Forex markets are holding steady in Asian session today, with major currency pairs and crosses all confined within yesterday’s ranges. This lack of movement comes despite a significant escalation in the US-led trade war, as newly effective 25% tariffs on all imported steel and aluminum products have prompted swift retaliation from key trading partners.

In swift response, European Commission President Ursula von der Leyen announced that the EU would implement retaliatory tariffs of equal value, totaling USD 28B, on a range of U.S. goods beyond just metals. These measures, set to take effect on April 1, will target products including textiles, home appliances, and agricultural goods. Meanwhile, Canada—the largest supplier of steel and aluminum to the U.S.—is hitting back with USD 20.7B in countermeasures, including a 25% tariff on steel products and increased taxes on US imports ranging from computers and servers to sports equipment and cast-iron products.

The UK has so far taken a more measured stance, with Prime Minister Keir Starmer stating that his government is adopting a “pragmatic approach” while keeping “all options on the table.” Australia, on the other hand, has opted against imposing retaliatory tariffs for now. Instead, Prime Minister Anthony Albanese has urged Australians to support local industries in response to Trump’s refusal to grant an exemption for Australian steel and aluminum.

On the currency front, Swiss Franc is so far the weakest performer this week, followed by Loonie and then Dollar. Euro remains the strongest but has begun to pull back in some crosses, with Sterling and Kiwi following. Yen and Aussie are positioned in the middle.

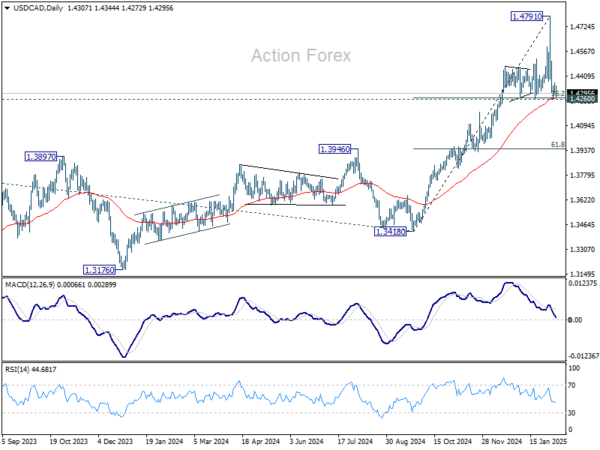

Technically, EUR/CAD could have formed a short term top at 1.5856, ahead of 200% projection of 1.4483 to 1.5058 from 1.4740 at 1.5890. Some consolidations would be seen with risk of deeper retreat to 55 4H EMA (now at 1.5470). But downside should be contained by 1.5401 support to bring rebound, and up trend resumption later.

In Asia, at the time of writing, Nikkei is up 0.09%. Hong Kong HSI is down -1.44%. China Shanghai SSE is down -0.73%. Singapore Strait Times is down -0.03%. Japan 10-year JGB yield is up 0.017 at 1.541. Overnight, DOW fell -0.20%. S&P 500 rose 0.49%. NASDAQ rose 1.22%. 10-year yield rose 0.030 to 4.318.

BoJ’s Ueda expects real wages to rise, boosting consumption

BoJ Governor Kazuo Ueda signaled optimism about Japan’s economic outlook, telling the parliament today that “import-cost-driven inflation” is expected to moderate while wages continue to “rise steadily.” This shift could lead to an improvement in real wages and consumption, a critical factor for sustaining domestic demand.

Ueda’s comments align with recent developments in Japan’s annual “shunto” wage negotiations, which have resulted in record pay hikes across major companies.

Hitachi announced a record 6.2% rise in monthly wages, fully meeting union demands. Toyota’s key auto parts supplier, Denso, also committed to historic pay hikes, while Toyota itself stated that the overall wage increase for its manufacturing staff would match last year’s levels—the highest seen since 1999.

Further clarity on the scale of wage hikes will come on March 14, when Rengo, Japan’s largest labor union federation representing 7 million workers, releases its preliminary report. Rengo had been seeking an average wage increase of 6.09%, up from last year’s 5.85%.

US stocks find temporary support, but downside risks persist

Risk sentiment showed signs of stabilization in the US overnight, with S&P 500 and NASDAQ posting gains. However, stocks are merely digesting recent steep losses rather than having a decisive turnaround.

The reaction to lower-than-expected US consumer inflation data was relatively muted. The market’s cautious interpretation of the data is justified, as the latest CPI figures do not yet capture the full effects of tariff-related price pressures. There is still a lack clarity on how inflation will evolve under the new tariff regime, particularly when reciprocal tariffs come into play on April 2. Nevertheless, for the moment at least, disinflationary momentum is leaning in the Fed’s favor.

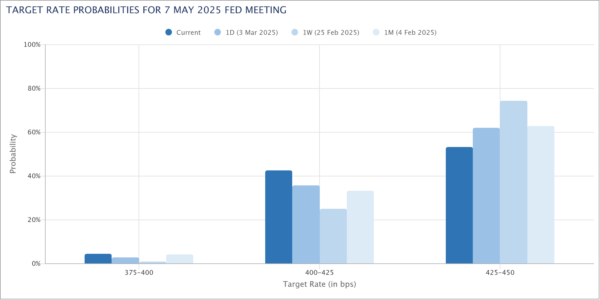

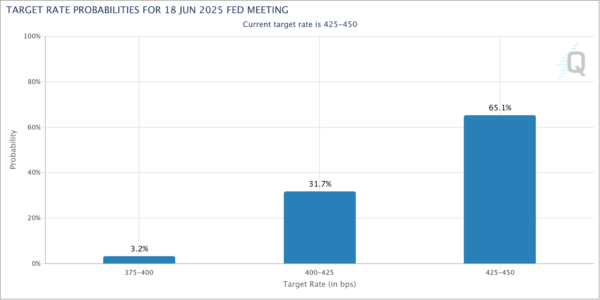

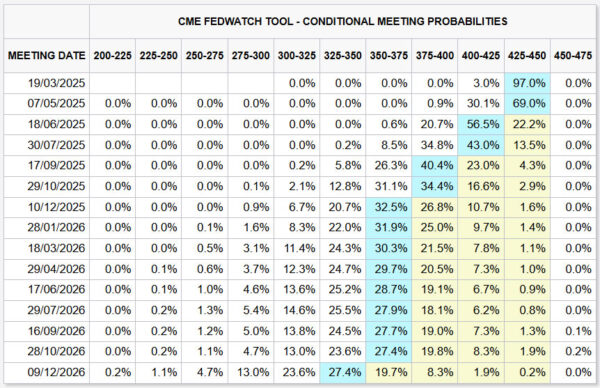

Interestingly, market pricing has shifted the expected timing of Fed’s next rate cut back from May to June. Futures now show just 31% probability of a 25bps cut in May, while the odds for a June cut have climbed to 78%.

Traders appear to believe Fed will need additional time to assess the economic impact of tariffs before making a policy move. From a timing perspective, June would align better with Fed’s next round of economic projections, allowing policymakers to incorporate more data into their decision-making.

As for NASDAQ, oversold condition as seen in D RSI could start to slow downside momentum, and some near term consolidations cannot be ruled out. But risk will stay on the downside as long as 18604.46 resistance holds. Fall from 20204.58 is seen as a correction to the whole up trend from 10088.82 (2022 low) at least. It should extend to 38.2% retracement of 10088.82 to 20204.58 at 16340.36 before bottoming.

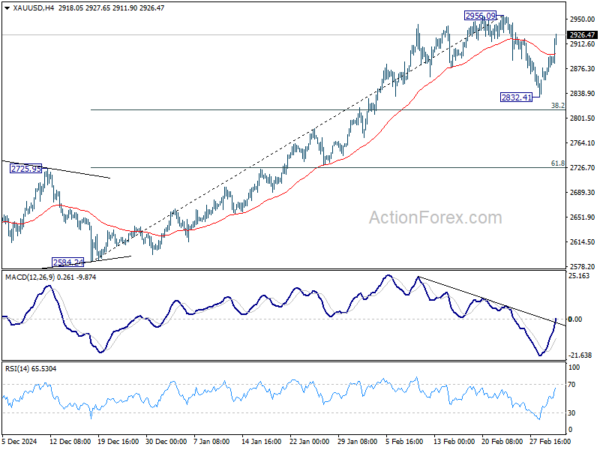

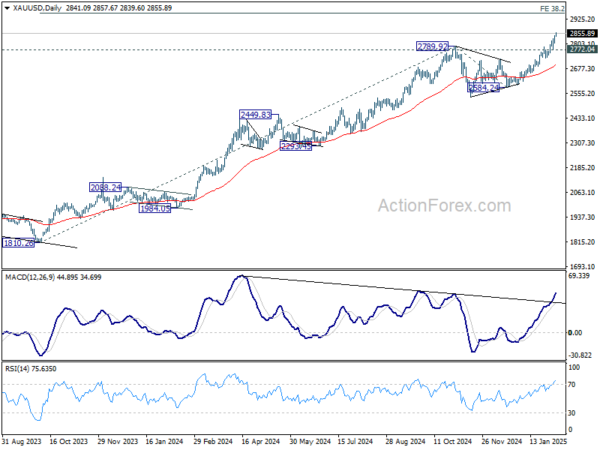

Gold gains as markets await Russia’s response to ceasefire proposal

Gold picked up momentum as investors closely monitor Kremlin’s response to the proposed ceasefire deal in Ukraine, as US officials head to Russia for negotiations.

Russia has yet to publicly endorse an immediate ceasefire, but has indicated that it is reviewing the plan, and a phone call between US President Donald Trump and Russian President Vladimir Putin is on the table.

However, Trump remains skeptical, stating that while he has received “positive messages” about the ceasefire, such reassurances “mean nothing” without concrete action from Putin.

Trump also warned that if Putin refuses to sign the deal, the US could take “financially very bad” actions against Russia, likely hinting at severe sanctions.

Ukrainian President Volodymyr Zelenskyy said earlier in the week that stronger Western financial and military support would follow should the ceasefire negotiations fail.

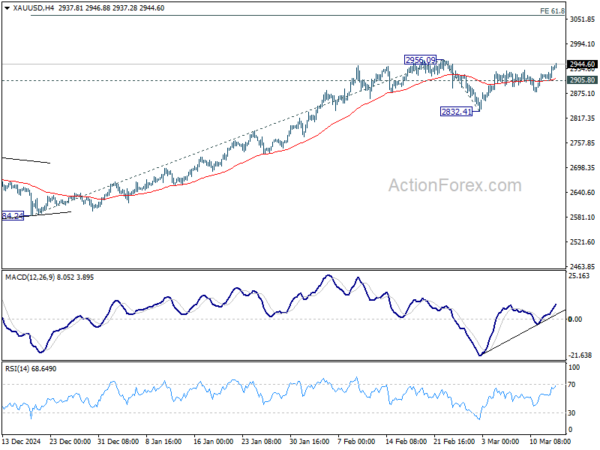

Technically, Gold’s near term rebound from 2832.41 extended higher today and focus is now on 2956.09 resistance. Decisive break there will resume the larger up trend to 3000 psychological, and possibly further to 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21.

However, break of 2905.80 support should extend the corrective pattern from 2956.09 with another falling leg back to 2832.41 and possibly below.

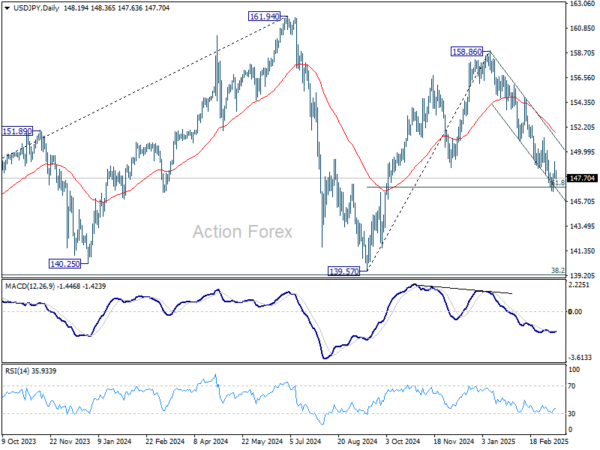

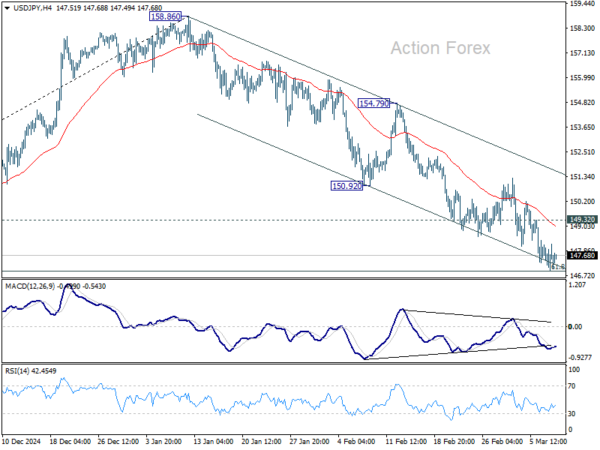

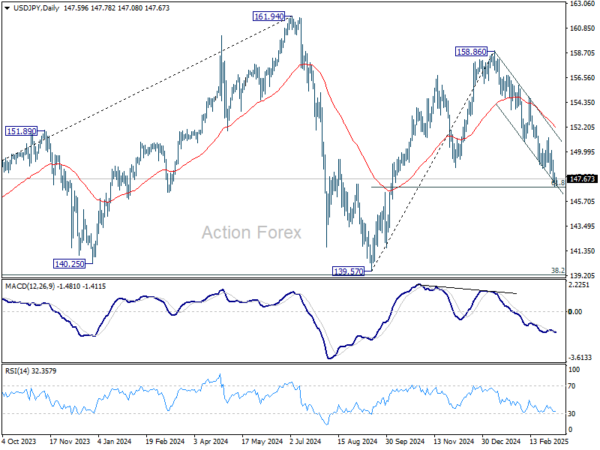

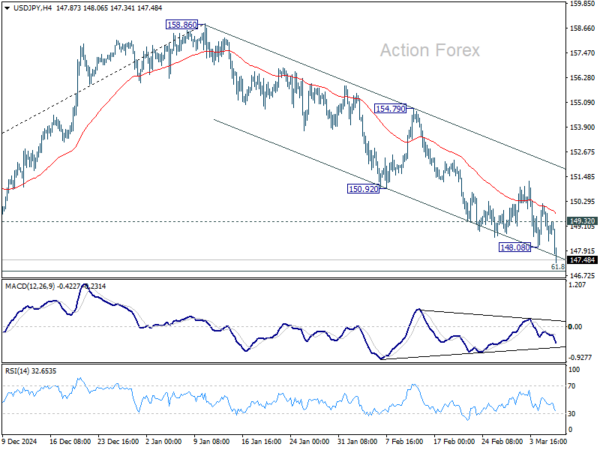

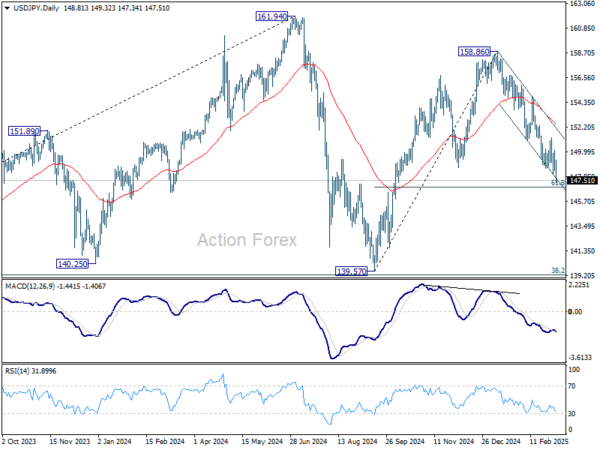

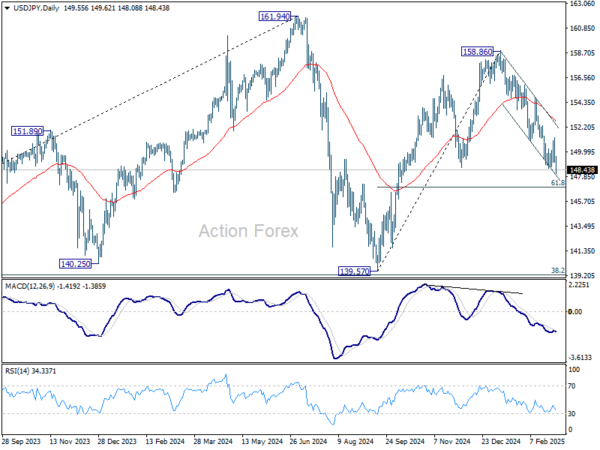

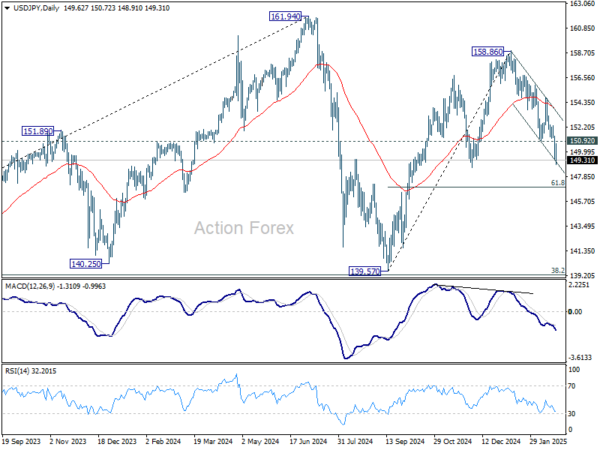

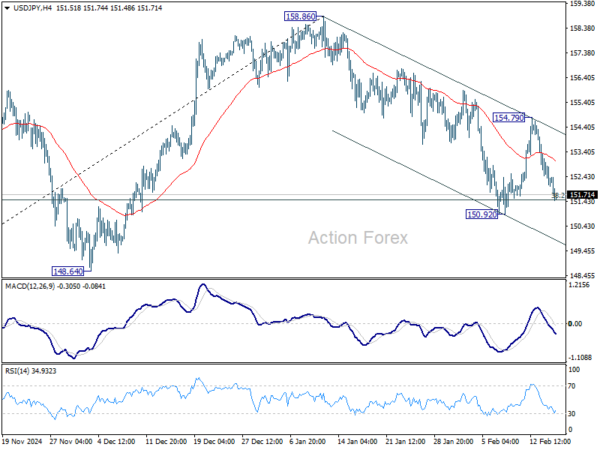

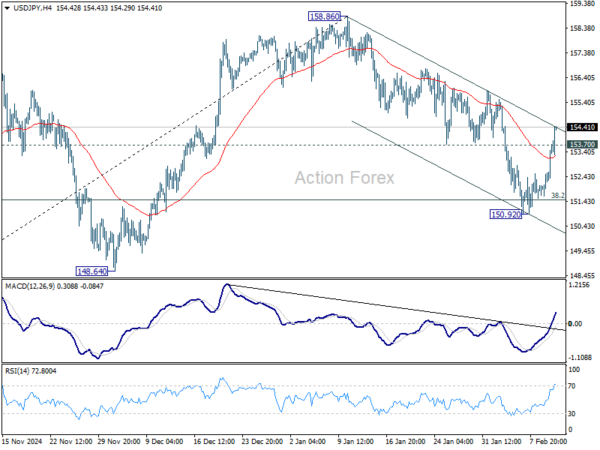

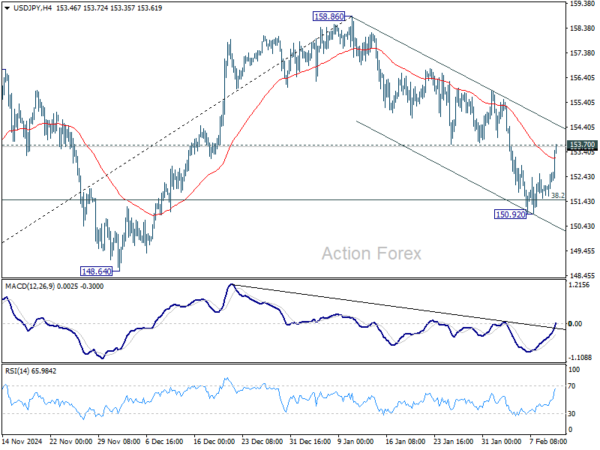

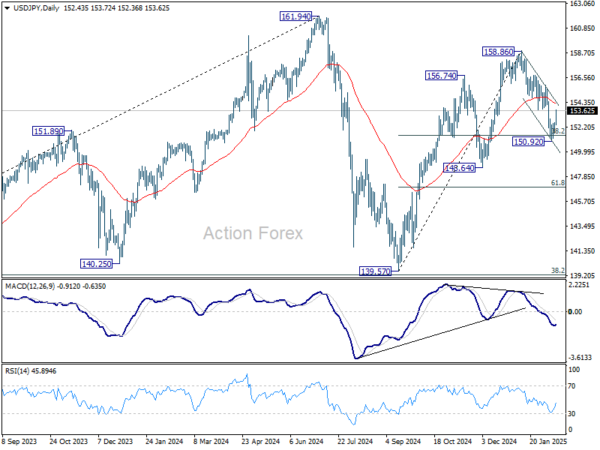

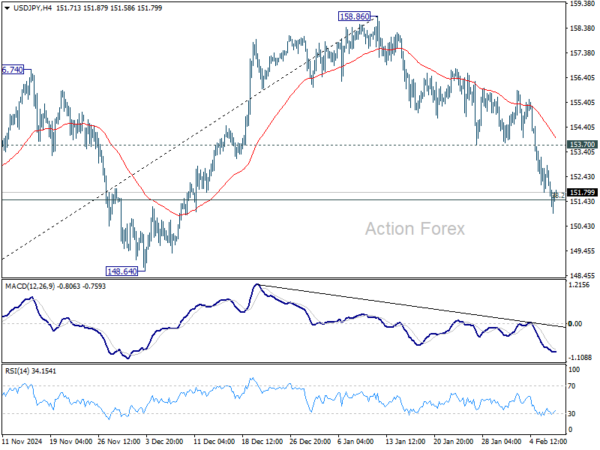

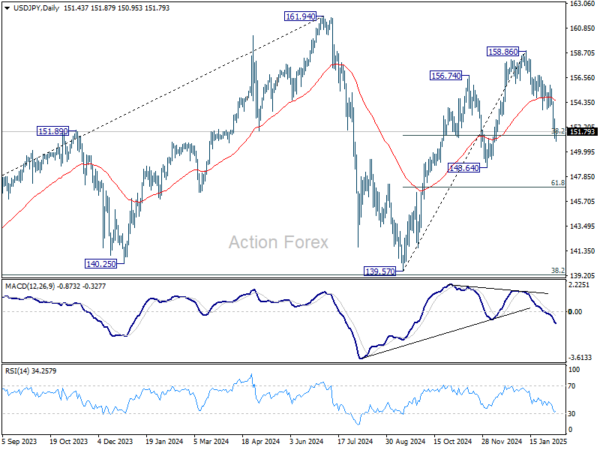

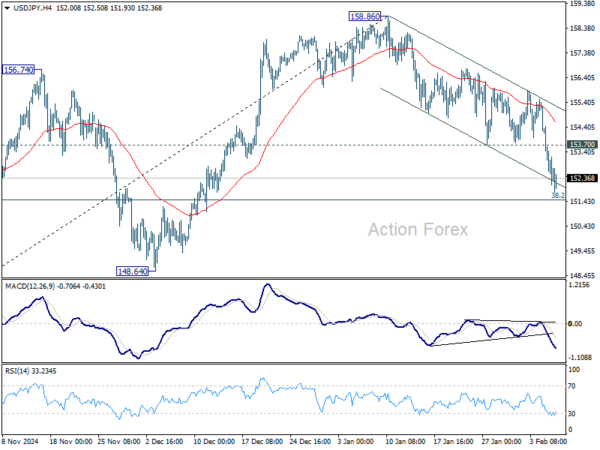

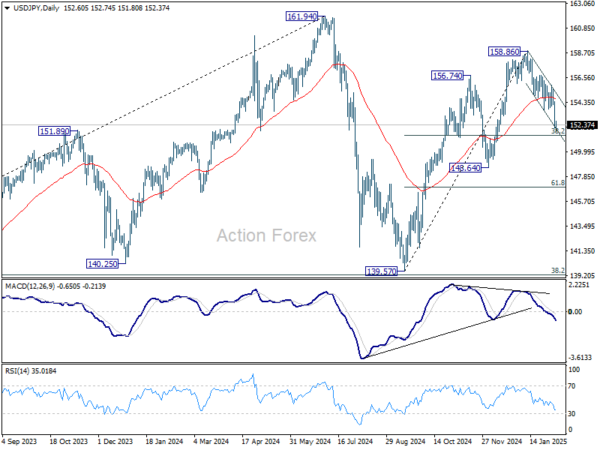

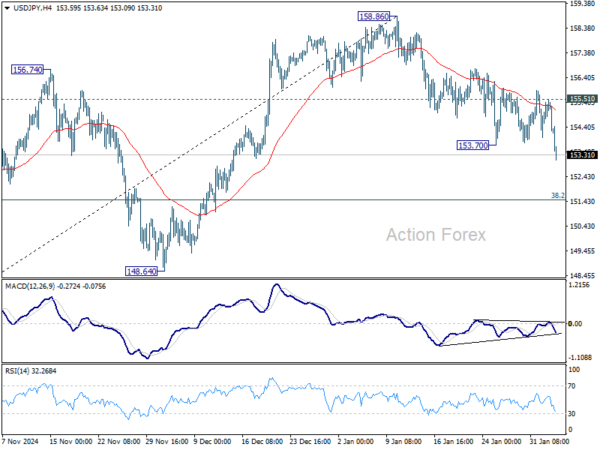

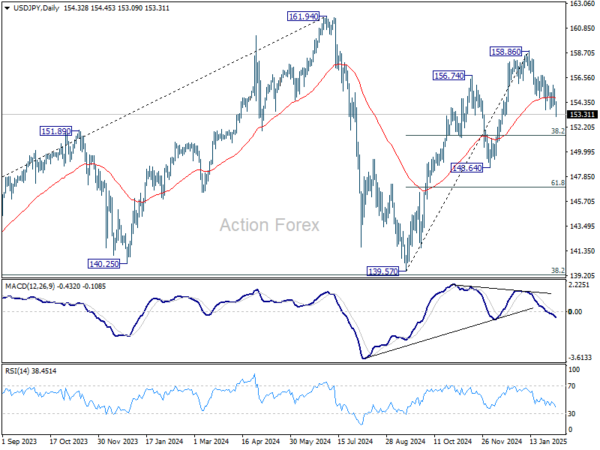

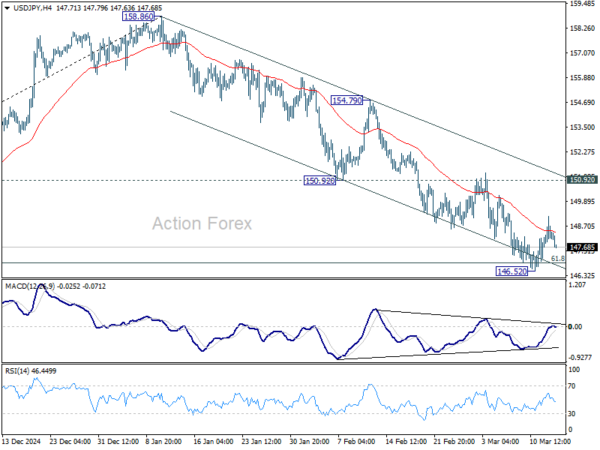

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.51; (P) 148.35; (R1) 149.10; More…

Intraday bias in USD/JPY remains neutral for the moment, and more consolidations could be seen above 146.52. Upside of recovery should be limited by 150.92 support turned resistance. On the downside, sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support.

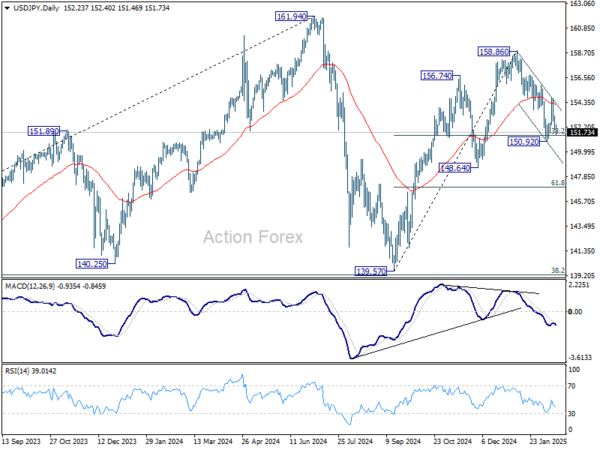

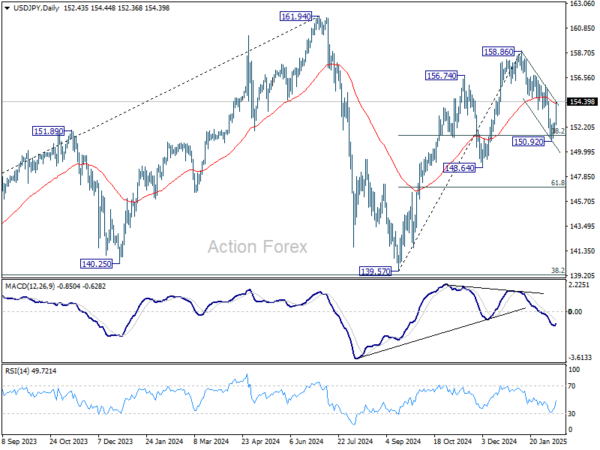

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.