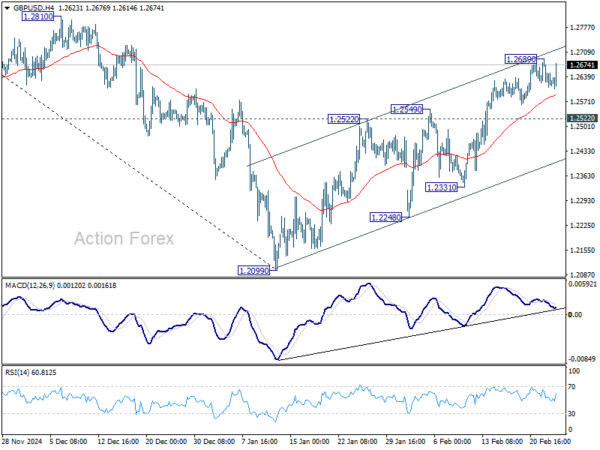

Trading is rather subdued in the forex markets today, with most major pairs and crosses stuck within yesterday’s range. Loonie failed to react to significantly stronger-than-expected retail sales data. Euro dipped earlier following weak PMI reports, but selling pressure quickly fizzled out. Yen saw some volatility during the Asian session, initially weakening alongside Japanese bond yields after BoJ Governor Kazuo Ueda’s comments, but selling was short-lived.

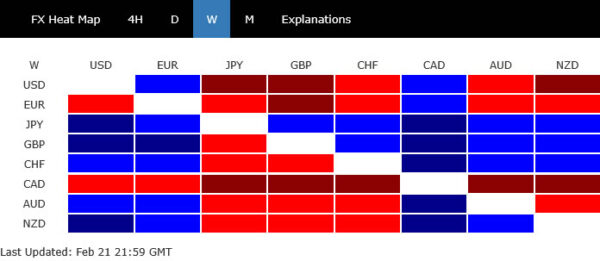

For the week so far, Yen remains the strongest performer, although it could now pause for consolidation after its recent rally. Sterling pound ranks second, followed by Aussie. On the weaker side, Euro has slipped to the bottom, just below Loonie and Dollar. However, the gap between the three remains tight, leaving room for shifts before the weekly close. Meanwhile, Swiss Franc and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.02%. DAX is up 0.29%. CAC is up 0.52%. UK 10-year yield is up 0.0044 at 4.619. Germany 10-year yield is down -0.0478 at 2.492.Earlier in Asia, Nikkei rose 0.26%. Hong Kong HSI rose 3.99%. China Shanghai SSE rose 0.85%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield fell -0.0229 to 1.428.

Canada’s retail sales surge in 2.5% mom Dec, but Jan set for pullback

Canada’s retail sales jumped 2.5% mom to CAD 69.6B in December, far surpassing market expectations of 1.6% mom. Sales increased across all nine subsectors, with the strongest contributions from food and beverage retailers and motor vehicle and parts dealers.

In volume terms, retail sales also rose 2.5% mom, indicating that the increase was not solely due to price effects.

For Q4, retail sales climbed 2.4% qoq, marking the second consecutive quarterly gain. Adjusted for inflation, sales volumes rose 1.8% qoq.

However, momentum may have slowed at the start of 2025. Advance estimate for January suggests retail sales declined by -0.4% mom.

Eurozone PMI manufacturing rises to 47.3, but services falls to 50.7

Eurozone Manufacturing PMI improved from 46.6 to 47.3 in February, a nine-month high. However, Services PMI declined to 50.7 from 51.3, dragging Composite PMI flat at 50.2, indicating near stagnant overall growth.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted that services sector price pressures remain elevated, creating complications for the ECB ahead of its next meeting. Persistent wage growth and rising input costs in manufacturing, driven by energy prices, add to inflationary risks.

Regionally, France’s services sector led the slowdown, with business activity deteriorating at an accelerated pace since September. In contrast, Germany maintained modest growth, supported by expectations of greater political stability ahead of its federal elections.

UK PMI composite dips to 50.5, stagflation dilemma for BoE

UK’s PMI Manufacturing dropped from 48.3 to 46.4 in February, a 14-month low. PMI Services edged up slightly to 51.1 from 50.8, while Composite PMI dipped to 50.5 from 50.6, indicating minimal overall growth.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted that business activity remained “largely stalled” for the fourth straight month, with job losses accelerating amid declining sales and rising costs. He cautioned that the combination of stagnant growth and mounting price pressures is creating a “stagflationary environment,” presenting a “growing dilemma” for BoE.

A primary driver of inflationary pressure is the increase in firms raising prices to offset rising staff costs tied to the National Insurance hike and minimum wage increase announced in the autumn Budget. However, these same fiscal measures have also exacerbated job cuts, with employment falling at its fastest pace since the global financial crisis, excluding the pandemic period.

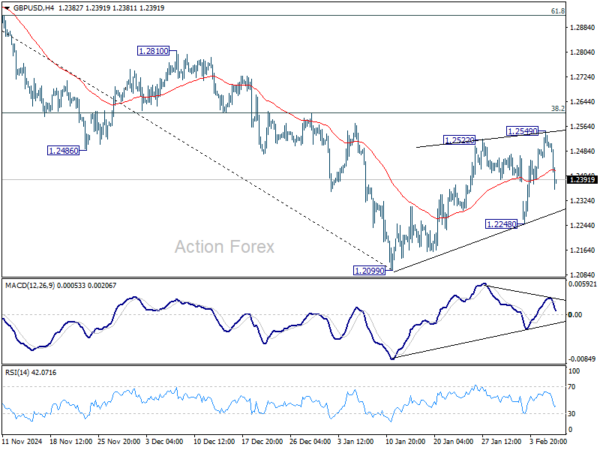

UK retail sales rebound sharply by 1.7% mom in Jan

UK retail sales volumes surged 1.7% mom in January, far exceeding market expectations of 0.3% m/m, marking a strong recovery from December’s -0.6% mom decline.

This sharp rebound pushed monthly sales index levels to their highest since August 2024.

However, the broader trend remains mixed. Over the three months to January 2025, sales volumes declined by -0.6% compared to the previous three months. On a year-over-year basis, sales volumes rose 1.4%, showing some improvement in spending patterns compared to early 2024.

Despite the monthly rebound, UK retail sales volumes remain -1.3% below pre-pandemic levels from February 2020.

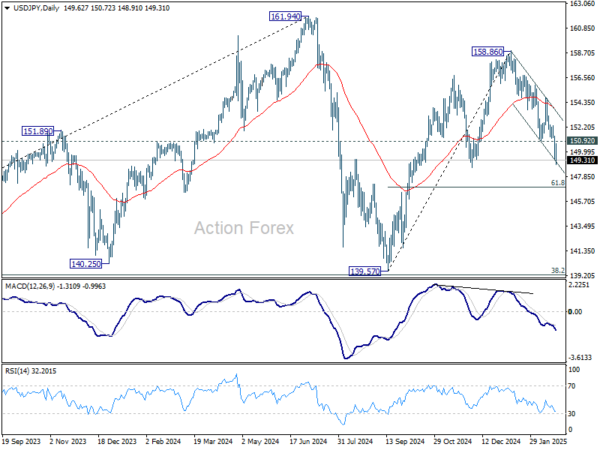

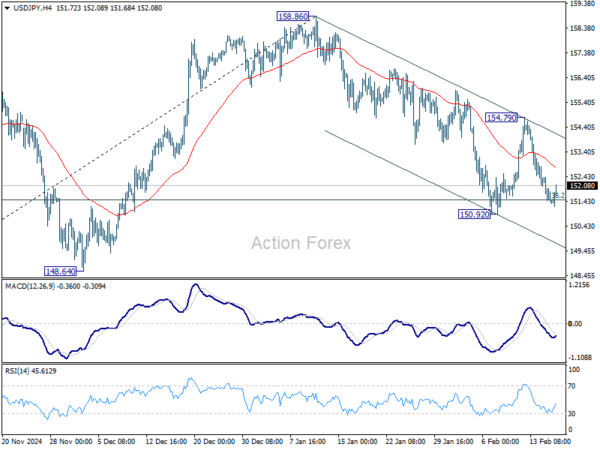

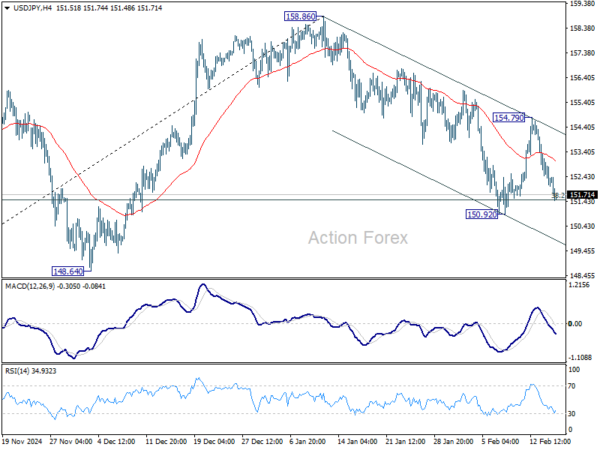

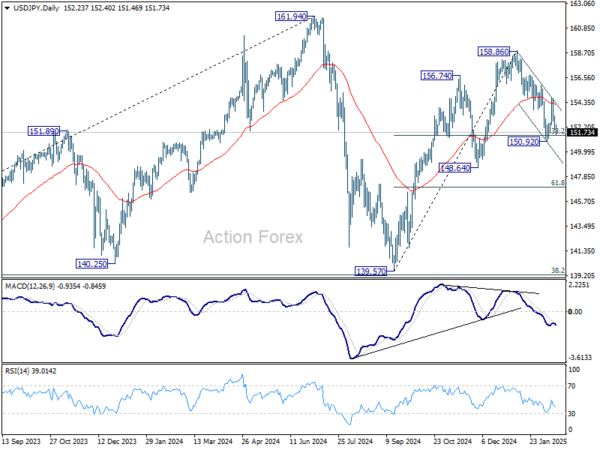

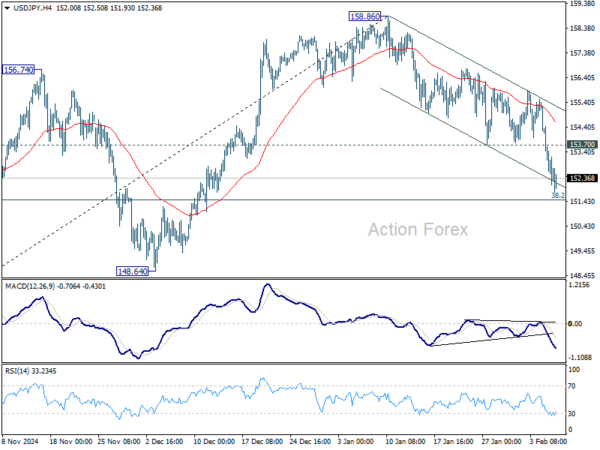

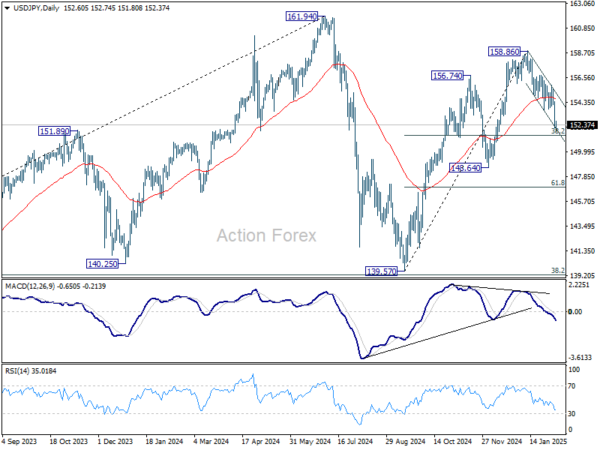

BoJ’s Ueda pledges action against sharp JGB yield rise, Yen tumbles

Yen pulled back sharply from its recent rally, along with steep fall in 10-year JGB yield from its 15-year high. The move came after BoJ Governor Kazuo Ueda reminded markets of the central bank’s commitment to curbing excessive yield volatility.

In parliamentary comments, Ueda stated, “We expect long-term interest rates to fluctuate to some extent.”

However, he cautioned that “when markets make abnormal moves and lead to a sharp rise in yields, we are ready to respond nimbly to stabilize markets.”

The pledge to increase bond purchases, if necessary, knocked the 10-year JGB yield off its 15-year high

Ueda declined to specify when BoJ might conduct emergency bond market operations, stating only that the central bank would closely monitor the market for signs of destabilization.

Japan’s core CPI jumps to 3.2% in Jan, above expectations

Japan’s inflation accelerated in January, with core CPI (ex-food) rising from 3.0% yoy to 3.2% yoy, surpassing expectations of 3.1% yoy and marking the fastest pace in 19 months, driven by higher rice and energy costs.

This was also the third consecutive month of acceleration, with core CPI rebounding sharply from 2.3% yoy in October. Inflation has now remained at or above BoJ’s 2% target since April 2022.

Core-core CPI (ex-food and energy) climbed to 2.5% yoy, up from 2.4% yoy, signaling broader price pressures beyond energy and food. Food prices, excluding perishables, surged 5.1% yoy, up from 4.4% yoy, driven by a 70.9% yoy spike in rice prices, the largest increase since data collection began in 1971. This sharp rise was attributed to supply shortages and higher production and transportation costs.

Energy prices also saw a notable increase of 10.8% yoy, up from 10.1% yoy in December, as gasoline costs rose following government subsidy reductions. Meanwhile, services inflation slowed slightly to 1.4% yoy from 1.6% yoy.

Headline CPI surged from 3.6% yoy to 4.0% yoy, a two-year high.

Japan’s PMI improves, but business confidence hits lowest since 2021

Japan’s PMI data for February showed slight improvements, with PMI Manufacturing rising from 48.7 to 48.9. Meanwhile, PMI Services edged up from 53.0 to 53.1. Composite PMI increased from 51.1 to 51.6, the highest in five months.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the “modest improvement” was driven by sustained growth in services, with firms crediting business expansion plans and improved sales.

However, optimism about future business activity weakened, with confidence dropping to its lowest level since January 2021. Companies cited labor shortages, persistent inflation, and weak domestic economic conditions as major concerns.

Employment growth slowed to its weakest pace in over a year, reflecting businesses’ caution about hiring amid economic uncertainty. Additionally, input price inflation remained elevated, similar to January’s historically high levels.

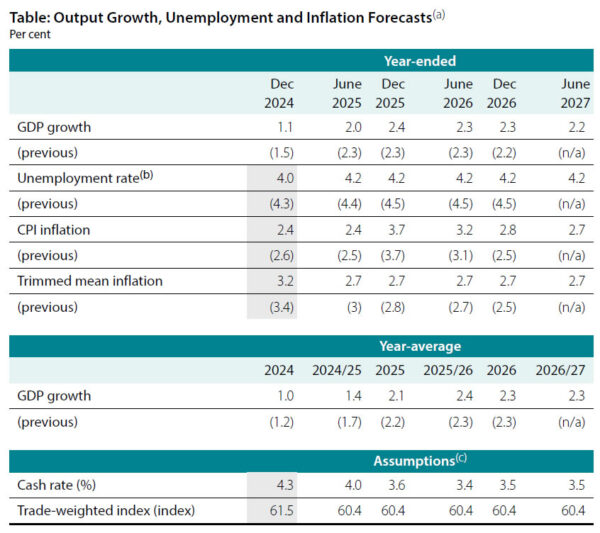

RBA’s Bullock: More rate cuts possible, but patience needed

At a parliamentary committee hearing today, RBA Governor Michele Bullock explained that this week’s 25bps rate cut was based on better-than-expected inflation data, weaker private demand, and wage growth aligning with forecasts.

Also, she acknowledged that the board is mindful of timing, stating, “What’s also playing on the board’s mind is that the board also doesn’t want to be late, and arguably we were late raising interest rates on the way up.”

While further easing remains on the table, Bullock emphasized the need for caution. “We are not pre-committed. We’re going to be data-driven on this and I think people just have to be patient,” she added.

Deputy Governor Andrew Hauser echoed this sentiment, reinforcing the RBA’s wait-and-see approach. He remarked, “If we’re wrong and inflation moves more quickly downwards, you could celebrate that fact and policy will need to respond, but we’d rather wait and see than assume that’s what’s going to happen.”

Australia’s PMI composite hits 6-month high, but business confidence dips

Australia’s PMI data for February showed continued expansion in private sector activity, with Manufacturing PMI rising to from 50.2 to 50.6, its highest level in 27 months. Meanwhile, Services PMI edged up from 51.2 to 51.4, and Composite PMI ticked up from 51.1 to 51.2, both reaching six-month highs.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the latest figures indicate a “modest” but steady improvement in economic conditions, while growth was broad-based.

However, business sentiment weakened to its lowest level since October 2024. This caution also affected pricing strategies, with businesses reluctant to fully pass on cost increases, leading to a slowdown in selling price inflation.

RBNZ’s Conway: 50bps cut the clear choice, signs of economic turnaround emerging

RBNZ Chief Economist Paul Conway revealed in a Reuters interview that the central bank considered both 25bps and 75bps rate cuts ahead of this week’s policy decision. But the bank ultimately concluded that a 50bps reduction “was the way to go” given the state of the economy and inflation.

Conway pointed to recent data in manufacturing and services, indicating that some businesses may already be “starting to feel a bit of a turnaround.” However, he acknowledged that companies remain cautious.

Regarding the labor market, Conway noted that employment trends typically lag economic activity. He added that”businesses need to have confidence that growth is returning and that growth will be sustained into the future before they start to think about employing someone.”

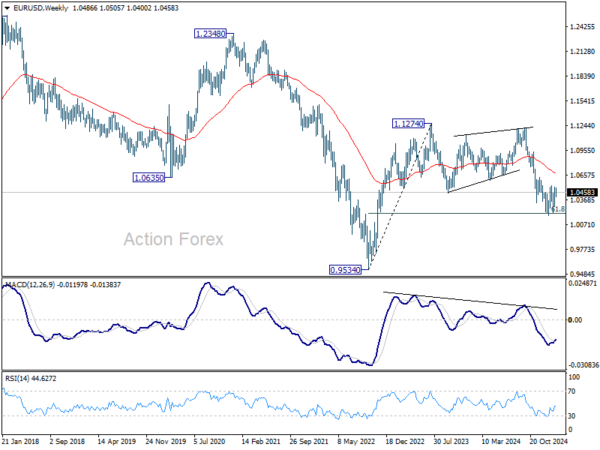

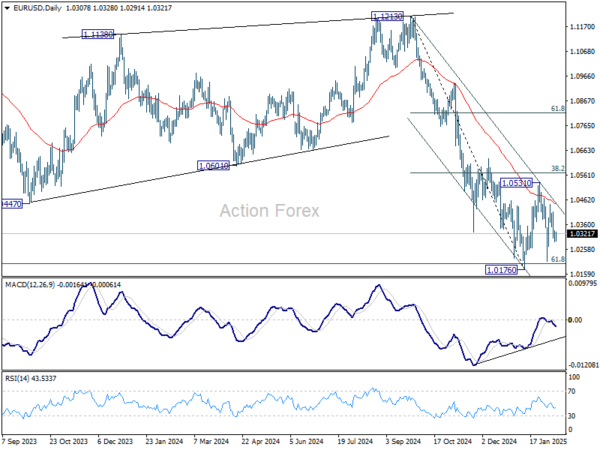

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0446; (P) 1.0475; (R1) 1.0532; More…

Outlook in EUR/USD remains unchanged despite today’s mild dip. Consolidation from 1.0176 is still extending and intraday bias remains neutral. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Economic Indicators Update

| GMT |

CCY |

EVENTS |

ACT |

F/C |

PP |

REV |

| 21:45 |

NZD |

Trade Balance (NZD) Jan |

-486M |

225M |

219M |

94M |

| 22:00 |

AUD |

Manufacturing PMI Feb P |

50.6 |

|

50.2 |

|

| 22:00 |

AUD |

Services PMI Feb P |

51.4 |

|

51.2 |

|

| 23:50 |

JPY |

CPI Y/Y Jan |

4.00% |

|

3.60% |

|

| 23:50 |

JPY |

CPI Core Y/Y Jan |

3.20% |

3.10% |

3.00% |

|

| 23:50 |

JPY |

CPI Core-Core Y/Y Jan |

2.50% |

|

2.40% |

|

| 00:01 |

GBP |

GfK Consumer Confidence Feb |

-20 |

-22 |

-22 |

|

| 00:30 |

JPY |

Manufacturing PMI Feb P |

48.9 |

49 |

48.7 |

|

| 00:30 |

JPY |

Services PMI Feb P |

53.1 |

|

53 |

|

| 07:00 |

GBP |

Retail Sales M/M Jan |

1.70% |

0.30% |

-0.30% |

-0.60% |

| 07:00 |

GBP |

Public Sector Net Borrowing (GBP) Jan |

-15.4B |

-20.5B |

17.8B |

18.1B |

| 08:15 |

EUR |

France Manufacturing PMI Feb P |

45.5 |

45.3 |

45 |

|

| 08:15 |

EUR |

France Services PMI Feb P |

44.5 |

49 |

48.2 |

|

| 08:30 |

EUR |

Germany Manufacturing PMI Feb P |

46.1 |

45.6 |

45 |

|

| 08:30 |

EUR |

Germany Services PMI Feb P |

52.2 |

52.6 |

52.5 |

|

| 09:00 |

EUR |

Eurozone Manufacturing PMI Feb P |

47.3 |

47.1 |

46.6 |

|

| 09:00 |

EUR |

Eurozone Services PMI Feb P |

50.7 |

51.5 |

51.3 |

|

| 09:30 |

GBP |

Manufacturing PMI Feb P |

46.4 |

48.5 |

48.3 |

|

| 09:30 |

GBP |

Services PMI Feb P |

51.1 |

51 |

50.8 |

|

| 13:30 |

CAD |

Retail Sales M/M Dec |

2.50% |

1.60% |

0% |

0.20% |

| 13:30 |

CAD |

Retail Sales ex Autos M/M Dec |

2.70% |

0.40% |

-0.70% |

|

| 14:45 |

USD |

Manufacturing PMI Feb P |

|

51.3 |

51.2 |

|

| 14:45 |

USD |

Services PMI Feb P |

|

53 |

52.9 |

|

| 15:00 |

USD |

Existing Home Sales M/M Jan |

|

4.17M |

4.24M |

|

| 15:00 |

USD |

Michigan Consumer Sentiment Index Jan F |

|

67.8 |

67.8 |

|