Dollar edged lower in early U.S. trading following weaker-than-expected retail sales data. However, the downside pressure remained limited, as investors took comfort in the fact that February’s sales growth marked a return to expansion after contraction in January. The data helped ease fears of an extended downturn in consumer spending, with markets breathing a sigh of relief that demand has not fallen into a prolonged slump. Still, with Fed’s policy decision and updated economic projections looming midweek, traders remain cautious and hesitant to take aggressive positions.

Beyond Fed, geopolitical developments are also on investors’ minds. U.S. President Donald Trump indicated he would speak with Russian President Vladimir Putin on Tuesday to discuss potential steps toward ending the war in Ukraine. This follows positive talks between US and Russian officials in Moscow, raising hopes that diplomatic efforts could progress. However, it remains uncertain whether concrete agreements will emerge, and markets will be closely monitoring any developments that could impact global risk sentiment.

Meanwhile, Euro traders are also in wait-and-see mode, with focus squarely on Germany’s parliamentary vote on Chancellor-in-waiting Friedrich Merz’s proposed state borrowing program tomorrow. The budget committee approved the plans on Sunday, but the vote faces last-minute legal challenges from the far-right Alternative for Germany party, which has petitioned the constitutional court, arguing that there was insufficient time for expert scrutiny. If the challenge gains traction, it could delay or complicate the EUR500B infrastructure and defense spending program.

Adding to concerns for Germany, the Munich-based Ifo Institute released a bleak economic forecast, predicting that the country’s economy will grow by just 0.2% this year, following two consecutive years of contraction. The report cited weak demand for industrial goods and increasing competitive pressures from global markets as key drags on growth.

In the currency markets, New Zealand Dollar is currently the strongest performer, followed by Australian Dollar, both of which are benefiting from renewed optimism surrounding China’s “special action plan” to boost consumption. On the other end, Japanese Yen is the weakest, followed by Dollar and Euro. The British pound and Swiss Franc are currently in the middle of the pack.

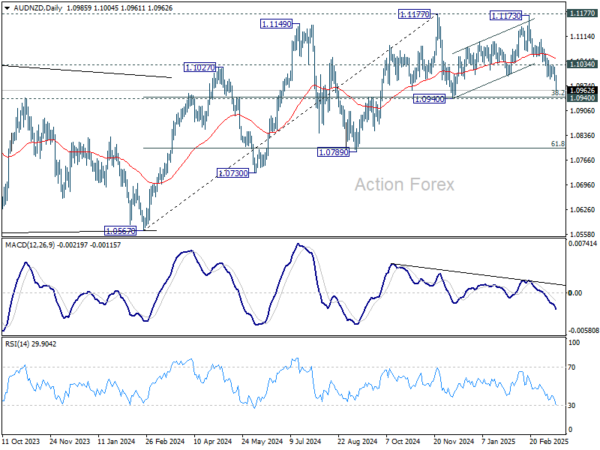

Technically, AUD/NZD’s decline from 1.1173 accelerates lower today. Immediate focus is now on 1.0940 cluster support (38.2% retracement of 1.0567 to 1.1177 at 1.0944). Strong rebound from there will keep the up trend from 1.0567 intact for another rally through 1.1177 at a later stage. However, sustained break of 1.0940/4 will complete a double top pattern (1.1177, 1.1173), and indicates bearish trend reversal. Deeper decline should then be seen to 61.8% retracement at 1.0800 next.

In Europe, at the time of writing, FTSE is up 0.26%. DAX is up 0.26%. CAC is up 0.40%. UK 10-year yield is down -0.023 at 4.651. Germany 10-year yield is down -0.060 at 2.819. Earlier in Asia,Nikkei rose 0.93%. Hong Kong HSI rose 0.77%. China Shanghai SSE rose 0.19%. Singapore Strait Times rose 0.61%. Japan 10-year JGB yield fell -0.025 to 1.503.

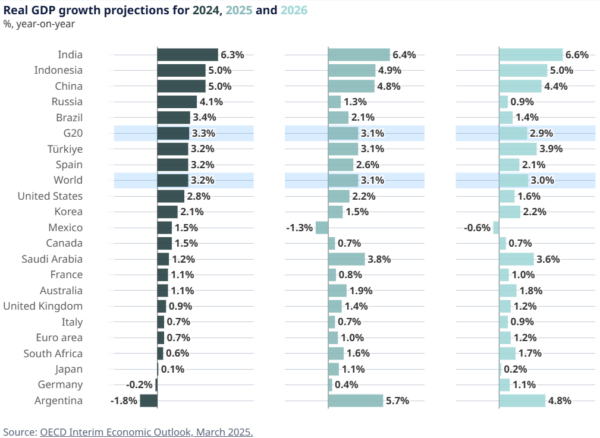

OECD trims global growth outlook amid trade tensions and policy uncertainty

OECD forecasts a slight slowdown in global economic growth over the next two years, reflecting the effects of escalating trade tensions and heightened policy uncertainty. In its Interim Economic Outlook, OECD projects global growth will ease from 3.2% in 2024 to 3.1% in 2025, and further to 3.0% in 2026. These numbers represent a downgrade from its previous forecasts, which projected 3.3% growth for both this year and next.

Among advanced economies, the US is expected to lose momentum, with growth forecast at 2.2% in 2025 before cooling to 1.6% in 2026—down from earlier estimates of 2.4% and 2.1%.

Meanwhile, Eurozone is projected to increase from 1.0% growth this year to 1.2% in 2026. Although this marks an improvement relative to 2024’s mild performance, it still lags the OECD’s previous forecasts of 1.3% and 1.5%.

The imposition of higher tariffs is expected to weigh particularly heavily on North American economies beyond the US. Canada’s growth rate is set to slow to 0.7% this year and next, well below the 2% previously estimated.

Mexico would be hit hardest, with its economy forecast to contract by -1.3% in 2025 and a further -0.6% the following year—reversing prior expectations for moderate growth.

By contrast, China appears relatively well-positioned to manage the fallout from higher tariffs. OECD anticipates that targeted government stimulus will support growth to 4.8% in 2025—slightly above the previous forecast of 4.7%—before moderating to 4.4% in 2026.

OECD Secretary-General Mathias Cormann warned that signs of weakness are emerging in the global economy, primarily due to “heightened policy uncertainty.” He added that “increasing trade restrictions” will raise costs for both production and consumption.

US retail sales rises 0.2% mom in Feb, ex-auto sales up 0.3% mom

US retail sales grew 0.2% mom to USD 722.7B in February, well below expectation of 0.7% mom. Ex-auto sales rose 0.3% mom to USD 584.7B , below expectation of 0.5% mom.

Ex-gasoline sales rose 0.3% mom. to USD 669.9B. Ex-auto& gasoline sales rose 0.5% mom to USD 627.2B.

Total sales for December through February period was up 3.8% from the same period a year ago.

ECB’s de Guindos: Trump’s tariffs complicate ECB’s monetary policy decisions

ECB Vice President Luis de Guindos acknowledged that US President Donald Trump’s tariff policies have made the central bank’s monetary policy decisions more challenging, creating an environment of increased uncertainty.

Speaking to Spanish radio Onda Cero, de Guindos noted that the “clarity regarding future decisions” has diminished in a situation “much more opaque than just six months ago.”

He also pushed back ECB’s inflation target timeline, stating that inflation is now expected to reach the 2% goal in Q1 2026, later than the previous mid-2025 projection, due to the impact of higher energy prices.

Despite these concerns, de Guindos remained cautiously optimistic that “everything is moving in the right direction.” While tariffs could lead to some short-term inflationary effects, he suggested that slower economic activity resulting from trade disruptions could ultimately offset these pressures over time.

NZ BNZ services falls to 49.1, slips back into contraction

New Zealand’s BusinessNZ Performance of Services Index fell back into contraction territory in February, dropping from 50.4 to 49.1. The index remains well below its long-term average of 53.0.

Key components of the survey also showed deterioration, with Activity/Sales slipping from 53.8 to 49.2, New Orders/Business falling from 50.0 to 49.4, and Stocks/Inventories declining from 50.0 to 48.0. While Employment showed a slight improvement, rising from 47.4 to 48.9, it remains in contraction.

Despite the sector’s renewed contraction, negative sentiment among businesses showed a modest improvement, with 57.8% of comments in February expressing pessimism, down from 61.9% in January. Most firms cited the challenging economic climate as their primary concern.

BNZ’s Senior Economist Doug Steel said that “while one might have hoped that the PSI would move higher again, we know that economic turning points can be messy. The brief foray above 50 in January remains the only month in the last year the PSI hasn’t been in contraction”.

China’s data shows resilient start in 2025, government unveils plan to boost consumption

China’s economy got off to a stronger-than-expected start in the first two months of the year. Industrial production grew 5.9% yoy, beating market expectations of 5.3% yoy. Retail sales also exceeded forecasts, rising 4.0% yoy compared to an expected 3.8% yoy, reflecting improving consumer demand.

Meanwhile, fixed asset investment increased by 4.1% yoy, surpassing projections of 3.2% yoy, but ongoing weaknesses in the real estate sector persisted, with property investment falling -9.8% yoy. Additionally, private investment remained flat, signaling that confidence among smaller businesses and private enterprises was subdued.

China’s National Bureau of Statistics noted that existing and new policies aimed at stimulating growth have begun to take effect, leading to steady expansion in the industrial and services sectors, improved investment, and stable employment conditions. Officials highlighted “new quality productive forces” as key drivers of momentum.

To further bolster domestic demand, China’s State Council unveiled a “special action plan” over the weekend, aiming to increase household incomes, introduce childcare subsidies, and reduce financial burdens to encourage consumption.

While the plan was widely circulated across local governments, it lacked concrete details on financial support for implementation, leaving uncertainties about its immediate impact.

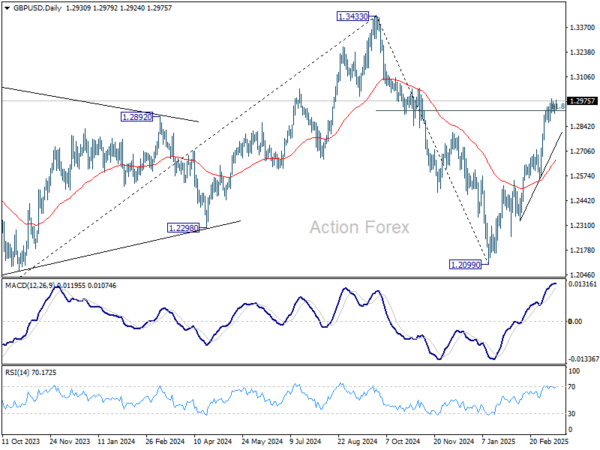

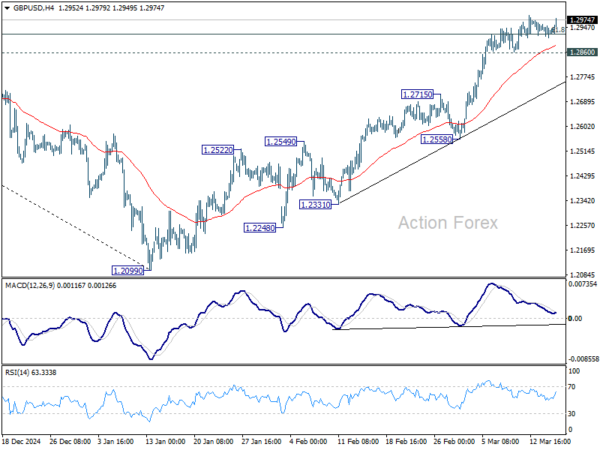

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2910; (P) 1.2934; (R1) 1.2958; More…

GBP/USD bounces slightly today and outlook is unchanged. Further rally is in favor with 1.2860 support intact. On the upside, sustained trading above 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high. However, break of 1.2860 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.