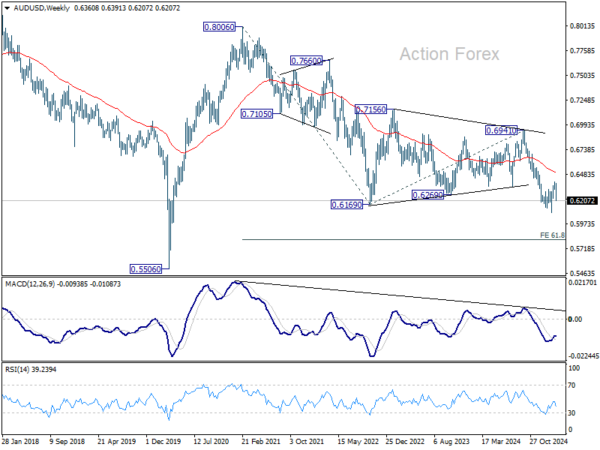

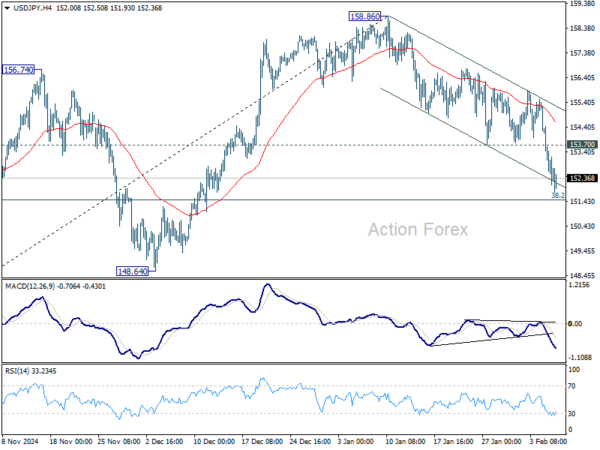

The risk-off sentiment that triggered the biggest US stock market selloff in months has spilled over into Asian markets, leading to broad declines across the region. The currency markets reflect this shift too, with traditional safe havens such as Japanese Yen and Swiss franc leading gains in Asia, while risk-sensitive currencies like the Australian and New Zealand Dollars face pressure.

Unlike previous bouts of risk aversion, Dollar is not benefiting from the current flight to safety. This time, the core of the problem originates from the US economy itself, where recession worries are intensifying. Rather than flocking to the greenback, investors appear to be diversifying into other safe havens or moving to the sidelines until the dust settles.

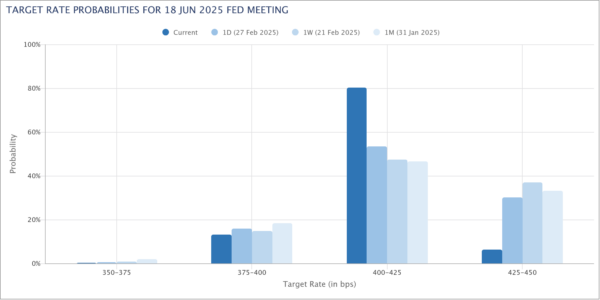

The uncertainty surrounding US trade policies has left businesses and consumers hesitant, potentially dragging economic growth lower. In response to the changing economic outlook, market participants are increasingly convinced that Fed will resume policy easing within the first half of the year. The only question is whether the next rate cut will arrive in May or June.

Another driver of Dollar weakness is the extending decline in yields since mid January. Technically, there is prospect for 10-year yield to draw support from 4.000 psychological level, which is slightly below 61.8% retracement of 3.603 to 4.809 at 4.063, to form a near term bottom. However, there is little prospect for 10-year yield to rebound strongly through 55 D EMA (now at 4.412). But at least, sideway movement in 10-year yield could help lift the pressure on Dollar.

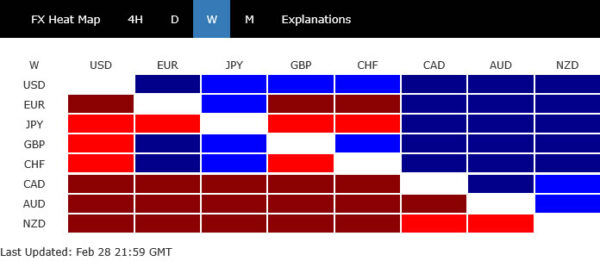

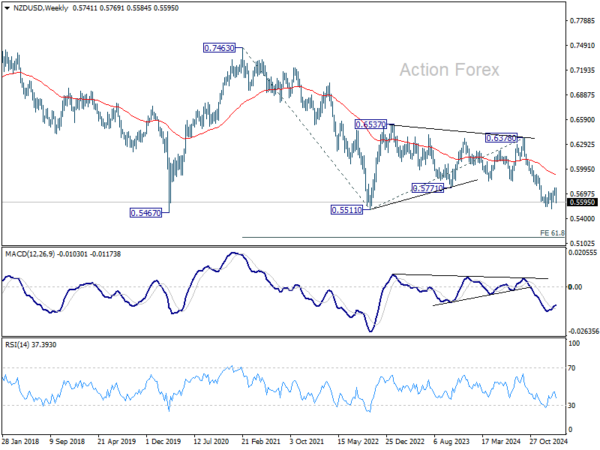

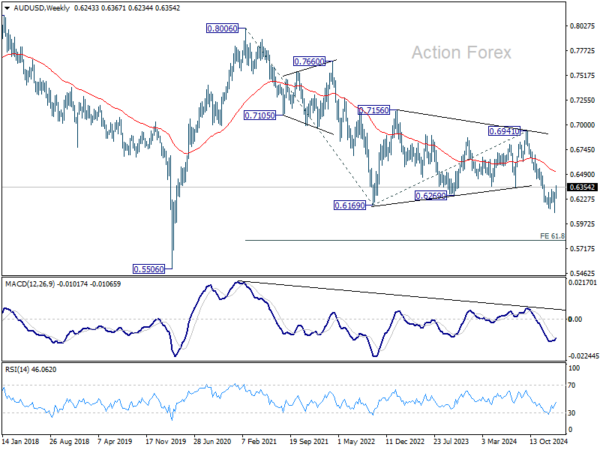

Overall for the week so far, Yen is the best performer, followed by Euro, and then Swiss Franc. Aussie is the worst, followed by Loonie and then Kiwi. Dollar and Sterling are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -1.02%. Hong Kong HSI is down -1.02%. China Shanghai SSE is down -0.50%. Singapore Strait Times is down -2.02%. Japan 10-year JGB yield is down -0.063 at 1.509. Overnight, DOW fell -2.08%. S&P 500 fell -2.70%. NASDAQ fell -4.00%. 10-year yield fell -0.104 to 4.213.

US stock market correction deepens as recession fears take hold

The US stock market suffered its most significant setback in months, with the S&P 500 dropping -2.7%, its biggest one-day decline since December 18. NASDAQ also lost -4.0%, marking its worst single-day percentage loss since September 2022. Analysts widely point to mounting recession worries as the primary catalyst behind the selloff.

Initial concerns emerged over the past month following a series of weaker economic data points, believed by some to be early reactions to an increasingly contentious tariff policy. These worries intensified after recent remarks from the White House suggested a bumpy economic outlook ahead.

In an interview aired on Sunday, US President Donald Trump fueled apprehensions further by describing the economy as going through “a period of transition.” When pressed about an impending recession, he avoided a direct prediction but acknowledged potential “disruption.” His remarks—“Look, we’re going to have disruption, but we’re OK with that”—did little to reassure investors already on edge about growth prospects.

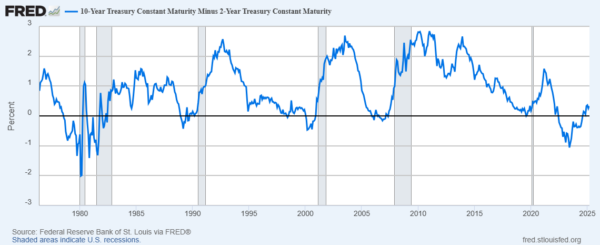

Adding further weight to recession fears, historical bond market indicators have been flashing warning signs. The 10-year to 2-year US yield curve inverted in mid-2022—a classic recession signal—and only turned positive again in September 2024. Historically, a U.S. recession tends to follow within months after the yield curve normalizes (i.e., turned positive again). If this trend holds true, the US economy could be inching closer to a downturn.

However, another view posits that tariffs are a distraction and that the real driver behind the US selloff is the recent surge in Japanese government bond yields, which have hit a 16-year high. As the carry trade unwinds—where investors borrow in low-yield currencies, often involving Japanese Yen, to fund investments in higher-yield or high-growth assets—capital is flowing out of big tech names, contributing to the NASDAQ’s outsized losses.

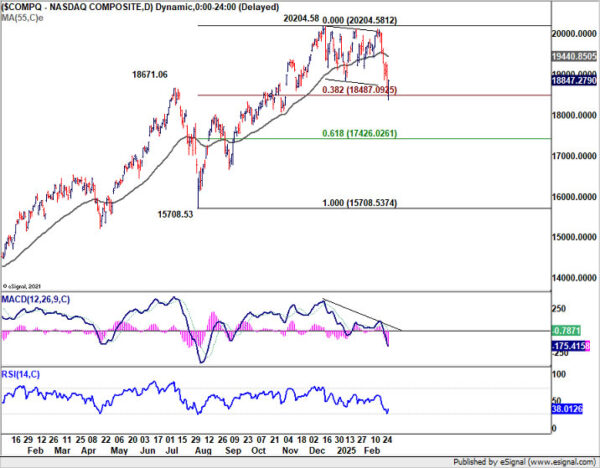

Technically, NASDAQ’s strong break of 55 W EMA (now at 17864.01) suggests that it’s already in correction to the up trend from 10088.82 (2022 low). Deeper fall should be seen to 38.2% retracement of 10088.82 to 20204.58 at 16340.36. Reaction from there will decide whether it’s merely in a medium consolidations phase or in an out-right bearish trend reversal.

As for DOW, immediate focus is now on 41844.89 support. Firm break there will complete a double top reversal pattern (45073.63, 45054.36). That should set up deeper fall to 38.2% retracement of 32327.20 to 45073.63 at 40204.49 at least, even it’s just a correction to the rise from 32327.20.

Australia Westpac consumer sentiment jumps to 95.9, soft landing achieved

Australian consumer sentiment saw a strong rebound in March, with Westpac Consumer Sentiment Index jumping 4.0% mom to 95.9, the highest level in three years and not far from neutral 100 mark.

Westpac attributed the improvement to slowing inflation and February’s RBA interest rate cut which have lifted confidence across households. positive views on job security suggest that “soft landing has been achieved”. Nevertheless, “unsettling overseas news” continues to weigh on the broader economic outlook.

Looking ahead to RBA’s upcoming meeting on March 31-April 1, Westpac expects the central bank to keep the cash rate unchanged. RBA was clear that the 25bps cut in February “did not mean further reductions could be expected at subsequent meetings.”

Westpac added, “further slowing in inflation will give the RBA sufficient confidence to deliver more rate cuts this year with the next move coming at the May meeting”.

Australia’s NAB business confidence slips back into negative as cost pressures persist

Australia’s NAB Business Confidence fell from 5 to -1 in February, erasing last month’s gain and returning to below-average levels. While business conditions improved slightly from 3 to 4, the decline in confidence suggests that businesses remain cautious despite RBA’s recent rate cut and positive Q4 GDP data.

NAB Chief Economist Alan Oster noted that the lift in sentiment seen in January was not sustained, signaling ongoing uncertainty in the business environment. Persistent cost pressures and subdued profitability appear to be key factors weighing on sentiment, keeping confidence below long-term norms.

Within business conditions, trading conditions ticked up from 7 to 8, and profitability conditions rose slightly from -2 to -1, though still remaining in negative territory. Employment conditions, however, weakened from 5 to 4.

Cost pressures remain a concern, with purchase cost growth accelerating from 1.1% to 1.5% in quarterly equivalent terms. On the positive side, labor cost growth eased from 1.7% to 1.5%, indicating that wage price pressures are gradually cooling. Meanwhile, final product price growth slowed from 0.8% to 0.5%, though retail price inflation held steady at 1.0%.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7149; (P) 1.7213; (R1) 1.7320; More…

EUR/AUD’s rally resumed and brief consolidations and intraday is back on the upside. Rise from 1.6335 should now target 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next. On the downside, below 1.7102 minor support will turn intraday bias neutral again and bring consolidations, before staging another rally.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 key resistance will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6355 support holds, even in case of deep pullback.