After a burst of volatility earlier in the session, currency markets are taking a breather as traders reassess the evolving US tariff situation. Comments from White House National Economic Council Director Kevin Hassett helped cool tensions when he clarified that, “This is not a trade war, this is a drug war,” directing the focus toward fentanyl imports rather than a sweeping escalation of protectionist policies. His remarks have provided a temporary sense of relief, as markets take a step back to evaluate whether tariff measures could be adjusted or reversed if progress is made on fentanyl control.

President Donald Trump’s updates on discussions with Canadian Prime Minister Justin Trudeau have also offered a glimmer of hope that a negotiated outcome could avert more severe tariff measures. Market sentiment hangs on the possibility that resolving fentanyl-related disputes could defuse tensions, but the risks for a breakdown in talks still looms. A failure to find common ground would likely re-energize the recent selloff and send safe-haven flows back into assets like the Japanese Yen, Swiss Franc and Dollar.

Speaking of currencies, the Yen stands out as the day’s strongest performer so far, benefiting from sliding US Treasury yields and ongoing risk aversion. Dollar remains firm in second place. Sterling is surprising the third strongest, drawing relative support since it appears less threatened by new US tariffs than the European Union. Meanwhile, Swiss Franc has also gained ground on renewed risk-off sentiment. Kiwi, Euro, and Loonie lag behind while Aussie remains under pressure, despite taking a brief pause from its recent downward spiral.

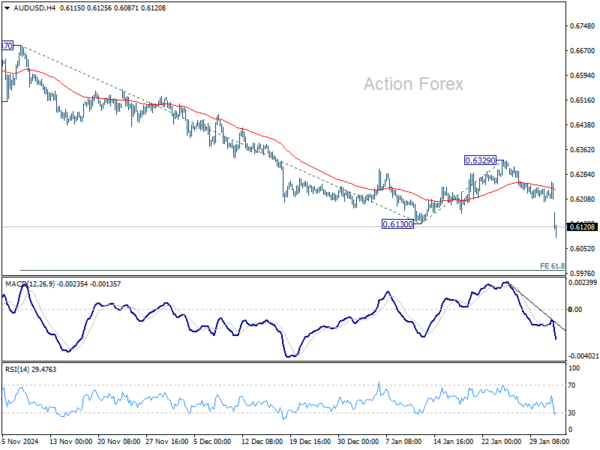

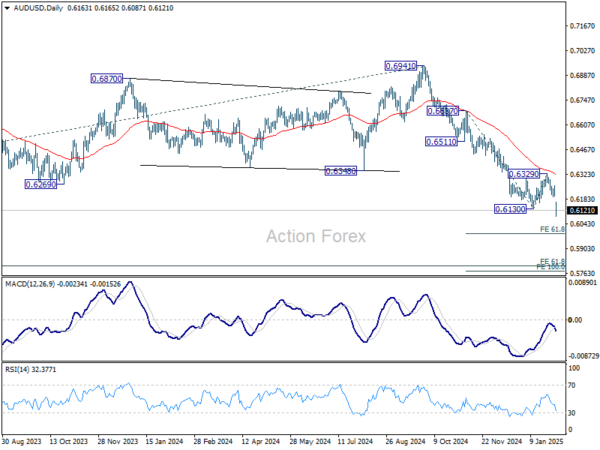

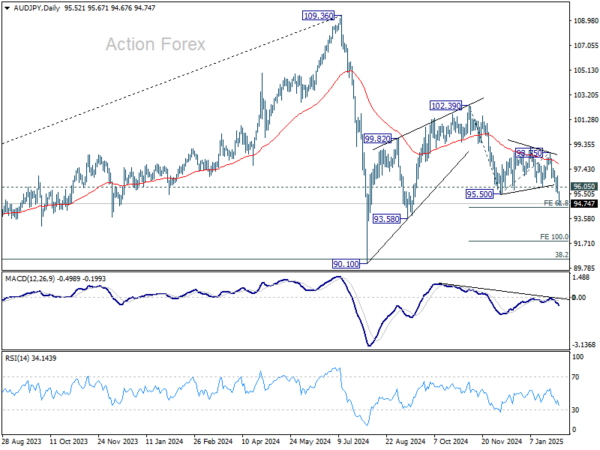

Technically, AUD/JPY’s fall from 102.39 resumed today by powering through 95.50 support. Immediate focus is now on 61.8% projection of 102.39 to 95.50 from 98.75 at 94.49. Decisive break there could prompt downside acceleration to 100% projection at 91.86. For now, risk will stay on the downside as long as 96.05 support turned resistance holds, in case of recovery.

In Europe, at the time of writing, FTSE is down -1.57%. DAX is down -2.00%. CAC is down -1.76%. UK 10-year yield is down -0.0996 at 4.440. Germany 10-year yield is down -0.091 at 2.370. Earlier in Asia, Nikkei fell -2.66%. Hong Kong HSI fell -0.04%. China was on holiday. Singapore Strait Times fell -0.76%. Japan 10-year JGB yield rose 0.0075 to 1.249.

US ISM manufacturing rises to 50.9, ending 26-month contraction

The US manufacturing sector returned to expansion in January, with ISM Manufacturing PMI rising to 50.9 from 49.2, breaking a 26-month streak of contraction, above expectation of 49.3.

The improvement was broad-based, signaling stronger demand and increased production capacity. Notably, new orders climbed to 55.1 from 52.1, reflecting growing demand, while production rose to 52.5 from 49.9, indicating that manufacturers are ramping up output in response.

The employment index also showed a meaningful recovery, rebounding to 50.3 from 45.4, suggesting that firms are hiring again after months of labor market weakness. Meanwhile, input costs rose, with the prices index increasing to 54.9 from 52.5, signaling that inflationary pressures may be creeping back into the supply chain.

Timothy Fiore, Chair of the ISM Manufacturing Business Survey Committee, highlighted that the January PMI reading aligns with a projected 2.4% annualized GDP growth rate.

Eurozone CPI rises to 2.5% in Jan, core unchanged at 2.7%

Eurozone CPI rose from 2.4% yoy to 2.5% yoy in January, above expectation of 2.4% yoy. CPI core (ex-energy, food, alcohol & tobacco) was unchanged at 2.7% yoy, above expectation of 2.6% yoy.

Looking at the main components, services is expected to have the highest annual rate in January (3.9%, compared with 4.0% in December), followed by food, alcohol & tobacco (2.3%, compared with 2.6% in December), energy (1.8%, compared with 0.1% in December) and non-energy industrial goods (0.5%, stable compared with December).

Eurozone PMI manufacturing finalized at 46.6, still too early to talk about greenshoots

Eurozone PMI Manufacturing was finalized at 46.6, up from December’s 45.1, marking an eight-month high. While still in contraction, the data suggests a slowdown in the sector’s decline. Germany’s PMI rose to 45.0, while France rose to 45.0. Austria (45.7) and Italy (46.3) also saw multi-month highs. Greece (52.8) and Spain (50.9) remained in expansion.

According to Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, despite the improvement, manufacturing remains under pressure. It is “too early” to signal a full recovery. Rising input costs, driven by nearly 7% increase in oil prices, pose risks for firms already facing weak demand. ECB’s easing path could also be complicated if inflationary pressures persist.

The US is expected to impose tariffs on European exports. However, business confidence has improved, with future output expectations rising four points above the long-term average, partly driven by optimism surrounding upcoming elections in Germany and possibly France.

While Germany and France remain the weakest performers, the pace of contraction has slowed across multiple sectors. De la Rubia noted that over 90% of Eurozone exports go to markets outside the US, limiting the immediate impact of potential tariffs.

UK PMI manufacturing finalized at 48.3, outlook remains weak

UK manufacturing sector remained in contraction at the start of 2025, with January’s final PMI rising slightly to 48.3 from December’s 11-month low of 47.0. Despite the modest improvement, four of the five key components—output, new orders, employment, and stocks of purchases—declined. The only positive indicator was longer average vendor lead times, which typically reflect supply chain constraints rather than stronger demand.

Rob Dobson, Director at S&P Global Market Intelligence noted that Weak domestic and international demand remains a key drag on the sector, with no clear signs of recovery in sight. Rising cost pressures are also adding to the strain, with input price inflation reaching a two-year high.

The effects of last year’s Budget changes, particularly increases in the minimum wage and employer National Insurance contributions, are expected to feed further into rising costs. These factors could keep pressure on profit margins and limit any near-term rebound in manufacturing activity. Business confidence remains low, hovering near December’s two-year low, reflecting ongoing uncertainty in both economic conditions and policy direction.

BoJ opinions signal more rate hikes as inflation risks tilt higher

BoJ’s Summary of Opinions from the January 23-24 meeting indicates a growing shift toward policy normalization, as multiple board members highlighted mounting inflationary pressures.

Rising import costs driven by the weak yen have led more businesses to raise prices, prompting concerns that inflation could overshoot expectations.

One member noted that with economic activity and prices remaining stable, “risks to prices have become more skewed to the upside,” emphasizing that rate hikes should be “timely and gradual.”

Some policymakers warned that continued Yen depreciation and excessive risk-taking could lead to an overheating of financial activities. To counter this, one board member argued for additional rate hikes to stabilize the currency and prevent further distortions in market expectations regarding BoJ policy.

At the January meeting, the BoJ raised its short-term policy rate from 0.25% to 0.50%, marking another step away from ultra-loose monetary policy. The central bank also revised its price forecasts higher, reinforcing its confidence that rising wages will sustain inflation near the 2% target.

Japan’s PMI manufacturing finalized at 48.7, deepest contraction in 10 Months

Japan’s PMI Manufacturing was finalized at 48.7 in January, down from December’s 49.6. This marks the sharpest decline in output since March 2024, as firms faced a steeper drop in new orders. Weak demand conditions forced manufacturers to scale back production, reflecting ongoing headwinds for the sector.

According to S&P Global, businesses reacted to falling demand by cutting both inventories and raw material holdings, while also reducing input purchases at the fastest pace in nearly a year. Employment growth also slowed, highlighting a cautious approach to hiring amid economic uncertainty.

Despite the downturn, manufacturers maintained a positive outlook for future output, though confidence fell to its lowest level since December 2022. While firms expect a recovery in demand, concerns persist over when such an improvement will materialize. The slowdown in input price inflation to a nine-month low provides some relief, but overall, sentiment remains fragile.

Australia’s retail sales dip -0.1% mom in Dec, less than expected

Australia’s retail sales turnover edged down by -0.1% mom in December, a smaller decline than the expected -0.7% mom. While the contraction marks a pullback from the strong growth seen in previous months—0.7% mom in November and 0.5% in October mom—it suggests that consumer spending remains relatively resilient.

According to Robert Ewing, head of business statistics at the Australian Bureau of Statistics, retail activity was supported by extended promotional events, helping to smooth spending patterns over the quarter. He noted that Cyber Monday, which fell in early December, boosted demand for discretionary items, particularly furniture, homewares, electronics, and electrical goods.

China’s Caixin PMI manufacturing slips to 50.1, growth momentum weakens

China’s Caixin Manufacturing PMI edged down to 50.1 in January from 50.5 in December.

According to Caixin Insight Group, manufacturers saw improved logistics and a slight pickup in supply and demand. However, employment levels deteriorated notably, and new export orders remained weak, reflecting sluggish global demand.

External risks also remain a key concern, with rising geopolitical uncertainty adding pressure to China’s export environment. Disruptions in global trade policies could further dampen overseas demand, making it difficult for manufacturers to sustain current production levels.

Domestically, consumer spending remains sluggish, highlighting the need for policy measures aimed at boosting disposable income and restoring confidence.

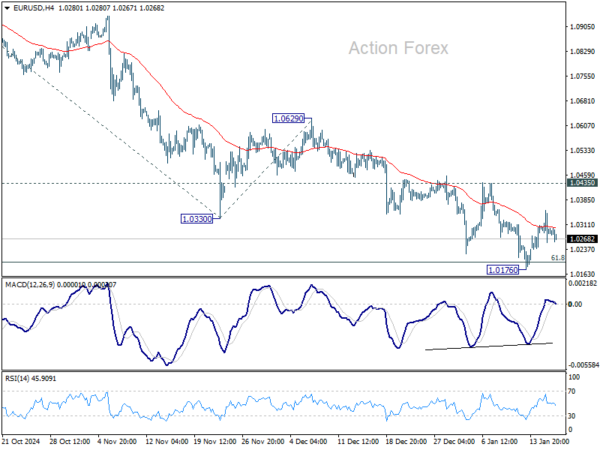

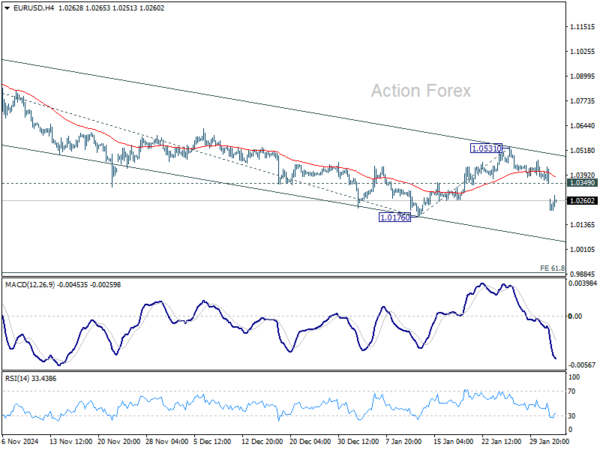

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0328; (P) 1.0381; (R1) 1.0412; More…

Intraday bias in EUR/USD remains on the downside for the moment. Decisive break of 1.0176 will resume whole fall from 1.1213. Next target will be 61.8% projection of 1.1213 to 1.0176 from 1.0531 at 0.9890. On the upside, above 1.0349 resistance will turn intraday bias neutral again first. But outlook will stay bearish as long as 1.0531 resistance holds, in case of strong recovery.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. For now, risk will stay on the downside as long as 1.0531 resistance holds, in case of rebound.