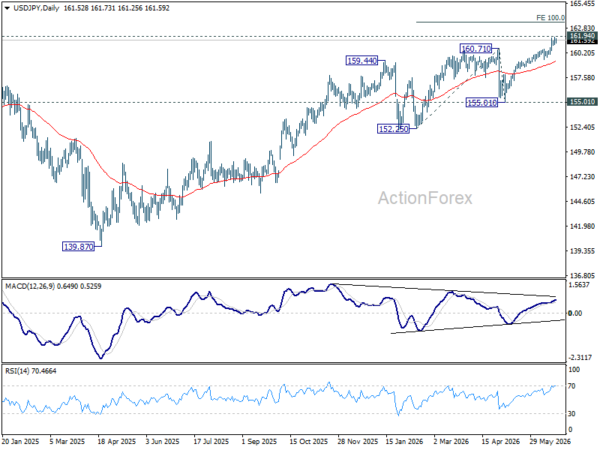

USD/JPY Daily Outlook

Intraday bias in USD/JPY stays mildly on the upside at this point. Decisive break of 161.94 high will resume the larger up trend to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next. On the downside, break of 160.58 minor support will turn bias back to the downside, and bring deeper pullback to 55 D EMA (now at 159.30).

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. This will remain the favored case as long as 55 W EMA (now at 155.17) holds.