Geopolitical developments dominated global headlines last week, particularly surrounding peace negotiations over Russia’s invasion of Ukraine and evolving US-Ukraine relations. While US President Donald Trump’s tariffs took a backseat, concerns over their impact on consumer spending and economic growth resurfaced by the end of the week, triggering renewed risk aversion.

Markets lacked clear direction for most of the week, with major assets struggling to gain momentum in either direction. However, risk sentiment soured late in the week as fresh worries emerged over the potential inflationary effects of tariffs, particularly on US consumers. This shift in tone could set the market narrative for the near term.

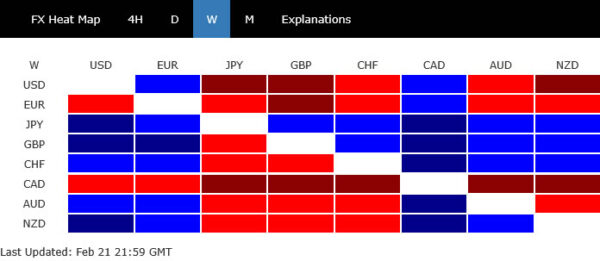

Against this backdrop, Dollar initially struggled but recovered some ground by the week’s close, finishing as the third worst performer overall. The late-week risk-off mood helped Dollar stabilize, with Dollar Index showing potential for a rebound off key Fibonacci support if risk aversion deepens further.

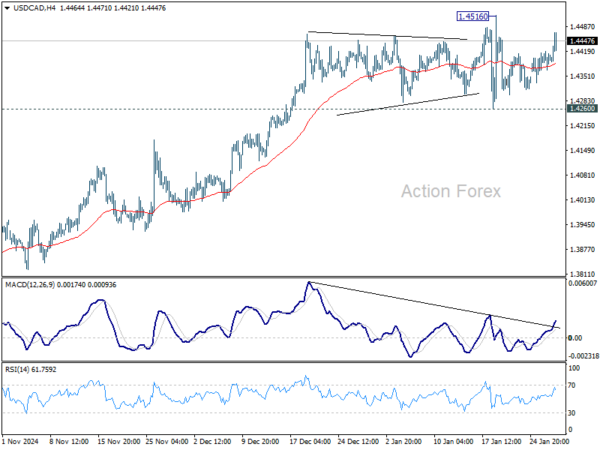

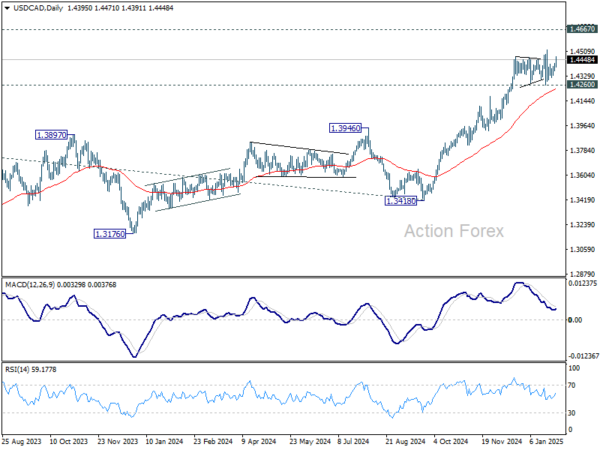

Euro finished as the second weakest currency, partly weighed down by disappointing PMI data. Hopes for a political boost from German election over the weekend could be short-lived, as renewed US tariff threats may quickly drag Euro lower again. The worst performer was Canadian Dollar, which faced additional pressure from concerns over trade and slowing economy.

In contrast, Yen emerged as the strongest currency, benefiting from increasing speculation of an earlier-than-expected BoJ rate hike. Divergence in yields also provided support, as Japan’s JGB yields rose while US Treasury yields declined.

Sterling and the Swiss Franc were the second and third strongest, respectively, as both benefited from uncertainty surrounding Euro. Australian and New Zealand Dollars ended mixed, weighed down by the late-week risk aversion. However, Kiwi ended up with a slight upper hand over Aussie.

Stocks Slide as Consumer Confidence Plunges, Dollar Index Holds Key Support

US stocks ended the week notably lower as earlier resilience turned into steep selloff on Friday. S&P 500, which had set a new record high, ended the week with -1.7% loss, while DOW and NASDAQ both fell -2.5%. DOW’s -700-point drop on Friday marked its worst trading day of the year, catching many investors off guard and raising concerns over broader market sentiment.

At the heart of the selloff was the unexpected deterioration in consumer sentiment. The University of Michigan Consumer Sentiment Index for February was finalized at 64.7, significantly below January’s 71.7 and the preliminary reading of 67.8. This was the lowest level since November 2023, signaling growing unease among US households about economic conditions.

Adding to market anxiety, inflation expectations surged. Households now expect inflation over the next year to rise to 4.3%, the highest since November 2023, up from 3.3% last month. Over the next five years, inflation expectations climbed to 3.5%, the highest level since 1995, compared to 3.2% in January.

Some analysts attribute the drop in sentiment to uncertainty over US President Donald Trump’s policies, particularly the potential for inflationary effects from new tariffs. The University of Michigan noted that the deterioration in sentiment was led by the -19% drop in buying conditions for durable goods, as consumers fear tariff-driven price hikes. Additionally, expectations for personal finances and the short-run economic outlook fell by nearly -10%.

However, there are differing views on the inflationary impact of tariffs. Some analysts argue that Trump’s tariff threats are more of a strategic negotiation tool aimed at broader geopolitical objectives, such as pressuring Canada and Mexico on fentanyl issues. If these concerns fade, inflation expectations could retreat, allowing consumer confidence to rebound.

Technically, DOW’s steep decline and strong break of 55 D EMA (now at 43848.97) is clearly a near term bearish sign. However, current fall from 45054.36 are seen as the third leg of the corrective pattern from 45073.63 only. Hence, while deeper fall could be seen to medium term rising channel support (now at around 42530) or below, strong support should emerge around 41884.89 to complete the pattern and bring up trend resumption.

However, decisive break of 41844.89 will complete a double top reversal pattern (45073.63, 45054.36). DOW would then be at least in correction to the up trend form 32327.20. That would open up deeper correction to 38.2% retracement of 32327.20 to 45054.36 at 40204.49, or even further to 38499.27 support. But then, this is far from being the base scenario at this point.

For now, Dollar Index is still sitting above 38.2% retracement of 100.15 to 110.17 at 106.34. Near term risk aversion could help Dollar Index defend this support level, with prospect of a bounce from there. Firm break of 55 D EMA (now at 107.40) should bring stronger rally back towards 110.17 high. However, Decisive break below the 106.34 support would deepen the decline to 61.8% retracement at 103.98, even still as a correction.

Yen Ends Week Strong as BoJ Might Hike Rates Again Sooner

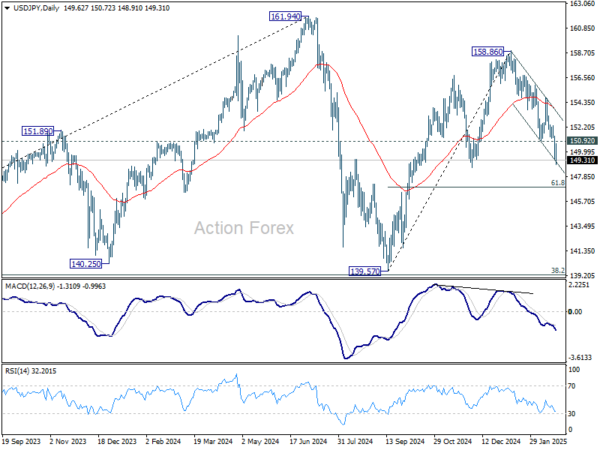

Yen ended last week as the best-performing currency, thanks to robust inflation data and hawkish remarks from BoJ officials. The rally briefly paused midweek after BoJ Governor Kazuo Ueda signaled readiness to intervene in the bond market, causing Japan’s 10-year JGB yield to retreat from its 15-year high. However, this setback proved temporary, as Yen quickly regained strength amid rising risk aversion and falling US Treasury yields.

According to the latest Reuters poll, 65% of economists (38 out of 58) expect BoJ to raise rates from 0.50% to 0.75% in July or September. Among the 39 analysts who gave a specific month, 59% (23 respondents) chose July, while 15% (six analysts) expected a June hike. The remaining 10 analysts were evenly split between April and September.

However, stronger-than-anticipated inflation could give BoJ further cause to pull the timetable forward. Last week’s data already showed core CPI surging more than expected to 3.2% in January, marking the fastest pace in 19 months. If consumer price pressures remain elevated, markets speculate that policymakers might prefer to act sooner rather than wait for the second half.

The April 30 – May 1 policy meeting could stand out as an appropriate window for BoJ to act. By then, BoJ will have access to Shunto wage negotiation results and an updated economic outlook, providing the necessary justification for an earlier rate hike.

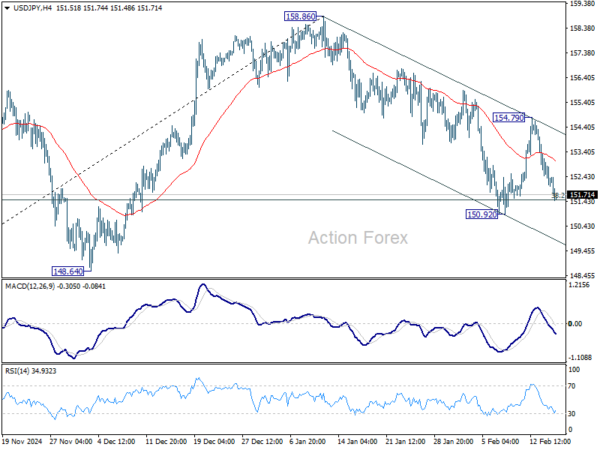

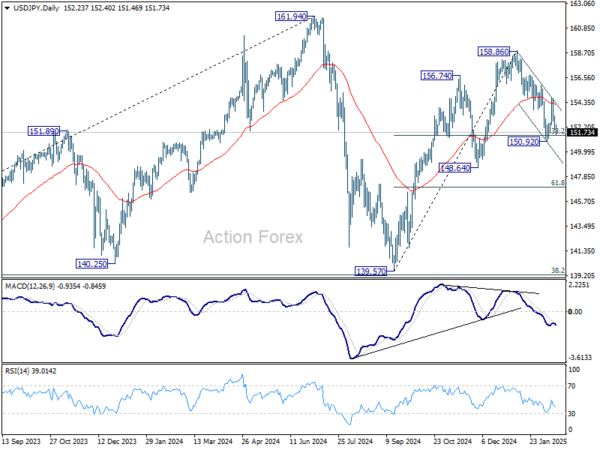

USD/JPY’s extended decline last week suggests that rebound from 139.57 has already completed with three waves up to 158.86. Fall from 158.86 is now seen as the third leg of the pattern from 161.94.

Deeper fall is expected as long as 150.92 support turned resistance holds, to 61.8% retracement of 139.57 to 158.86 at 146.32. Firm break there will pave the way back to 139.57. Meanwhile, break of 150.92 will delay the bearish case and bring some consolidations first.

Any extended USD/JPY weakness should limit Dollar’s rebound. However, this alone shouldn’t be enough to push DXY below key fibonacci support at 106.34 mentioned above.

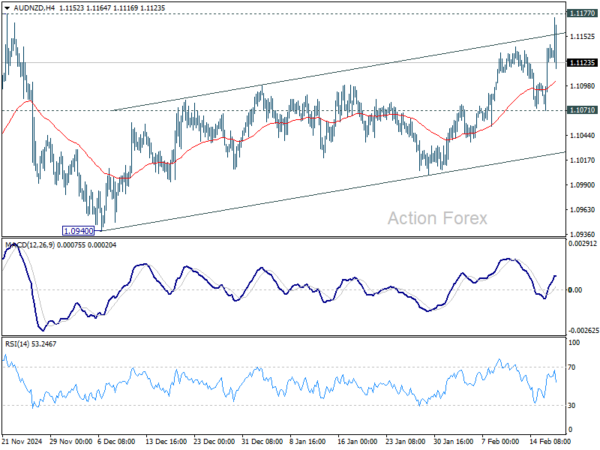

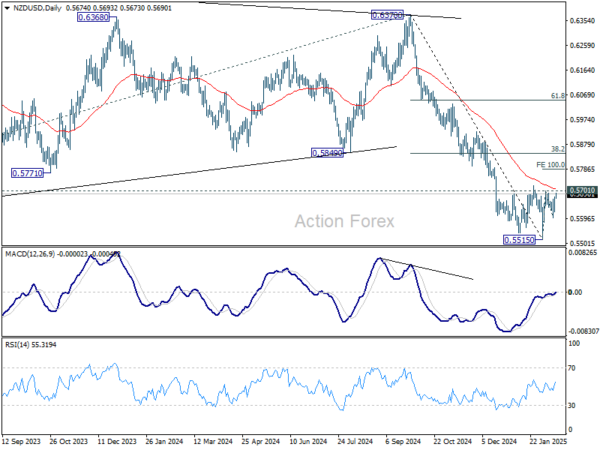

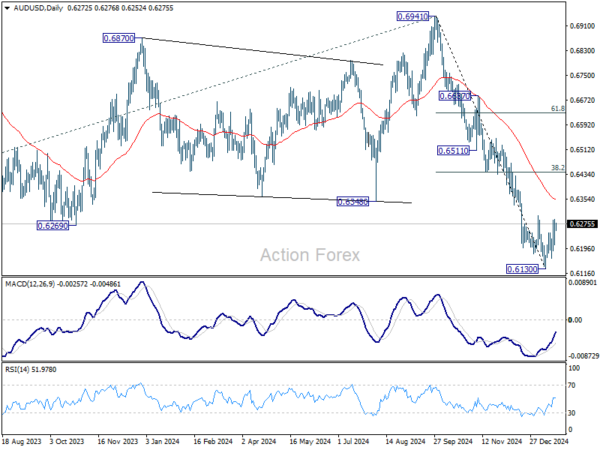

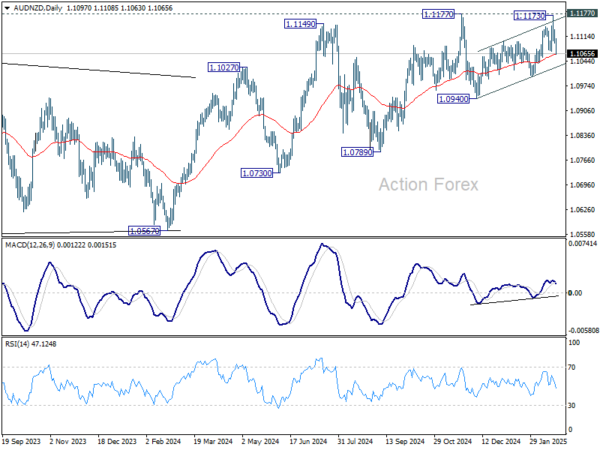

AUD/NZD Reverses after RBA and RBNZ Rate Cuts

Both RBA and RBNZ delivered rate cuts last week, with RBA lowering its cash rate by 25bps to 4.10% and RBNZ cutting by 50bps to 3.75%, in line with expectations.

RBA maintained a cautious tone, with Governor Michele Bullock emphasizing “patience” before considering another cut. The accompanying statement warned against easing “too much too soon,” highlighting concerns that disinflation progress could stall and inflation could settle above the midpoint of the target range if policy is loosened aggressively.

Australian economic data also reinforced RBA’s cautious stance, with strong job growth and elevated wage pressures supporting a measured pace of policy easing.

Meanwhile, RBNZ delivered a more defined path for easing, with Governor Adrian Orr clearly ruling out further 50bps cuts barring an economic shock. Instead, the central bank has outlined two additional 25bps cuts in the first half of the year.

In the currency markets, AUD/NZD saw a sharp decline, falling back toward its 55 D EMA (now at 1.1063). The key driver of this move is likely the perception that RBNZ is nearing the end of its rate-cutting cycle, while RBA has only just begun easing, leaving room for further reductions if economic conditions weaken.

With the OCR at 3.75% already close to the neutral band, there is limited downside for RBNZ, while RBA at 4.10% has more room to cut rates. This policy divergence, particularly if Australia’s economy slows further due to trade tensions between US and China, could keep downward pressure on AUD/NZD in the near term.

Technically, sustained trading below 55 D EMA should confirm rejection by 1.1177 resistance. Fall from 1.1173 would be seen as the third leg of the corrective pattern from 1.1177. Further break of near term channel support (now at 1.1029) would pave the way back to 1.0940 support next.

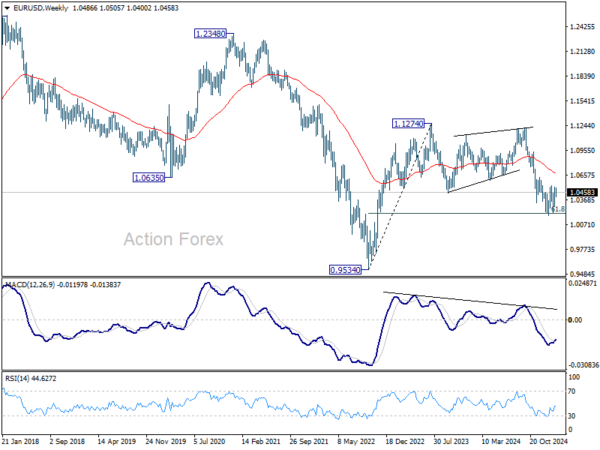

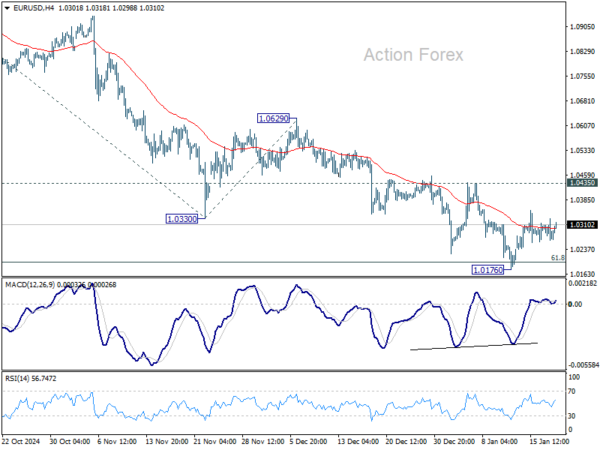

EUR/USD Weekly Outlook

Range trading continued in EUR/USD last week and outlook is unchanged. Initial bias remains neutral this week first. Price actions from 1.0176 are seen as a corrective pattern only. IN case of further rise, upside should be limited by 38.2% retracement of 1.1213 to 1.0176 at 1.0572. On the downside, break of 1.0400 support will turn bias back to the downside for 1.0176/0210 support zone. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, focus stays on on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, strong rebound from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0929). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, eventual downside breakout would be mildly in favor.