The forex market was relatively subdued during Asian session, with one clear exception: Japanese Yen continues to outperform. Fresh data from Japan showed a 2.7% yoy increase in household spending, not only marking the first rise in five months, but also the fastest pace since August 2022. Paired with this week’s solid wage growth figures, the numbers suggest real wage gains are driving consumption—a development that could reinforce BoJ’s push toward gradual policy normalization.

Additionally, IMF offered further support for Yen by endorsing a gradual rise in BoJ rates to a neutral range of 1-2% by the end of 2027. Although this view appears somewhat conservative compared to hawkish BoJ board member Naoki Tamura’s call for a 1% rate by the second half of fiscal 2025, the gap isn’t significant. If Japan’s inflation and wage growth hold up, it’s feasible that interest rates could reach the midpoint of 1.5% within a few quarters from Tamura’s target.

Attention now shifts to the US non-farm payroll report, with prospects of upside surprise. Dallas Fed President Lorie Logan raised an interesting argument that Fed may not ease policy further unless the labor market noticeably softens, even if inflation trends lower. A strong NFP reading would bolster expectations for an extended Fed pause. However, it may not be enough to spark an upside breakout in the Dollar from recent ranges, given ongoing uncertainties tied to US trade policies.

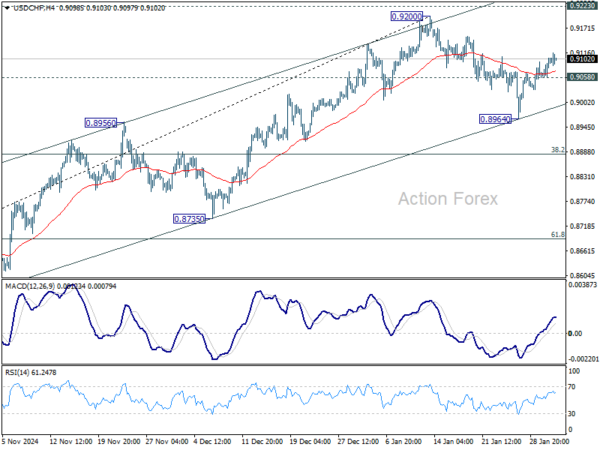

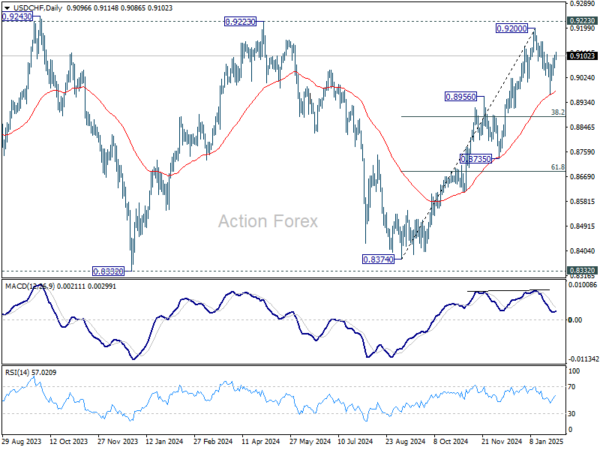

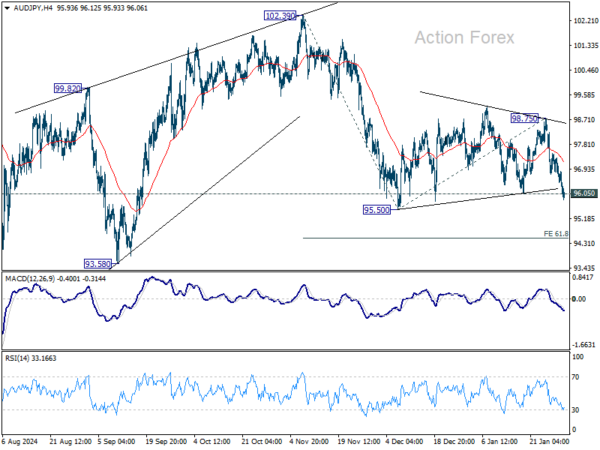

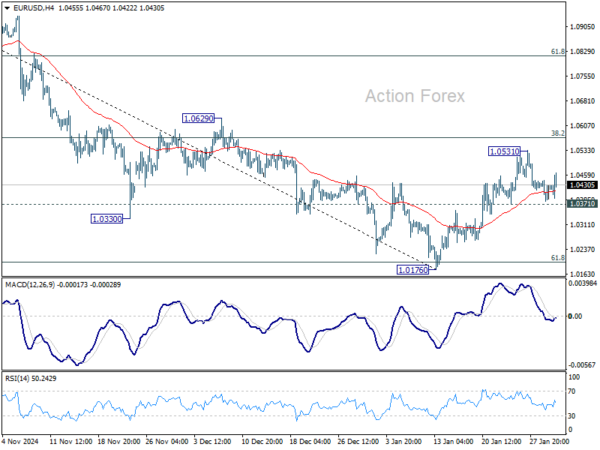

Overall for the week so far, Dollar is currently the worst performer, followed by Euro, and then Sterling. Yen is the best, followed by Loonie, and then Aussie. Swiss Franc and Kiwi are positioning in the middle.

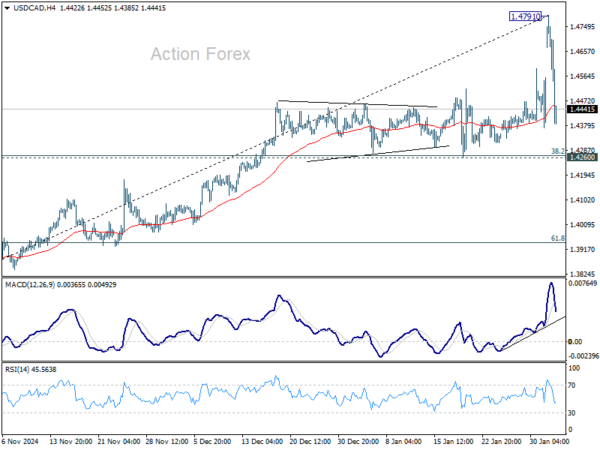

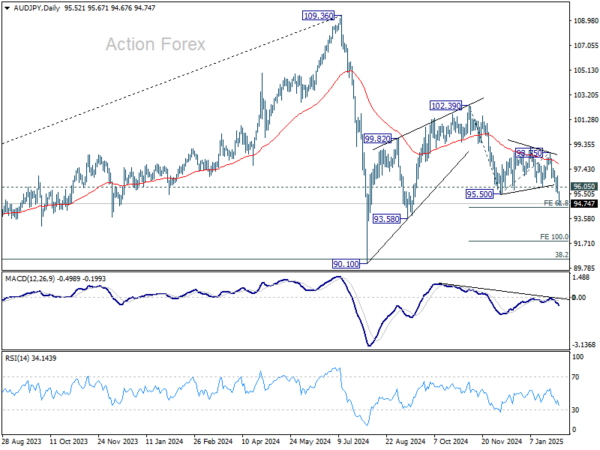

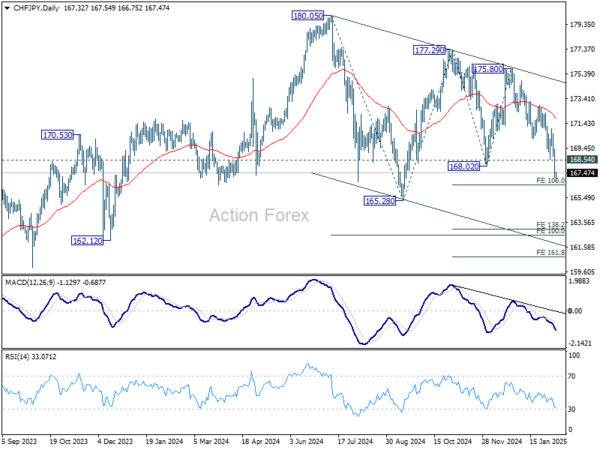

Technically, CHF/JPY’s break of 168.02 support confirms resumption of fall from 177.29. This decline is seen as the third leg of the corrective pattern from 180.05 high. Further fall is expected as long as 168.54 support turned resistance holds. Firm break of 100% projection of 177.29 to 168.02 from 175.80 at 166.53 should bring deeper fall through 165.28 support to 138.2% projection at 162.98.

In Asia, at the time of writing, Nikkei is down -0.72%. Hong Kong HSI is up 1.05%. China Shanghai SSE is up 1.02%. Singapore Strait Times is up 0.83%. Japan 10-year JGB yield is up 0.0339 at 1.301. Overnght, DOW fell -0.28%. S&P 500 rose 0.36%. NASDAQ rose 0.51%. 10-year yeld rose 0.018 to 4.440.

NFP may beat expectations, but unlikely to trigger Dollar range breakout

Today’s US Non-Farm Payroll report is the focal point for market participants, with consensus estimates pointing to 169k new jobs in January and an unemployment rate holding steady at 4.1%. Average hourly earnings growth is expected at 0.3% month-over-month, maintaining the robust wage gains of recent months.

There are indications the data could surprise to the upside. Latest ISM surveys showed employment components improving, with manufacturing’s gauge jumping from 45.4 back into expansion at 50.3, and services employment rising to 52.3 from 51.3. ADP private payrolls number also showed a solid 183k increase, little changed from December’s 176k. Meanwhile, initial jobless claims remain near historical lows, with the four-week moving average inching up only slightly from 213k to 217k.

If today’s jobs report beats expectations, the case for Fed to maintain its pause on easing for longer would strengthen. However, persistent uncertainties—especially US trade policies—may limit the Dollar’s ability to rally significantly. While a strong labor market may keep rate cuts at bay, investors will weigh other geopolitical and economic factors before pushing the greenback through key near term resistance levels.

Technically, Dollar Index is currently extending the consolidation pattern from 110.17 short term top. In case of deeper pull back, downside should be contained by 38.2% retracement of 110.15 to 110.17 at 106.34 to bring rebound. On the upside, firm break of 110.17 is needed to confirm resumption of recent up trend. Otherwise, outlook would remains neutral for more sideway trading.

Fed’s Logan sees rates on hold “for quite some time” even if inflation drops

Dallas Fed President Lorie Logan suggested at a BIS conference overnight that interest rates may remain on hold for “quite some time,” even if inflation continues to move closer to the 2% target. She emphasized that a decline in inflation alone would not be a sufficient trigger for policy easing, as long as labor market conditions remain strong.

She argued that such a scenario would “strongly suggest that” interest rate is already pretty close to neutral, “without much near-term room for further cuts”.

Instead, Logan highlighted that signs of a weakening labor market or a slowdown in demand would be more relevant factors in determining when easing should begin.

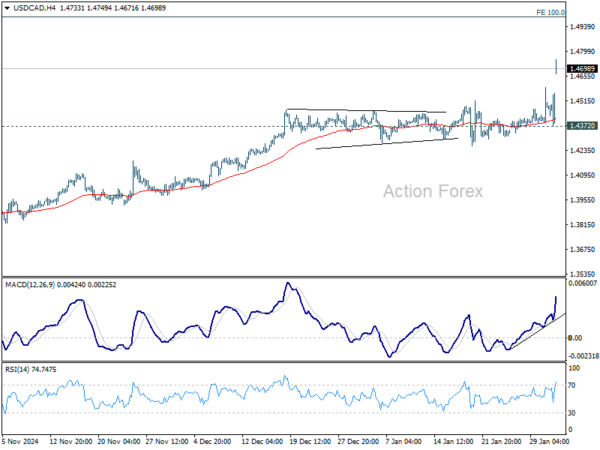

BoC’s Macklem warns tariff threats already weighing on confidence

Speaking at a conference in Mexico City, BoC Governor Tiff Macklem raised concerns over the economic uncertainty stemming from U.S. President Donald Trump’s tariff threats. He noted that “threats of new tariffs are already affecting business and household confidence, particularly in Canada and Mexico.”

“The longer this uncertainty persists, the more it will weigh on economic activity in our countries,” he warned.

Macklem stressed that central banks face a challenging task in managing the economic fallout. He explained that policymakers cannot counteract both “weaker output” and “higher inflation” simultaneously.

The challenge will be to assess the downward pressure on inflation from reduced economic activity while balancing it against the upward pressure from higher input costs and supply chain disruptions caused by tariffs.

IMF backs BoJ’s gradual rate hikes, sees policy rate moving toward neutral by 2027

Nada Choueiri, deputy director of IMF’s Asia-Pacific Department and mission chief for Japan, stated that IMF remains “supportive” of BoJ’s current monetary policy course. She emphasized that rate hikes should be implemented in a gradual and flexible manner to ensure that domestic demand continues to recover.

Choueiri projected that BoJ’s policy rate could rise “beyond 0.5%” by the end of this year, with a longer-term path toward the “neutral level” by the end of 2027.

IMF estimates Japan’s neutral rate to be within a band of 1% to 2%, with a midpoint of 1.5%.

Also, IMF maintains an optimistic outlook for Japan’s economy, forecasting 1.1% GDP growth in 2025, supported by increasing wages and stronger consumer spending.

Given these projections, IMF expects BoJ to continue its tightening cycle in a controlled manner.

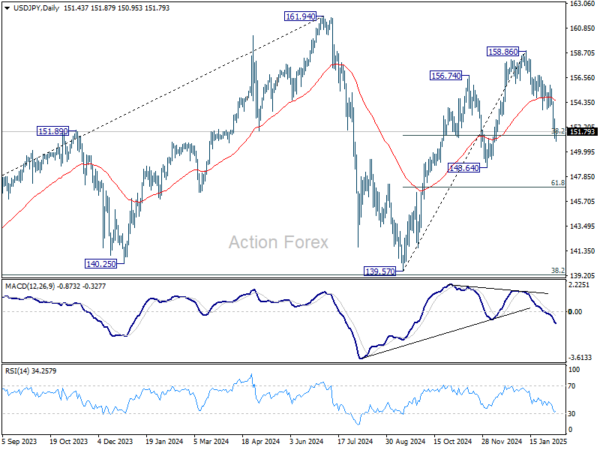

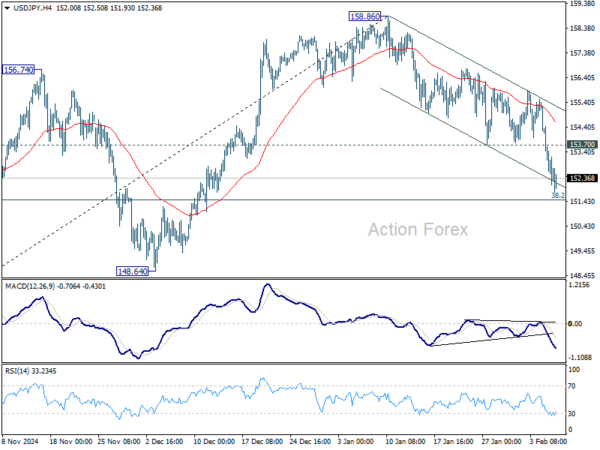

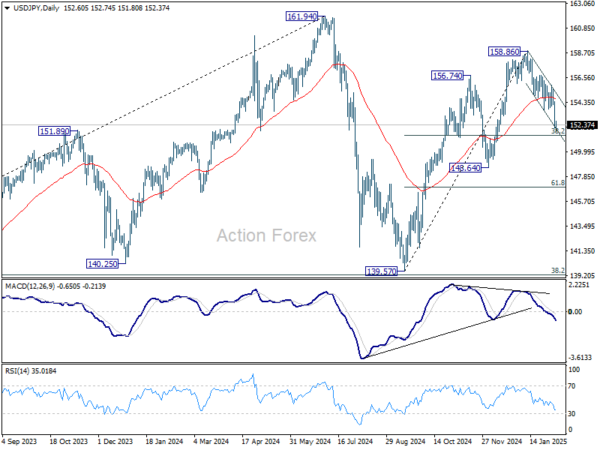

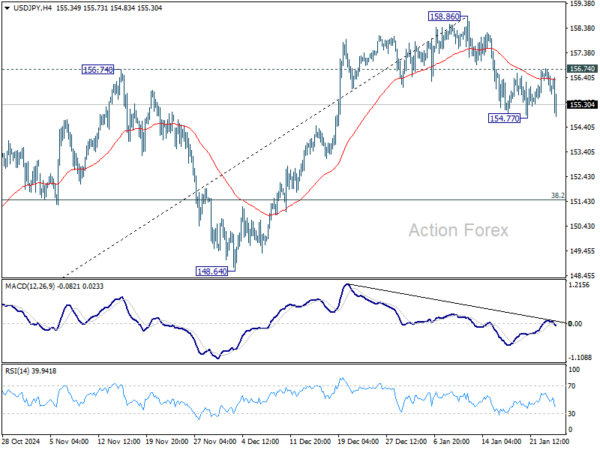

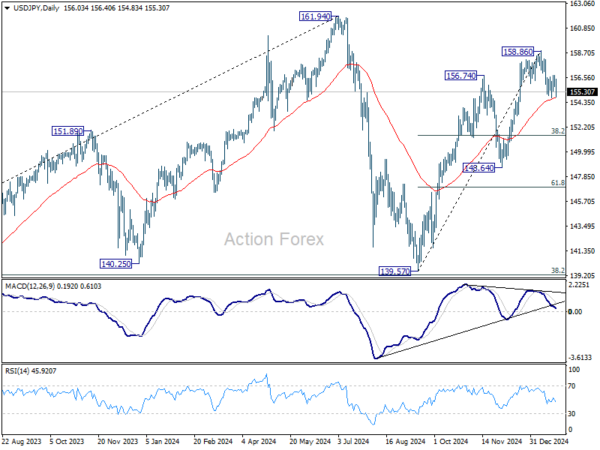

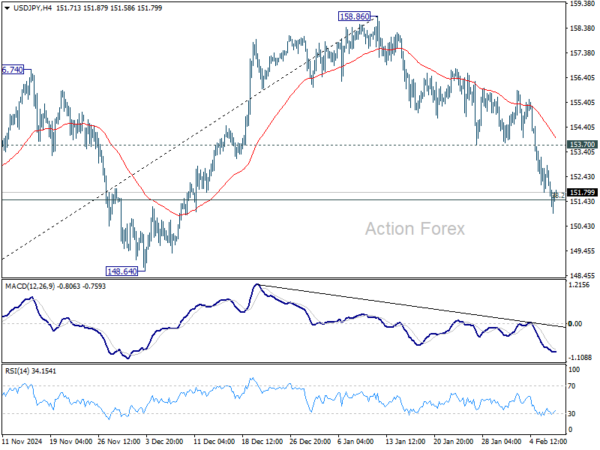

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.83; (P) 151.86; (R1) 152.48; More…

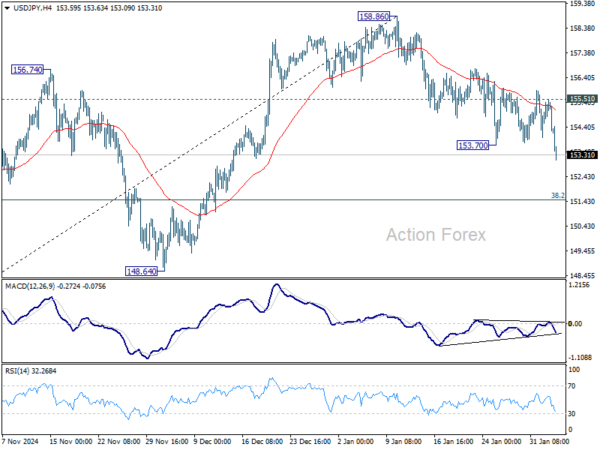

USD/JPY is now pressing 38.2% retracement of 139.57 to 158.86 at 151.49 as fall from 158.86 extended. Strong bounce from current level will keep this decline as a correction, and retain near term bullishness. Firm break of 153.70 support turned resistance will turn bias back to the upside for stronger rebound. However, sustained break of 151.49 will raise the chance of bearish reversal, and target 61.8% retracement at 146.32 next.

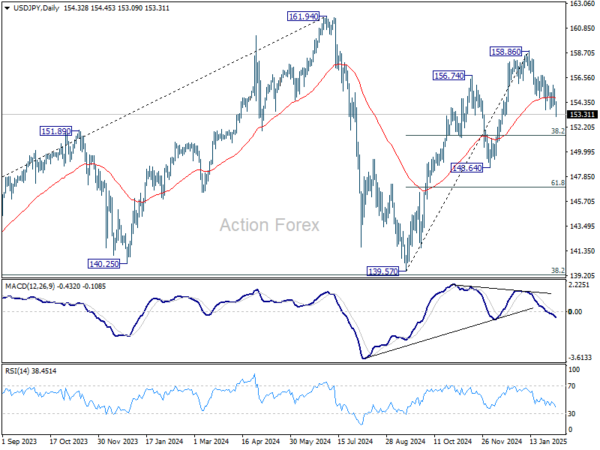

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.